Learn how to calculate land value for fiscal policy. Our guide covers key methods, data requirements, and implementation steps for land value capture.

June 23, 2026

How to Calculate Land Value for Fiscal Policy & Reform

Learn how to calculate land value for fiscal policy. Our guide covers key methods, data requirements, and implementation steps for land value capture.

You're likely in one of two places right now. Either your ministry has been asked to design a land-based revenue reform and the valuation team is stuck on a basic question, “how do we calculate land value at scale?” Or you already have assessed values on the books, but they aren't reliable enough to support a recurring levy without provoking appeals, political resistance, and credibility problems.

That problem is more common than most tax guidance admits. Many valuation manuals are built for one-off appraisals, mortgage underwriting, or depreciation treatment. A finance ministry needs something else. It needs a repeatable, auditable, policy-ready land valuation system that can support recurring public revenue, survive scrutiny, and update over time as markets move.

The practical challenge isn't just separating land from buildings. It's building a framework that works when sales are thin, when parcel records are incomplete, when zoning changes faster than cadastres, and when flood risk, transit access, or public investment alter site values in ways that ordinary appraisal templates barely address.

Table of Contents

- Why Accurate Land Valuation Is a Policy Superpower

- The Core Concepts of Land Value Assessment

- Choosing Your Primary Valuation Approach

- Mass Appraisal for System-Wide Fiscal Reform

- Refining Valuations with Adjustments and Externalities

- From Valuation Data to Policy Implementation

Why Accurate Land Valuation Is a Policy Superpower

Finance ministries usually encounter land valuation as a technical workstream. In practice, it's a strategic lever. If you can separate site value from building value, you can stop taxing construction improvements as if they were the same thing as scarce location value. That distinction changes the incentives embedded in the whole tax system.

When governments can't calculate land value cleanly, they tend to tax the visible object, the property as a whole. That often means a well-maintained building, a renovation, or a new apartment block faces a higher tax burden than a vacant or underused site in the same neighborhood. The result is predictable. Productive investment gets penalized. Passive holding gets rewarded.

Housing ministries feel this as affordability pressure. Urban planners see it as idle land, leapfrog development, and infrastructure inefficiency. Treasury officials experience it as a weak and politically fragile revenue base.

A useful reminder comes from the United States. The share of single-family house values attributable to land rose from 37.0 percent in 2012 to 39.9 percent in 2022, meaning just under two-fifths of typical single-family house value represented the underlying land rather than the structure, according to the FHFA land price appreciation analysis.1 That doesn't tell you what any one parcel is worth in your jurisdiction, but it does show why ministries can't treat land as a minor residual.

Why this matters in fiscal reform

A strong land valuation system gives policymakers three things at once:

- A cleaner base for recurring revenue. Land doesn't disappear, relocate, or depreciate the way structures do.

- A better signal for urban management. Rising site values often reveal where public investment, access, and regulatory privileges are being capitalized.

- A fairer separation of economic sources. Land value reflects location, legal rights, and surrounding community investment more than private effort alone.

Practical rule: If your tax reform team can't explain the difference between taxing a site and taxing a building, it isn't ready to draft rates.

The policy lens that changes the calculation

Under a tri-factor economic view, labor, capital, and nature aren't the same thing and shouldn't be taxed as if they are. That matters because most ministries already understand how to tax income and transactions. The missing piece is often the value created by location, public infrastructure, legal permission, and natural advantage.

Accurate land valuation turns that abstract principle into administrative reality. It lets a ministry ask better questions. Which value came from private construction? Which came from public action? Which came from scarce natural opportunity? Once that separation is credible, fiscal reform stops being a blunt instrument and starts becoming targeted policy.

