Explore the history of the window tax in England. Learn how its failure provides critical lessons for modern land-value capture and equitable tax reform today.

July 6, 2026

Window Tax in England: A Lesson in Modern Tax Reform

Explore the history of the window tax in England. Learn how its failure provides critical lessons for modern land-value capture and equitable tax reform today.

A tax assessor walks down a Georgian street in England, counting windows from the outside. Years later, the same street shows the policy's verdict in brick: openings sealed, rooms darkened, and a public revenue tool turned into an architectural scar.

Table of Contents

- Why a 300-Year-Old Tax Still Matters Today

- The Mechanics of the Window Tax

- The Societal Costs of Taxing Daylight

- Why Taxing Windows Failed Where Land Value Succeeds

- Global Precedents for Smarter Property Taxation

- The Enduring Legacy for 21st Century Reform

Why a 300-Year-Old Tax Still Matters Today

The most memorable image from the window tax in England isn't a ledger. It's a wall where a window used to be.

That image matters because it shows tax policy in physical form. When governments tax something people build, improve, or maintain, people often stop building, improving, or maintaining it. In this case, the taxed item was a basic feature of habitable housing: access to light and air.

The policy has become folklore, but folklore understates the lesson. The window tax wasn't merely quirky or old-fashioned. It was a long-running demonstration that the tax base itself can shape architecture, health, and household behavior far more powerfully than lawmakers expect.

A street-level lesson in economic history

England's streets preserved the evidence. Bricked-up openings still tell us that people didn't passively absorb tax design. They adapted to it. Some adaptations were financially rational and socially destructive at the same time.

That's why this episode still matters to a modern finance ministry facing housing shortages, weak productivity, and pressure to raise revenue without choking investment. The core question hasn't changed: what should the state tax if it wants revenue without discouraging useful activity?

Practical rule: If a tax makes people remove value from homes, shops, or workplaces, the tax base is probably wrong.

The deeper importance of the window tax is conceptual. It sits near the boundary between taxing wealth signals and taxing actual economic capacity. Windows looked like a visible marker of prosperity, so they became an easy administrative proxy. But a visible proxy is not the same as a sound base.

Modern land reform debates return to this distinction. A useful primer on the tradition that separates land from labor and capital appears in this Georgism glossary entry. That framework helps explain why the window tax failed, and why the better target is often the underlying site value created by location, infrastructure, and community growth.

Why this matters now

A ministry designing property taxation in the present should read the window tax as a warning against taxing improvements. Windows were productive capital in ordinary life. They made homes healthier and more usable.

Taxing them sent exactly the wrong signal. It rewarded concealment, not development. It penalized better housing, not idle advantage. And it did so for generations.

The Mechanics of the Window Tax

A tax collector did not need a ledger, an income declaration, or a surveyor's estimate of rental value. He could stand in the street and count. That administrative convenience explains why the window tax survived for so long. It also explains why it became a textbook example of a tax that was easy to enforce and costly to live under.

How the tax began

The window tax was introduced in 1696 under William III as a revenue measure in wartime Britain, and it remained in force until 1851, as outlined by the UK National Archives overview of the tax. The state chose windows because they were visible and difficult to hide at scale. In administrative terms, this was a clever proxy for household means.

In economic terms, it was a poor tax base.

A window is part of the building's usefulness. It improves light, air, and the quality of occupation. Taxing it meant taxing an improvement to capital, not an underlying source of passive economic advantage. That distinction matters. Good tax systems try to raise revenue from bases that do not shrink when people build, repair, or upgrade. Bad ones do the opposite.

What households paid

By the mid-eighteenth century, the levy had become a banded charge tied to the number of windows in a dwelling.

| Window Tax Bands and Rates (1747) | Tax per Window |

|---|---|

| 9 or fewer windows | No tax |

| 10 to 14 windows | 6d |

| 15 to 19 windows | 9d |

| 20+ windows | 1s |

The structure did not remain fixed. Parliament revised the thresholds and increased the burden repeatedly over time. The important point is not the exact sequence of rate changes. It is the logic of the schedule. Liability rose in steps, and those steps changed household behavior.

That is a familiar problem in public finance.

Why the notch mattered

A banded tax of this kind creates what economists call a notch. Once a property crosses a threshold, the tax bill can jump sharply rather than rise smoothly with the added feature. Under that rule, the decision to add one more window was no longer a simple question of comfort or utility. It became a tax planning problem.

