Complete guide to property tax reform: models, impacts, and implementation roadmaps for equitable growth in 2026.

June 26, 2026

Property Tax Reform: Guide to Models, Impacts & Roadmaps

Complete guide to property tax reform: models, impacts, and implementation roadmaps for equitable growth in 2026.

Property tax is often treated as an administrative necessity. In practice, it's one of the clearest signals a government sends about what it wants more of and what it wants less of. The surprising part is that many systems still tax buildings and improvements heavily while leaving the gains from scarce, well-located land comparatively undertaxed, even though a technically superior reform path exists in the form of split-rate taxation that taxes land more heavily and buildings more lightly, encouraging construction while discouraging speculative holding, according to the IMF's analysis of split-rate property taxation.1

For finance ministries, municipal treasuries, and housing policymakers, that distinction matters. A tax on labor can suppress work. A tax on capital can suppress investment. A tax on land value, by contrast, targets a base that governments and communities themselves help create through infrastructure, planning, public safety, and agglomeration. That makes property tax reform not just a revenue question, but a structural reform agenda.

Table of Contents

- Why Property Tax Reform Matters Now

- The Economic Foundation of Modern Tax Reform

- A Comparative Menu of Reform Options

- Evidence and Precedents from Around the World

- Assessing Fiscal and Distributional Impacts

- A Phased Path to Practical Implementation

- Frequently Asked Questions for Policymakers

- How do we protect cash-poor homeowners

- Can local governments implement reform with imperfect data

- What if reform shifts taxes onto politically vocal groups

- Should governments prefer caps exemptions or structural reform

- Is a pure land value tax always the right end state

- What should ministers or mayors ask first

Why Property Tax Reform Matters Now

Property tax reform has moved from a technical issue to a macro-critical one. Governments are asking local tax systems to support housing supply, discourage speculative landholding, and preserve stable municipal revenue at the same time. Many current systems pull in the opposite direction. They raise liability when owners build, renovate, or intensify use, while placing a lighter relative burden on land that is well located but underused.

That incentive structure is hard to defend on economic grounds.

The policy problem is larger than rate levels. It sits in the tax base itself. Under a conventional property tax, improvements and structures are taxed alongside land, even though they have different economic effects. Taxing buildings can deter investment in capital. Taxing wages and transactions can weaken labor market activity and business formation. Taxing land rents works differently because the supply of land is fixed. For governments trying to shift the burden away from productive activity and toward location-based economic rents, property tax reform is one of the few instruments available at scale.

This is why the tri-factor lens matters. Land, capital, and labor should not be taxed as if they respond in the same way. A tax system that falls too heavily on construction and too lightly on site value will tend to suppress infill, delay redevelopment, and reward passive holding in high-demand areas.

Housing costs and underused land

The timing matters because many housing markets are constrained less by the absence of demand than by the slow release and inefficient use of urban land. There is evidence that land-use regulation and housing-supply constraints, rather than construction cost or land scarcity alone, drive much of the high cost of housing in expensive markets.23 In growing cities, a large share of site value comes from public decisions and collective economic activity. Transport links, utility networks, school catchments, planning permissions, and job access all raise land values. Those gains are often capitalized into land prices before a single new unit is built.

If the tax system captures little of that uplift while continuing to tax new construction, it reinforces scarcity. Owners have a stronger incentive to wait for appreciation, and developers face a higher carrying cost once they improve the site. That is why property tax design belongs inside a serious discussion of housing affordability policy, not at its margins.

Property tax is one of the few local fiscal tools that can influence land use, investment timing, and revenue stability at the same time.

A strategic reform, not a narrow tax adjustment

Property tax also matters because local governments rely on it more than on most other own-source revenues. In OECD countries, recurrent taxes on immovable property are widely used because the base is visible, hard to move, and more stable than transaction taxes or cyclical business taxes, as documented by the OECD's analysis of property taxation.4 Stability, however, does not guarantee efficiency. A stable tax can still discourage the wrong behavior if it is applied to improvements rather than to the underlying land rent.