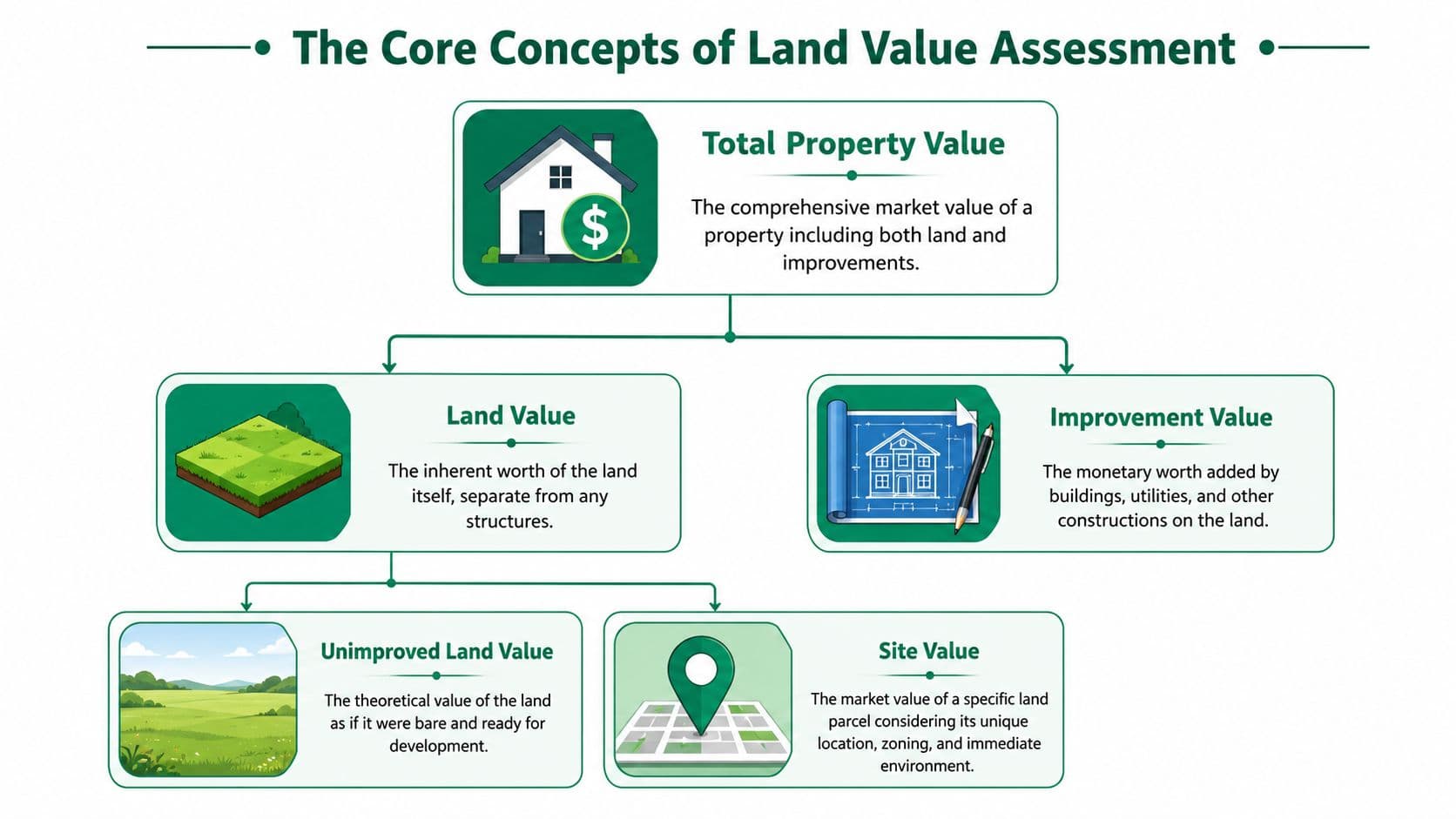

The Core Concepts of Land Value Assessment

The first mistake most reform teams make is using property value, land value, and site value as if they were interchangeable. They aren't. If your terms are loose, your model will be loose, and then your legal drafting, appeals process, and revenue estimates will all inherit the same weakness.