A ministry analyst would recognize the incentive immediately. If an extra improvement triggers a disproportionate increase in liability, rational owners will stop short of the threshold, alter designs to avoid it, or remove the taxable feature altogether. The tax code then starts to shape the building stock.

This is the broader lesson. States often reach for visible proxies because they are cheap to administer. But a visible proxy can be a destructive base if it falls on productive capital. The window tax looked practical from the street and wasteful in the national accounts.

The contrast with land is sharp. A tax on unimproved site value does not punish the addition of windows, rooms, workshops, or better materials. It collects part of the value created by location and public investment while leaving construction and maintenance less distorted. That is the central efficiency argument in favor of taxation and efficiency in property reform. The failure of the window tax shows the same principle in reverse. Once the state taxes improvements, it invites underinvestment by design.

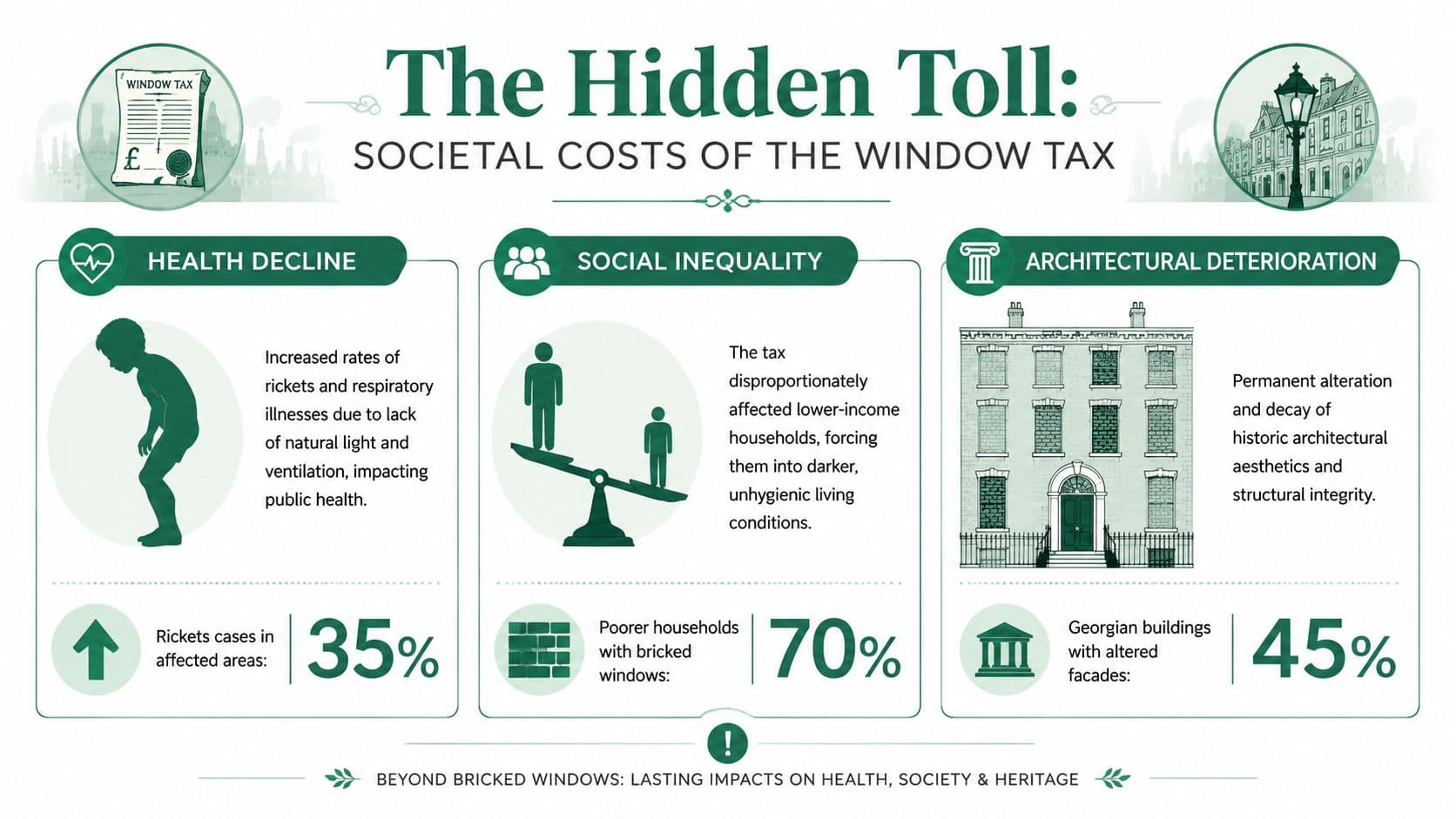

The Societal Costs of Taxing Daylight

The window tax did more than alter tax returns. It altered houses, streets, and lungs.

When avoidance changes the built environment

Once the tax penalty attached to windows, households and builders responded in the obvious way. They boarded up openings, reduced them, or designed around them. That response degraded architecture, but aesthetics were only the first loss.

The more serious point is institutional. A state that taxes visible improvements trains people to subtract value from the built environment. A better room becomes a cost. Ventilation becomes a liability. A façade becomes an accounting problem.

This is why the window tax in England belongs in any serious discussion of housing policy. It shows that bad taxation can create poor housing without a formal ban, a zoning code, or an explicit design mandate. Price signals alone can do the damage.

The public health cost