The practical implication is straightforward. Governments do not need to choose between fiscal stability and better incentives. They can redesign the property tax base so that local revenue remains dependable while the tax burden shifts away from productive investment and toward the location value that public action and market demand create.

That makes property tax reform a strategic component of growth policy, housing policy, and local public finance. It is one of the clearest ways to reduce taxes on capital and labor without weakening the revenue base that municipalities need to function.

The Economic Foundation of Modern Tax Reform

Modern tax reform starts with a simple distinction that many tax codes still blur. Economies generate value from land, capital, and labor. If policymakers tax each factor the same way, they get the wrong behavioral result.

Three factors, three tax effects

Land is fixed in supply. No tax can reduce the amount of land that exists. What changes is how owners use it, hold it, or withhold it.

Capital includes buildings, machinery, and other produced improvements. Taxing capital can discourage renovation, maintenance, and construction.

Labor is human effort and skill. Taxing labor can reduce work incentives and distort hiring.

Tri-factor economics makes the policy choice clearer. If a government wants less speculation and more building, it should move tax pressure away from labor and capital and toward the economic rents tied to land. Empirical studies of two-rate property taxes find that taxing land more heavily than buildings tends to stimulate construction activity.5

A useful analogy is agricultural. Tax the farmer's effort and equipment heavily, and you get less cultivation. Tax the site value created by fertile location and public access, and you don't reduce the land itself. You push the owner to use it well or transfer it to someone who will.

Why land is different

Land value often reflects an economic rent. That is, a return tied less to productive effort and more to control over a scarce location. For policymakers working through this distinction, a concise primer on economic rent in land and public finance is useful because it explains why site values rise even when the owner does little.

Here, the classic property tax can become counterproductive. It lumps together two very different bases:

-

The site itself

The location value created by nature, public investment, and surrounding activity. -

The improvement on the site

The building, retrofit, extension, or productive use added by owners and investors. -

The occupant's effort

The enterprise, labor, or service that makes the property economically active.

A tax system that doesn't separate these elements can end up taxing the socially useful part more than the passive gain.

Practical rule: Tax bases should align with policy goals. If the goal is more housing and investment, don't tax new floorspace as if it were a social cost.

That principle doesn't mean every jurisdiction should jump immediately to a pure land value tax. It does mean governments should understand what they're currently taxing and why. Once officials see the difference between taxing land rents and taxing productive activity, the logic of modern property tax reform becomes much harder to ignore.

A Comparative Menu of Reform Options

Policymakers rarely choose between a perfect status quo and a perfect reform. They choose among imperfect, administratively bounded options. The right design depends on valuation capacity, legal authority, political tolerance for redistribution, and the government's objectives.