What you are actually trying to measure

Start with the broadest category. Total property value is the market value of the parcel as transacted, including the land and whatever has been built on it. That may be useful for mortgage lending or transfer taxation, but it's too broad for a land-focused fiscal instrument.

Then split it:

| Term | What it means in practice | Why ministries care |

|---|---|---|

| Land value | The value of the underlying land apart from buildings and other improvements | It's the base for land-focused taxation and value capture |

| Improvement value | The value created by buildings, utilities, drainage, grading, and other man-made additions | Taxing this can discourage maintenance and construction |

| Site value | The value of a specific parcel in its actual legal and locational context | This is often the operational target for recurring levies |

A useful test is simple. If the structure burned down tomorrow, what part of the market value would still remain because of the location, permissions, access, surrounding services, and natural attributes of the parcel? That remaining value is the territory you're trying to isolate.

Why land rent matters for tax design

Once ministries move from valuation to tax design, the next concept is land rent. That's the recurring economic value a site commands because it occupies a valuable location within a legal and social system. It's closely tied to accessibility, infrastructure, agglomeration, environmental quality, and development rights.

For teams working through this concept, Unitism's glossary entry on economic rent is a useful reference because it clarifies the difference between returns to productive effort and returns tied to exclusive control of a scarce opportunity.

A valuation model built for fiscal reform should identify the value of the site itself, not reward or punish the owner for how much concrete, steel, or paint happens to sit on top of it.

The distinction that improves policy choices

This distinction becomes practical when ministries decide what behavior the tax system should encourage.

- If you tax improvements heavily, owners may defer maintenance, hold back redevelopment, or build less intensively than planning policy would prefer.

- If you tax site value more directly, owners have a stronger incentive to use well-located land efficiently.

- If you fail to separate nature from capital, you'll struggle to explain why some parcels rise in value because of public investment, water access, scenic advantage, or reduced climate exposure rather than private effort.

That last point matters more than it used to. Modern reform debates increasingly have to address not only land in the narrow cadastral sense, but also the value effects of natural assets and risks attached to it.