The best verified evidence goes beyond the familiar phrase “dark houses.” The tax created incentives to close off ventilation, and that had measurable health consequences.

According to a Lincoln Institute working paper on the window tax, the tax created a deadweight loss equal to 13.6% of total tax revenue, with an excess burden of 62% for households near the tax thresholds. The same source links the widespread boarding of windows to higher rates of respiratory disease and tuberculosis in affected households.

That changes how the story should be told. This wasn't only a symbolic “tax on light.” It was a tax design that pushed families toward reduced airflow inside homes. The health channel ran through ventilation as much as illumination.

Bad tax design can move from the treasury into the body. In this case, the path ran through the walls of the home.

A short explainer on deadweight loss helps make sense of why this matters. Revenue alone doesn't measure policy quality. The full cost includes the useful activity people abandon to avoid the tax.

Why economists care about the excess burden

The excess burden figure matters because it captures waste generated by distorted choices. For households near the thresholds, the tax didn't just transfer resources to the state. It imposed a large additional welfare cost by making one extra window disproportionately expensive.

That's the hidden toll. The government collected revenue, but society paid more than the revenue raised. And the overpayment wasn't abstract. It appeared as sealed rooms, reduced habitability, and avoidable illness.

Three lessons stand out:

- Taxing improvements invites deterioration. When the state taxes a beneficial feature of a building, some owners will remove or suppress that feature.

- Thresholds magnify avoidance. Sharp jumps in liability produce stronger behavioral responses than smooth schedules.

- Health effects can follow fiscal design. Housing taxes don't stay in spreadsheets. They can shape air quality, daylight, and disease exposure.