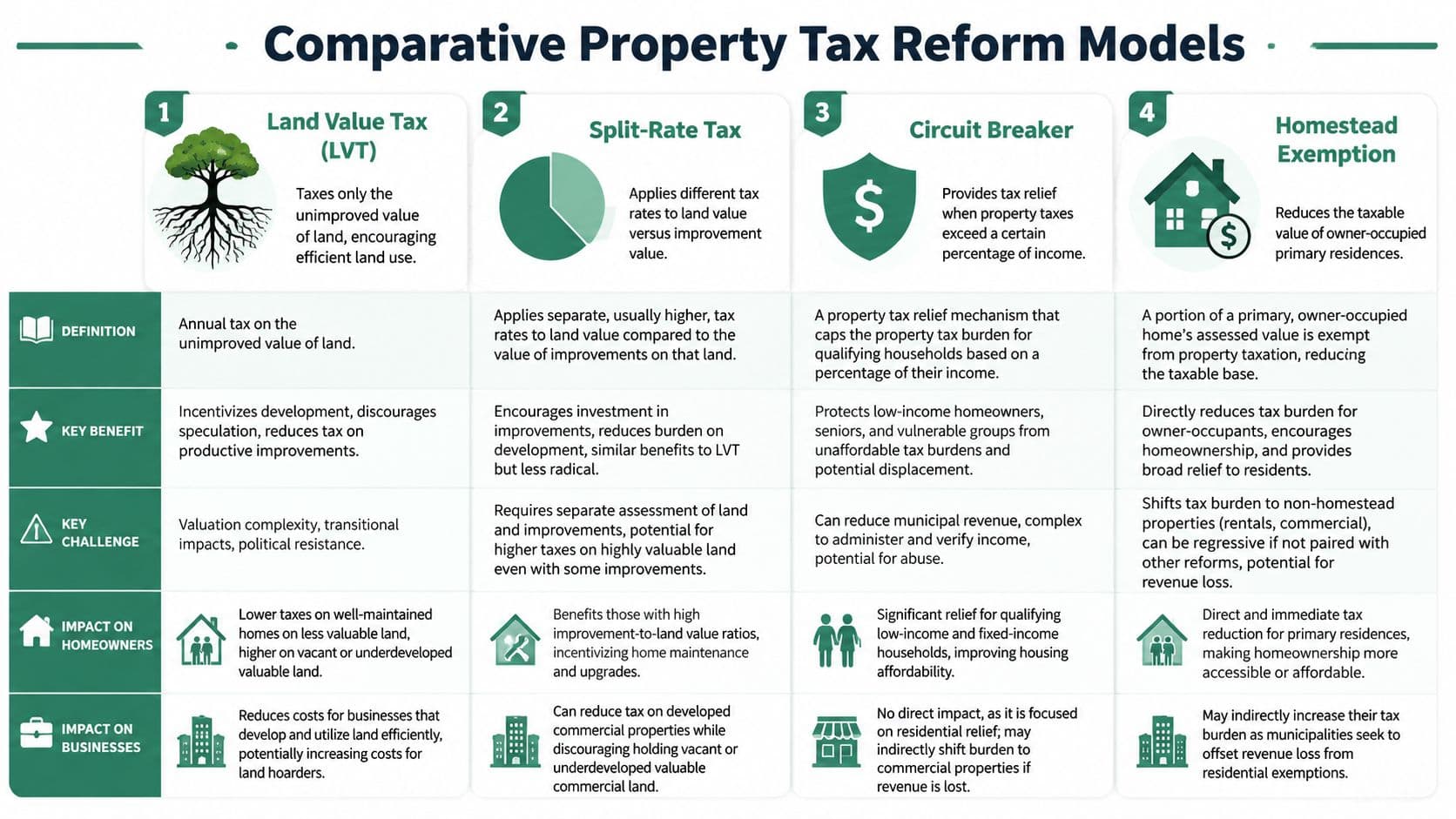

Four models policymakers actually use

Land value tax

A land value tax applies the tax only to the unimproved value of land. Buildings are excluded from the base. Economically, this is the cleanest option if the government wants to stop taxing construction and focus fully on location value.

Its strength is conceptual clarity. Owners pay for exclusive control over a scarce site, not for building on it. Its weakness is administrative and political. Assessors must isolate site value reliably, and some owners of high-value land in prime locations will face sharper tax bills.

Split-rate tax

A split-rate system taxes land and improvements separately, with a higher rate on land and a lower rate on buildings. This is often the most practical bridge between a standard property tax and a pure land value tax.

The IMF describes split-rate taxation as a technically superior approach because it separates land from buildings, discourages speculative holding through a higher tax on land, and encourages construction and densification by taxing buildings more lightly.1 The same analysis argues that this can address housing unaffordability by bringing land prices closer to construction costs and can reduce fiscal volatility by making revenues less dependent on real-estate boom-bust cycles.1 Historical experience is consistent with this: Pittsburgh's shift toward taxing land more heavily than buildings was associated with a downtown building boom.6

For many jurisdictions, split-rate reform is the most realistic structural option because it changes incentives without requiring a wholesale redesign of every relief program at once.

Circuit breakers

A circuit breaker limits property tax liability for eligible households based on income. This is a relief mechanism, not a tax base reform.