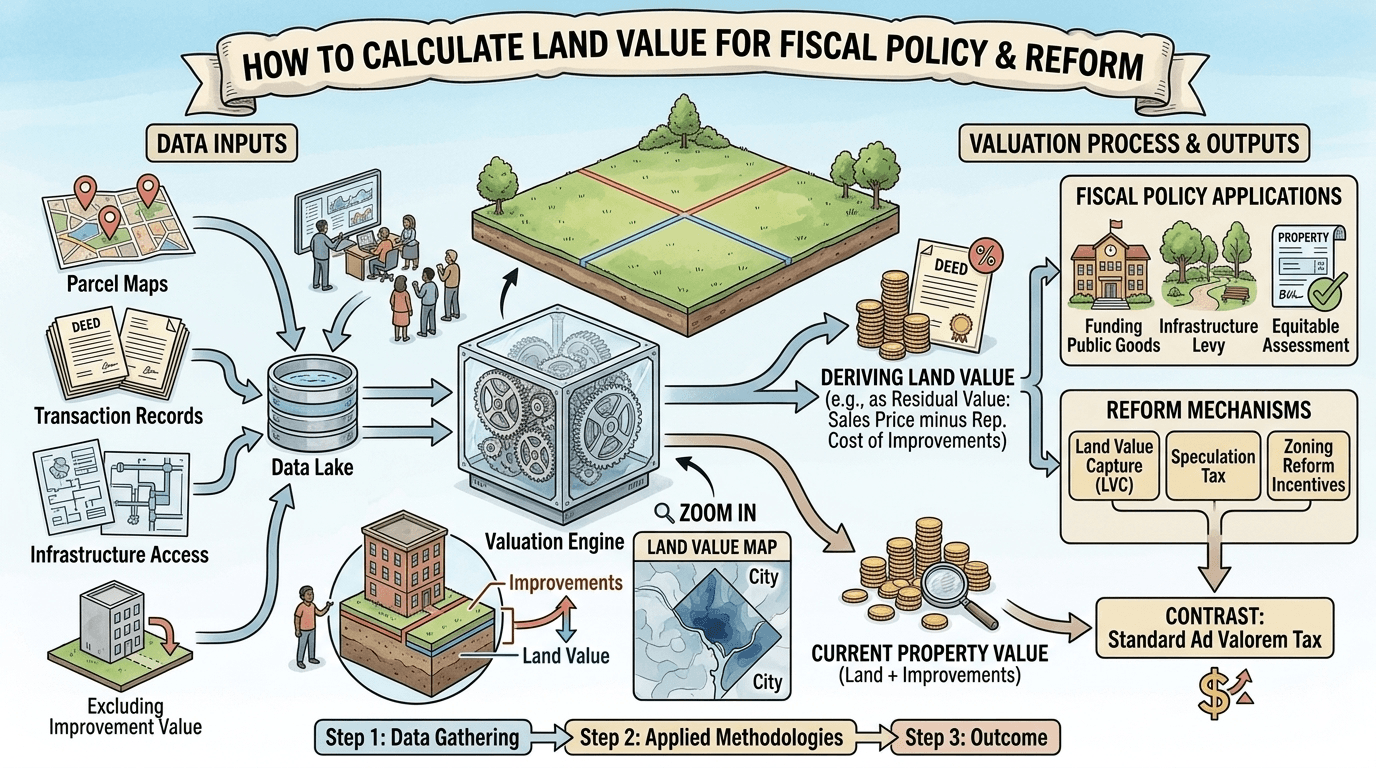

Choosing Your Primary Valuation Approach

No single method works everywhere. The right way to calculate land value depends on what data you have, what legal standard you need to satisfy, and whether you are valuing one parcel, a development site, or an entire tax base.

A good policy team treats valuation methods as a toolkit, not a doctrine. In some districts, direct land sales are strong enough to anchor values. In others, redevelopment potential matters more than vacant land transactions. In many places, you'll need to blend methods and document why.

When direct land sales exist

The sales comparison approach is still the cleanest starting point when you have enough unimproved land transactions.

You identify comparable parcels, normalize them to a common valuation date, and adjust for differences such as zoning, access, parcel shape, topography, and utility connections. If the market is active and the comparables are substantially similar, this gives assessors and courts something they understand intuitively.

What works:

- Recent unimproved sales in the same submarket

- Clear adjustment logic tied to observable parcel attributes

- Segmentation by land use class so urban commercial land isn't blended with fringe residential plots

What usually fails:

- Thin markets where a handful of sales dominate

- Comps drawn from parcels with very different legal permissions

- Manual adjustments that can't be replicated at scale

For teams that want a practical primer on site-level appraisal thinking, the Domus guide to site valuation is a helpful external reference, especially when training non-specialists who need to understand the differences between valuation contexts.

When development potential drives value

The Residual Land Valuation, or RLV, approach is essential for sites where the market value of the land depends mainly on what can legally and feasibly be built there.

The logic is straightforward. Land value equals the expected value of the completed project minus development costs and the developer's required margin. In other words, the projected costs of the development plus the developer's required margin are subtracted from projected revenue to arrive at the residual land value, as described in the Altus Group discussion of land valuations.2 The exact share that land represents of gross development value, and the size of the developer's margin, vary by market and project and should be drawn from local feasibility evidence rather than assumed.

That makes RLV particularly useful for:

- Upzoning analysis

- Betterment or land-value capture design

- Feasibility testing for infill and redevelopment sites

- Testing whether assessed site values are economically plausible

If your model says a parcel has a very high site value but no feasible project can support paying that amount for land, the valuation team should stop and examine its assumptions.