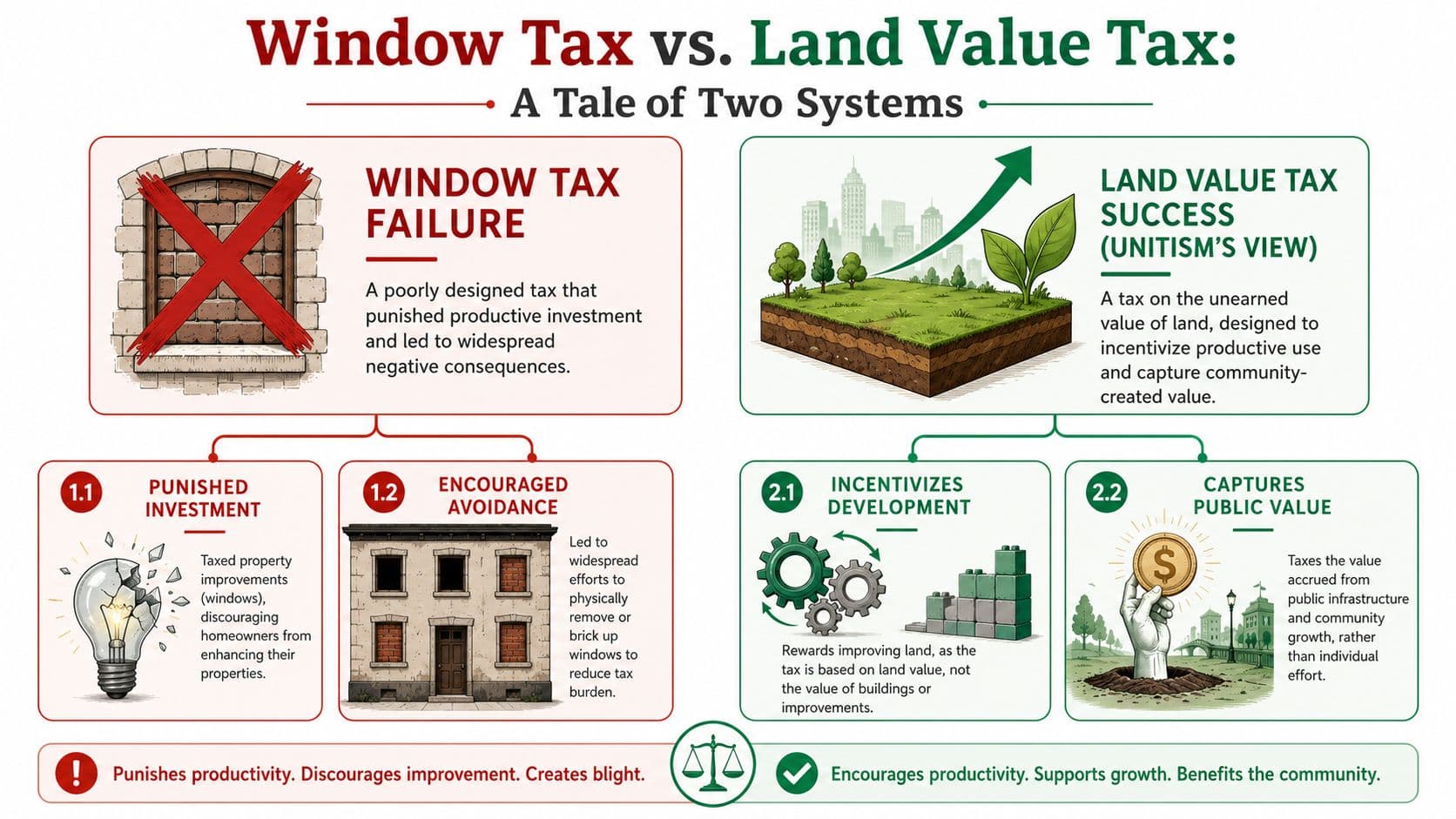

Why Taxing Windows Failed Where Land Value Succeeds

The window tax failed because it taxed the wrong thing.

The wrong base

Windows are capital improvements. Someone pays to install them, maintain them, and use them to make a building more livable. Taxing windows means taxing an owner's decision to improve a structure.

That is the core design error. The state wanted a practical proxy for property wealth, but it chose a visible component of the building rather than the underlying site. It taxed what people added, not what they received from location.

The distinction matters in public finance. Land and improvements behave differently. A building extension, renovated façade, or additional window results from private effort and investment. Site value often reflects location advantages created by population density, public services, infrastructure, and legal permission.

A tax system that confuses those categories penalizes the part of the property market governments usually want more of: maintenance, construction, and adaptation.

What land value taxation does differently

A Lincoln Institute article on the window tax and land value taxation makes the underappreciated point clearly: the window tax functioned as a de facto land-value tax proxy and failed because it taxed visible capital rather than unimproved site value. That failure produced a 62% excess burden at tax notches, and the same article notes that modern land-value taxation in places such as Denmark and Singapore is designed to avoid that distortion by separating land value from improvements.

That separation is the critical reform principle.

Under a land value tax, adding windows, improving insulation, repairing a roof, or upgrading a shopfront doesn't increase liability merely because the owner made the property better. The tax base is the location value of the site, not the privately created improvement on top of it.

Key distinction: A tax on buildings asks, “What did you build?” A tax on land asks, “What value does this location hold, regardless of what you build on it?”

For readers who want the conceptual definition, this land value tax glossary entry gives the cleanest statement of the principle.