It's useful when governments need to protect low-income households, fixed-income retirees, or owners facing a temporary mismatch between property value and income. It doesn't solve the underlying distortion in the tax base, but it can make broader reform politically and socially viable.

Homestead exemptions

A homestead exemption reduces the taxable value of owner-occupied primary residences. It offers immediate, visible relief. It is also blunt.

Because it narrows the residential base, it can shift burden onto renters, second homes, or businesses unless paired with offsetting measures. That doesn't make it wrong. It means it should be understood as broad relief, not as a targeted affordability instrument.

Governments also use land value capture tools around infrastructure, rezoning, or public investment. These aren't always annual property taxes, but they belong in the same toolkit because they recover publicly created land value. For readers comparing those instruments to annual site-based taxation, this overview of land value capture mechanisms and trade-offs is a helpful complement.

Property Tax Reform Models at a Glance

| Reform Model | Economic Efficiency | Equity Impact | Administrative Complexity |

|---|---|---|---|

| Land value tax | High, because it doesn't penalize building activity | Depends on location patterns and relief design | High where site valuation systems are weak |

| Split-rate tax | High, with a more gradual shift than pure land taxation | Can improve fairness if paired with transition relief | Moderate to high |

| Circuit breaker | Limited effect on investment incentives | Strong for income-based protection | Moderate, because income verification matters |

| Homestead exemption | Limited structural effect | Broad homeowner relief, but often blunt | Low to moderate |

The best reform package is often hybrid. Use structural reform to improve incentives, then use targeted relief to protect households during transition.

Evidence and Precedents from Around the World

Property tax reform succeeds or fails on implementation design. The international record shows a consistent pattern. Governments can cut bills quickly, but durable reform depends on whether they also protect local revenue, improve valuation practice, and decide which tax base should carry more of the burden: land, buildings, or labor and capital elsewhere in the economy.

The strongest precedents are not those that merely reduce taxes. They are the cases that clarify a policy choice. Relief-focused reforms lower liabilities for selected taxpayers, often with fiscal pressure shifted to state budgets or future local service adjustments. Structural reforms change incentives by taxing economic rents tied to location more heavily than productive investment in buildings, equipment, or work. In tri-factor terms, that means shifting the tax mix away from labor and capital, and toward land.

What recent state reforms reveal

Recent U.S. state reforms are useful because they show several models operating in parallel.

In Indiana, fiscal analysts for the Indiana Legislative Services Agency estimated in HEA 1001's fiscal impact statement that the 2025 budget package would reduce local property tax collections and increase state-financed relief through a new homeowner credit and related changes.7 The policy objective was immediate taxpayer relief. The implementation risk was straightforward: local governments, schools, and other taxing units would face a smaller property tax base unless state transfers or service adjustments filled the gap.

Ohio pursued a similar relief-first direction, but through multiple bills. The Ohio Legislative Service Commission's bill analyses and fiscal notes document changes affecting school district levies, property tax calculations, and local revenue constraints across the 2025 session. The lesson is administrative as much as fiscal. Layering several targeted amendments can deliver visible relief, yet it also makes the system harder to explain, model, and administer.

Montana chose a more explicit reallocation across property classes. The Montana Department of Revenue's summary of Senate Bill 542 explains that the state paired homeowner relief with higher rates on second homes, short-term rentals, and certain higher-value commercial property.8 That approach is politically more demanding, but it is closer to rent-based taxation than across-the-board relief because it distinguishes between primary residence use and higher-value or non-owner-occupied property holdings.

Texas relied on scale and state capacity. The Texas Comptroller's explanation of the 2023 and 2024 property tax relief measures shows a package built around larger homestead exemptions, tax rate compression, and state backfilling for school finance.9 That model can produce fast, visible reductions in bills. It is less useful as a long-run template for countries or states without large surplus revenues, because temporary fiscal capacity is doing much of the policy work.