The biggest problems in RLV are rarely mathematical. They sit in the assumptions. Ministries often inherit optimistic sale values, understated soft costs, or no explicit treatment of delay and approval risk. A robust RLV model needs scenario testing, not a single spreadsheet output.

When you need an annual value rather than a capital value

Some reforms don't need a one-time capital value. They need a recurring annual site value or a site-rental estimate that can support levy design.

That's where capitalization of ground rent becomes useful. If a parcel generates, or could generate, a stable annual ground rent, analysts can capitalize that stream into a land value. The reverse also matters for public finance. If you begin with a capital land value, you may need to convert it back into an annual figure for rate-setting, incidence analysis, and public communication.

This approach works best when:

- There is a clear and defensible annual rent concept.

- The chosen capitalization rate is documented and segment-specific.

- Vacancy, risk, and legal constraints are handled explicitly.

Where teams get into trouble is pretending the capitalization rate is self-evident. It isn't. It needs justification because it drives the annual liability implied by the valuation system.

When only improved property sales are available

In many cities, vacant land sales are too scarce to anchor the tax base. Then ministries often use an extraction method. You begin with sales of improved properties and estimate the contribution of the building and other improvements, leaving the residual attributed to land.

This can be practical, but it's vulnerable to building-cost errors and depreciation assumptions. It also tends to work poorly where informal construction, inconsistent records, or major quality variation make improvement values hard to estimate with confidence.

A simple decision guide helps:

| Situation | Most suitable lead method | Main caution |

|---|---|---|

| Active market for comparable vacant sites | Sales comparison | Don't overstate similarity between parcels |

| Redevelopment or upzoning context | Residual land valuation | Feasibility assumptions can distort outcomes |

| Need for annual recurring tax base | Ground rent capitalization | Capitalization rate must be justified |

| Improved sales dominate, vacant sales scarce | Extraction method | Building-value estimates can contaminate land estimates |

The practical answer to “how do we calculate land value?” is often, “with the least distorted method the market and data will support, plus a clear audit trail.”