A finance ministry test

A modern finance ministry can apply a simple test before approving any property tax reform.

| Policy question | Tax on windows or buildings | Tax on unimproved land value |

|---|---|---|

| Does it penalize property improvements? | Yes | No, not directly |

| Does it encourage concealment or underinvestment? | Often | Less so by design |

| Does it capture location value created by the community? | Poorly | More directly |

| Does it align with better housing quality? | Weakly | More strongly |

The historical case is more than a cautionary tale. It becomes a diagnostic tool. If the proposed tax base rises when an owner adds useful capital, the reform likely repeats the logic of the window tax in another form.

That lesson is especially relevant in housing systems burdened by underbuilding and high land prices. Taxing improvements suppresses supply quality and renovation. Taxing site value, by contrast, is aimed at the unearned component of property value that owners receive from place rather than from their own construction effort.

The broader opportunity

The enduring insight isn't just that the window tax was cruel or clumsy. It's that it accidentally illuminated the correct alternative.

Once policymakers see why the tax failed, they can frame reform around a sharper principle: tax what the community creates, not what households and firms add. That means shifting the base away from productive capital and toward land value.

Global Precedents for Smarter Property Taxation

The historical argument would be weaker if it ended in the archive. It doesn't. The same sources that diagnose the failure of the window tax also point toward jurisdictions that structured property taxation around a cleaner distinction between land and improvements.

What the historical lesson points toward

The earlier Lincoln Institute analysis identifies Denmark and Singapore as places where modern land-value taxation is designed to avoid the distortion created by taxing visible capital. The point isn't that every jurisdiction uses the same model. It's that serious reform efforts increasingly start from the same economic insight: don't punish improvements if your goal is a healthier built environment and a broader, less distortionary base.

That matters because ministries often inherit property tax systems assembled from administrative convenience rather than first principles. Assessment practice, legacy exemptions, and political compromise can leave governments taxing transactions, structures, and renovations more heavily than they tax the locational value that public action helps create.

A cleaner system reverses that emphasis.

What ministries can take from current practice

The practical lesson from international precedent isn't a plug-and-play statute. It's a sequence of design choices.

- Separate land from improvements. Valuation has to distinguish site value from building value. Without that separation, policymakers can't stop taxing productive capital by accident.

- Reduce taxes that discourage construction. If a city wants better housing, it shouldn't raise liability just because an owner adds usable space, more light, or a more durable structure.

- Treat location value as a public revenue base. Infrastructure, transit access, neighborhood demand, and legal permission all help create site value. Capturing part of that value is more coherent than taxing maintenance.

Some jurisdictions move gradually. Others use split-rate systems or partial land-value capture instruments. The administrative path can differ, but the strategic direction remains the same: move the tax burden off buildings and onto land.

Ministries don't need to choose between revenue and development. They need to choose a base that doesn't make the two goals collide.

For policymakers exploring implementation pathways, this overview of property tax reform approaches is a practical companion to the historical lesson.

The larger implication is hopeful. The window tax showed how a bad base can darken homes. Modern land-focused systems show how a better base can support revenue while leaving room for construction, adaptation, and healthier use of urban land.

The Enduring Legacy for 21st Century Reform

The window tax lasted long enough to leave a physical archive in brick. Its longer legacy should be analytical.

A modern tax system can't afford to ignore what that episode revealed. When governments tax the parts of property that owners create, repair, or improve, they discourage the very behavior that strong housing systems require. When they focus instead on underlying site value, they move closer to a base that doesn't punish construction quality or basic livability.

That isn't just a historical opinion. It's a policy design principle. A ministry facing today's housing and fiscal pressures should ask, in every reform memo, whether the proposed base taxes productive effort or captures socially created location value.

The right way to study this kind of question is with discipline rather than anecdote. For policy teams building evidence standards into reform work, Contesimal's guide to the systematic literature review process is a useful model for evaluating competing claims, historical evidence, and implementation options.

England repealed the window tax after public pressure connected blocked light and poor health. Today's policymakers have the advantage of hindsight. They can do more than repeal old mistakes. They can design taxes that reward building, support healthier cities, and align public revenue with the value that land and community generate together.

The bricked-up window is still speaking. Finance ministries should listen.

If your government, city, or policy team is exploring how to shift taxes off work and buildings and toward land and nature, Unitism® offers research, valuation frameworks, policy design, implementation support, and public education grounded in land economics. It's a strong starting point for turning historical lessons like the window tax into practical reform.