North Dakota combined relief expansion with tighter limits on future local tax growth. The North Dakota Legislative Branch record for HB 1176 and related session materials shows a broadened primary residence credit, a cap on annual increases in local property taxes, and additional relief for selected groups.10 This illustrates a common trade-off. Caps improve predictability for taxpayers, but they can also weaken the connection between assessed value growth, service demand, and municipal revenue.

The comparative point is clear. These reforms differ in politics, but they cluster into two economic strategies. One uses state resources or statutory limits to reduce current bills. The other reallocates burdens toward land and location-based rents, which is more consistent with a Unitist reform logic because it taxes what is fixed in supply rather than what governments want more of, such as housing improvement, business investment, and employment.

A broader international review reaches a similar conclusion. Jurisdictions that maintain regular reassessment, clear valuation standards, and credible local administration are better positioned to shift the tax base toward land without large compliance failures. Jurisdictions that skip those foundations often fall back on blunt exemptions, caps, or ad hoc rebates.

That is why valuation capacity matters more than reform rhetoric. Officials considering a phased shift toward land-based taxation need parcel-level methods for separating site value from improvement value. A practical starting point is this guide to calculating land value for policy design and assessment practice.

Policymakers also face an operational problem. The evidence base is dispersed across fiscal notes, assessor manuals, ministry circulars, court decisions, and budget papers. Teams that need to review dense technical material quickly may find value in tools built for use cases for academic research audio, especially when legislative staff and finance officials are comparing multiple reform models under tight deadlines.

Assessing Fiscal and Distributional Impacts

Most property tax reform proposals fail politically for one reason. Their authors talk about fairness in aggregate while taxpayers experience change individually. A government can show a more rational tax structure overall and still lose support if it doesn't identify who pays more, who pays less, and how transitions will be managed.

Winners and losers are not a side issue

New York City's experience illustrates the point with unusual clarity. In one equalization analysis, 499,400 Class 1 properties would see lower taxes, with a median cut of $1,109, while 197,200 other properties would pay more, according to the New York City Independent Budget Office analysis of reform winners and losers.11

That isn't an argument against reform. It is an argument against vague reform.

Equalization is often described as fair. But any system that changes relative burdens across classes, neighborhoods, or tenure types will create visible losses for some groups. If officials don't model those shifts openly, opponents will define the story first.

What a serious impact assessment should test

A credible assessment should answer at least four questions:

-

Who faces an immediate increase

Separate results by property class, geography, assessed value band, and owner occupancy status. -

Which increases are politically manageable

Some increases are small and diffuse. Others are concentrated on organized stakeholders with legal and media capacity. -

Where should relief be targeted

Relief should focus on hardship, not merely ownership status. That can include income-based protections, deferrals, or phased-in liability. -

How does the reform affect the budget path

Governments need year-by-year estimates, not just a long-run equilibrium picture.

A strong distributional model also helps governments communicate. It turns a general argument into a map, a list, and a transition plan. That's the difference between saying reform is fair and proving how fairness is being implemented.

If officials cannot explain who pays more and why, they are not ready to legislate.

For public engagement, scenario tools can help officials and residents understand how different designs alter burdens across parcels and neighborhoods. A practical example is a land dividend exploration tool, which illustrates how changes in the treatment of land value can reshape fiscal outcomes and public returns.

A Phased Path to Practical Implementation

Governments often delay property tax reform because they imagine a single legislative event with immediate winners and losers. In practice, the workable path is phased. Reform succeeds when valuation systems, legal architecture, fiscal buffers, and public communication move in sequence.

Phase one build the base

Start with the administrative substrate. That means the cadastre, parcel identifiers, valuation methodology, appeals process, and data integration between tax, land registry, planning, and utility records. If a jurisdiction cannot separate site value from improvement value yet, the first task isn't legislative rhetoric. It's data quality.

This phase should also establish a baseline incidence model. Officials need to know how the current system distributes burdens before they can simulate alternatives. That includes owner-occupied homes, rentals, commercial property, industrial parcels, underused sites, and exempt property.