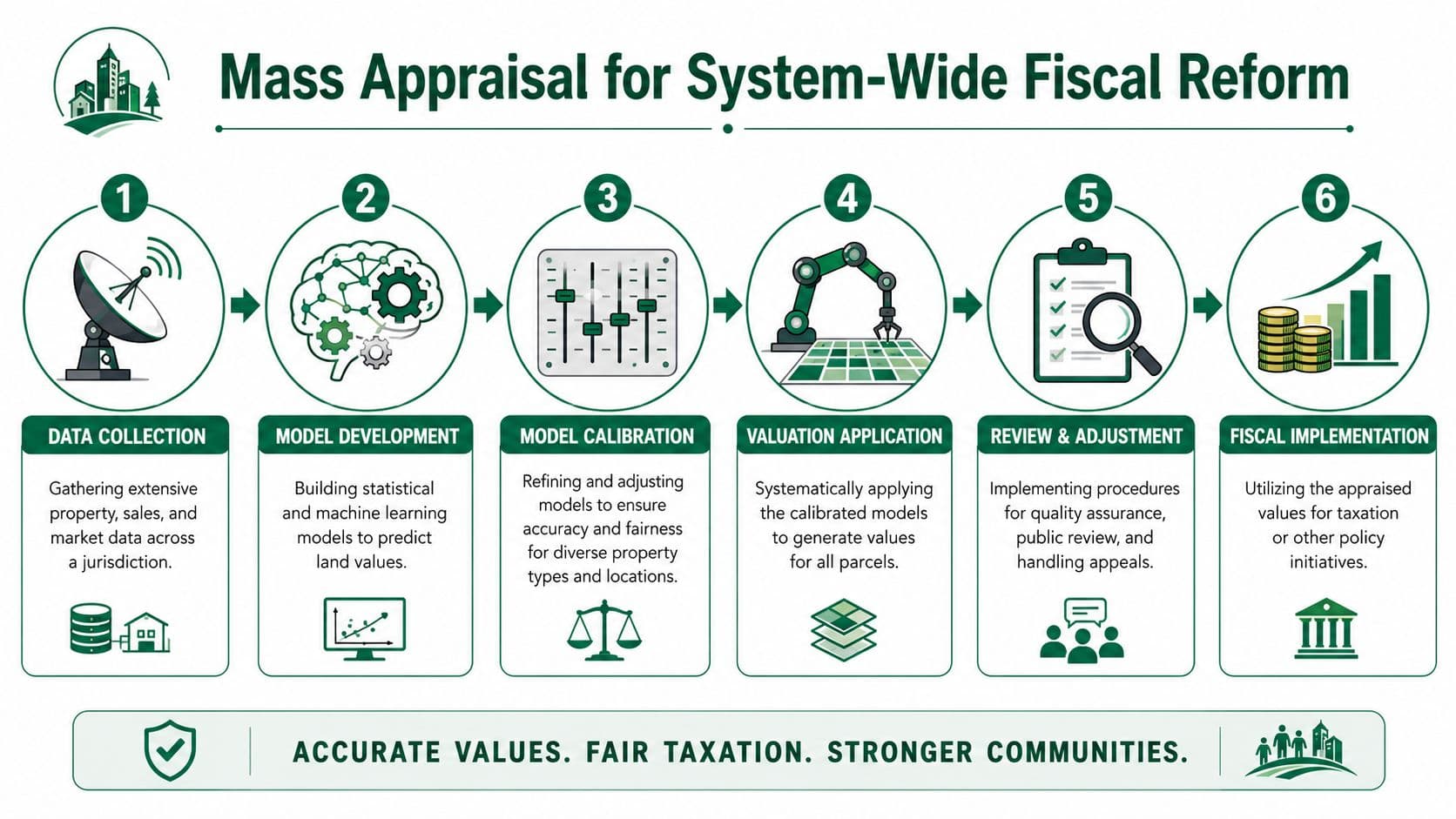

Mass Appraisal for System-Wide Fiscal Reform

A ministry can value a few strategic parcels by hand. It can't run a recurring national or citywide land tax that way. For that, you need computer-assisted mass appraisal, usually called CAMA, supported by GIS, parcel data, and statistical modeling.

Mass appraisal doesn't mean abandoning valuation judgment. It means standardizing it, testing it, and applying it consistently across the roll.

What a workable CAMA pipeline looks like

A policy-ready system usually follows a sequence like this:

- Build the parcel base first. Parcel identifiers, boundaries, land use class, zoning, access, and infrastructure status need to be clean enough to model.

- Standardize transaction inputs. Sales must be screened for non-market transfers, unusual terms, and timing differences.

- Create locational variables. Travel time, transit access, service proximity, neighborhood characteristics, and environmental constraints matter because site value is spatial.

- Model the land component. Advanced national work has paired k-means clustering and gradient-boosted trees with hedonic regression to estimate parcel-level land values across residential, commercial, industrial, and agricultural uses, as described in the BEA working paper on parcel-level land-value estimation.3

- Review spatial outputs. Maps often reveal where the model is wrong before summary tables do.

- Set up a rerun process. A tax base that can't be updated is an expiring asset.

For ministries handling raw records, financial statements, and property datasets from multiple agencies, a tool like real estate financial report analysis can help analysts structure and inspect documentation quickly before values feed into the formal model.

How to keep an automated system defensible

The strongest argument for CAMA is consistency. The strongest argument against a bad CAMA system is also consistency. If the model is wrong, it can be wrong everywhere.

The benchmark worth keeping in mind is qualitative rather than a fixed number: well-built CAMA systems aim for land value estimates that are reasonably close to observed sales, but accuracy depends heavily on having sufficient sales data and on regular validation. Standards bodies such as the International Association of Assessing Officers publish ratio-study measures (for example, the coefficient of dispersion) precisely so that jurisdictions can test and document how close their models come to market evidence. A ministry does not need a perfect model. It needs one that is transparent, regularly tested, and operationally fair.