Phase two design the transition

Once the data are usable, governments can choose the reform mix. In most cases, a phased package works better than a single reform instrument. A jurisdiction might combine a higher land rate, a lower building rate, temporary household protections, and a staged reassessment timetable.

Iowa's recent reform shows what a multi-part package looks like. The state's FY 2023 reform under Senate File 2472 was described as the largest property tax adjustment in decades.12 In FY 2023, Iowa's local property tax burden was 31.2% higher than the national average.12 The law converted the former $4,850 homestead credit into a homestead exemption, providing roughly $300 million in ongoing tax relief to homesteads, imposed a 2% levy growth cap on certain taxing authorities, and reduced the school foundation property tax levy.12 According to the Common Sense Institute analysis of Iowa's FY 2023 property tax reform, the reform cuts in half the reduction Iowa would otherwise have needed by FY 2033 to reach a median local tax burden, lowering that requirement from $1.61 billion to $810 million.12 Once fully effective in FY 2027, the same analysis projects $4.2 billion in tax savings over six years and an improvement to 16th nationally among the least-burdened local tax states.12

The lesson isn't that every jurisdiction should replicate Iowa's design. It's that reform packages work best when they combine burden relief, levy controls, and long-run structural changes in a single roadmap.

Phase three lock in credibility

Implementation fails when governments stop after enactment. The final phase is institutional.

-

Publish the methodology

Assessors should explain how land and improvements are valued and how appeals are handled. -

Sequence the burden shift

If the reform increases liability for certain classes, phase those changes over multiple tax years where feasible. -

Create automatic review points

Finance ministries and local governments should revisit incidence, collections, and appeals after the first full cycle. -

Protect service delivery

If relief measures reduce near-term revenue, the budget must identify how schools and local services remain funded.

A phased implementation plan does more than reduce political shock. It gives administrators time to learn, taxpayers time to adjust, and elected officials a defensible story about order rather than disruption.

Frequently Asked Questions for Policymakers

How do we protect cash-poor homeowners

Use targeted relief, not broad exemptions alone. Income-based circuit breakers, deferrals, or occupancy-based protections are better suited to households that are asset-rich and income-poor. A notable current example is North Carolina's House Bill 1181, filed in April 2026, which includes an emerging relief model that would cap property taxes at 6% of income for owners with 10+ years of occupancy and expand circuit-breaker eligibility for two-person households, according to the North Carolina Budget and Tax Center summary of House Bill 1181.13

Can local governments implement reform with imperfect data

Yes, but they shouldn't pretend imperfect data are sufficient forever. Governments can begin with pilot valuation work, segmented reassessments, and simplified land-improvement separation in the highest-value zones first. The objective is not instant perfection. It is a credible path from rough classification to accurate parcel-level valuation.

What if reform shifts taxes onto politically vocal groups

That will happen in some form. The answer isn't to deny it. The answer is to model it, publish it, and mitigate hardship where the policy rationale is weak. Political opposition becomes harder to manage when affected groups discover changes from their bill rather than from the government's own analysis.

Should governments prefer caps exemptions or structural reform

They solve different problems. Caps and exemptions provide relief. Structural reform changes incentives. Governments usually need both, but in the right order and with clear purpose. If the tax base keeps rewarding idle land and penalizing productive improvements, relief alone won't fix housing supply or land use inefficiency.

Is a pure land value tax always the right end state

Not necessarily. Some jurisdictions may stop at split-rate taxation because it captures most of the efficiency gain with lower transition risk. Others may prefer a broader property tax with stronger income-based protections. What matters is whether the final design taxes economic rents more effectively and productive activity less heavily.

What should ministers or mayors ask first

Ask three questions. What behavior does the current tax system reward. Who would pay more under reform. Can the administration value land and improvements separately with enough credibility to defend the system in public.

Governments that want to reduce taxes on work and productive investment while improving land use need more than abstract theory. Unitism® supports policymakers with land valuation frameworks, fiscal and distributional modeling, transition design, training, and implementation support grounded in tri-factor economics and land-based public finance.