Operational test: If assessors can't explain why adjacent parcels differ in value, the public appeal system will explain it for them.

Three safeguards matter most:

- Segment the market sensibly. Dense commercial cores, suburban residential zones, and peri-urban agricultural land shouldn't be forced into one valuation logic.

- Check for outliers and influential sales. Thin high-value transactions can distort gradients if you let them dominate.

- Publish value maps and methods. Public understanding improves when taxpayers can see the pattern rather than only the bill. A visual exploration tool such as a land value map can help ministries test whether modeled gradients align with known local conditions.

A modern mass appraisal system should be reproducible. If the model depends on one expert's undocumented intuition, it isn't a system yet.

Refining Valuations with Adjustments and Externalities

A base model gets you into the right neighborhood. Adjustments determine whether the valuation is credible parcel by parcel. Many tax reforms become fragile at this stage, because the raw estimate may be directionally correct while still being unfair in the cases taxpayers care about most.

The adjustments that usually matter most

In practice, ministries should maintain a disciplined adjustment schedule rather than allowing ad hoc assessor discretion. The important categories are familiar, but they need to be formalized.

- Zoning and legal use. A parcel with broader development rights has a different economic capacity from one restricted to low-intensity use.

- Access and infrastructure. Frontage, road quality, transit access, sewer, water, and digital connectivity can all alter site value materially.

- Physical constraints. Shape, slope, contamination, easements, setback limits, and drainage issues can reduce usable development area.

- Locational spillovers. Proximity to employment centers, parks, schools, logistics corridors, or nuisance uses changes market behavior.

The discipline is to tie each adjustment to evidence that can be documented and repeated. A ministry should be able to say not only that a factor matters, but how it enters the model and under what conditions it is applied.

A simple governance rule helps. Keep a central adjustment manual. If local assessors are making exceptions in email threads or spreadsheet comments, consistency will erode quickly.

Bringing nature into the model

Standard land valuation guides often miss a growing issue. Some of what markets capitalize into land prices is not just land in the narrow legal sense, but natural capital and environmental exposure attached to a location.

That includes positive features such as green-space access, water frontage, urban cooling, and ecological amenity. It also includes negative features such as flood exposure, erosion risk, heat vulnerability, and pollution burdens.

The direction of travel in the evidence is clear: environmental risk is capitalized into land prices. One spatial-econometric study of Hangzhou found that, holding other factors constant, residential land plots at high risk of flooding carried a price discount of roughly 8.6 percent, illustrating why incorporating natural capital variables is increasingly important for fair assessment, especially in climate-vulnerable regions.4 These themes are explored further in this paper on measuring land value.

That doesn't mean every ministry should immediately monetize every ecosystem service. It does mean the valuation system should stop pretending environmental conditions are outside the tax base when buyers and developers plainly price them in.

A parcel beside a new park and a parcel exposed to chronic flood risk are not equivalent sites, even if their lot sizes match and their buildings don't.

A workable adjustment framework

For most administrations, the practical path is staged:

| Adjustment layer | Early-stage approach | Mature approach |

|---|---|---|

| Legal attributes | Use zoning class and permitted use | Model intensity, conditional permissions, and development constraints |

| Access and services | Add binary service indicators | Add network-based accessibility measures |

| Physical constraints | Flag severe limitations | Quantify impact on usable area and development potential |

| Environmental factors | Include major hazards and amenities qualitatively | Integrate them as modeled variables in mass appraisal |

This staged approach matters because ministries often wait for perfect data before addressing externalities at all. That's the wrong instinct. Start with the factors you can defend, then expand the model as evidence and data quality improve.

From Valuation Data to Policy Implementation

A technically good valuation system can still fail as policy if it isn't translated into legislation, administration, and public communication. Ministries often spend months refining parcel values and only later discover that the reform needs annual liability rules, appeal procedures, cadastre integration, exemptions policy, and billing workflows that were never designed.

Turning capital values into recurring revenue inputs

This is the gap that appears most often in public finance work. Many guides explain how to estimate market value, but they stop before showing how to derive a recurring annual value suitable for a site-based charge.

That gap is widely observed in practice. A common weakness in existing guidance is the translation of appraised land values into recurring annual rental figures for instruments like site-value taxation; many practitioner guides focus on appraisal methods but offer little systematic process for selecting and justifying a capitalization rate, leaving policymakers without a clear route to stable reform. A practitioner discussion of this issue appears in this review of land value guidance gaps.

For ministries, the operational sequence is usually:

- Establish the capital site value base through one or more defensible valuation methods.

- Define the annual value concept clearly in law or regulation.

- Document capitalization assumptions by segment rather than relying on one blanket figure.

- Stress-test liabilities against appeals risk, distributional effects, and payment capacity.

- Phase implementation if valuation quality varies across the jurisdiction.

If the legal framework says “tax land value” but the administration cannot explain how that becomes a yearly bill, the reform will be challenged from the start.

What ministries must get right before launch

The final work is administrative, not academic.

- Legal clarity matters. The statute must define the base, valuation date, update process, and appeal grounds with precision.

- Cadastre and tax roll integration matters. If parcel IDs don't match across agencies, billing and compliance break down.

- Communication matters. Taxpayers need to know why a site value changed and what evidence supports it.

- Transition design matters. Sudden shifts without phasing, offsets, or clear treatment of existing taxes create avoidable opposition.

For teams considering the broader design logic behind these reforms, this primer on land value capture explained is a useful reference for framing how valuation links to public revenue tools.

A ministry doesn't need a perfect model before it starts. It does need a valuation system that is coherent, governable, and capable of improvement. That's what turns land valuation from an appraisal exercise into fiscal infrastructure.

Frequently Asked Questions

How do you separate land value from building value when most sales include both?

When you only have improved property sales, the most common route is the extraction method, where you start from the total sale price, estimate the depreciated contribution of the building and other improvements, and treat the remaining residual as land value. It works in practice, but it’s sensitive to construction-cost and depreciation assumptions, so it tends to be weakest where construction is informal, records are inconsistent, or building quality varies a lot. A good test is to ask what value would remain if the structure burned down tomorrow, since whatever persists because of location, permissions, access, and surrounding services is the land component you’re trying to isolate.

Which land valuation method should a ministry choose for a recurring tax base?

There’s no single method that fits every jurisdiction, so the better question is which approach the available data and legal standard can actually support. If you have an active market for comparable vacant parcels, sales comparison is the cleanest anchor; in redevelopment or upzoning contexts, residual land valuation is more appropriate; when you need an annual figure for rate-setting, ground rent capitalization works best; and when vacant sales are scarce, the extraction method may be your only realistic option. For a system-wide tax base, ministries generally need computer-assisted mass appraisal that blends these methods, applies them consistently, and keeps a clear audit trail for every value.

What do ministries most often overlook when turning land valuations into actual policy?

The biggest gap is the step between a capital value estimate and a recurring annual bill, because many guides explain how to appraise a parcel but stop short of showing how to convert that into a defensible site-value charge. In practice this means defining the annual value concept in law, documenting and justifying a capitalization rate by market segment rather than using one blanket figure, and stress-testing liabilities against appeals risk and payment capacity. Beyond the math, reforms also fail when legal definitions are vague, cadastre and tax roll records don’t match across agencies, or the transition lacks phasing and clear public communication, so the administrative groundwork matters as much as the valuation itself.

If your team is designing land valuation for tax reform, Unitism® provides support on valuation frameworks, site-rental estimation, policy design, implementation planning, and public communication so ministries can move from concept to an operational land-based revenue system.