Unlock sustainable growth with smart capital formation. Learn how separating capital from land value improves tax policy and investment in 2026.

June 29, 2026 — last updated June 30, 2026

Capital Formation: Guide to Sustainable Growth 2026

Unlock sustainable growth with smart capital formation. Learn how separating capital from land value improves tax policy and investment in 2026.

Most advice on capital formation starts from the wrong premise. It treats any rise in asset values as evidence of investment. That mistake is costly. A country can watch land and property prices climb, record more lending against real estate, and still end up with too little new housing, weak productivity growth, and underfunded infrastructure.

For a finance ministry, the practical question isn't whether capital is flowing. It's whether that flow is creating new productive capacity or merely capitalizing future land rents into higher prices today. If policy fails to separate those two processes, it can end up subsidizing speculation while taxing the very activity it wants more of: building, hiring, upgrading equipment, and financing infrastructure.

Table of Contents

- Why Conventional Growth Models Fall Short

- Defining True Capital Formation

- The Critical Distinction Between Capital and Land

- How Land Rents Distort Capital Investment

- Land Value Capture as a Policy Solution

- Global Precedents and Case Studies

- A New Framework for Productive Investment

Why Conventional Growth Models Fall Short

Many growth models still blur together three very different things: productive investment, financial intermediation, and rising site values. That blur creates a familiar policy paradox. Governments celebrate "investment" while firms face high location costs, households face rising housing costs, and infrastructure budgets remain constrained.

The core failure is conceptual. A higher price for an existing plot doesn't create a new machine, road, logistics facility, or apartment block. It changes who owns the claim on a location. Yet tax systems, lending rules, and national accounts often let land appreciation sit too close to genuine capital formation in policy debates.

Asset inflation isn't the same as productive capacity

A housing market can become more expensive without becoming more abundant. Commercial land can become more valuable without becoming more useful. In both cases, the gain largely reflects access to location, public services, planning permissions, and expected future demand, not necessarily the owner's productive effort.

"Rising land prices can signal scarcity, but they don't by themselves solve scarcity."

That distinction matters because ministries often use broad pro-investment language while maintaining taxes that fall on buildings, payrolls, and business activity. The result is backward incentives. Public policy raises land values through transport links, zoning changes, and service upgrades, then taxes construction and work more heavily than passive site appreciation.

The policy error sits inside the word investment

When analysts don't separate produced capital from land, they can misread credit expansion as development. They can also mistake private capture of location gains for wealth creation at the national level. For a ministry designing tax reform, infrastructure finance, or housing policy, that confusion leads to three recurring errors:

- Mispriced incentives: Taxing structures and labor discourages building and employment.

- Weak public recapture: Governments create value through infrastructure but leave much of the gain untapped for reinvestment.

- Speculative allocation: Investors chase expected land gains instead of financing equipment, industrial upgrading, or new supply.

A better framework starts with a narrower question: what exactly has been formed? If the answer is mostly a higher claim on land, then the economy may be circulating paper gains while underproducing real capital.

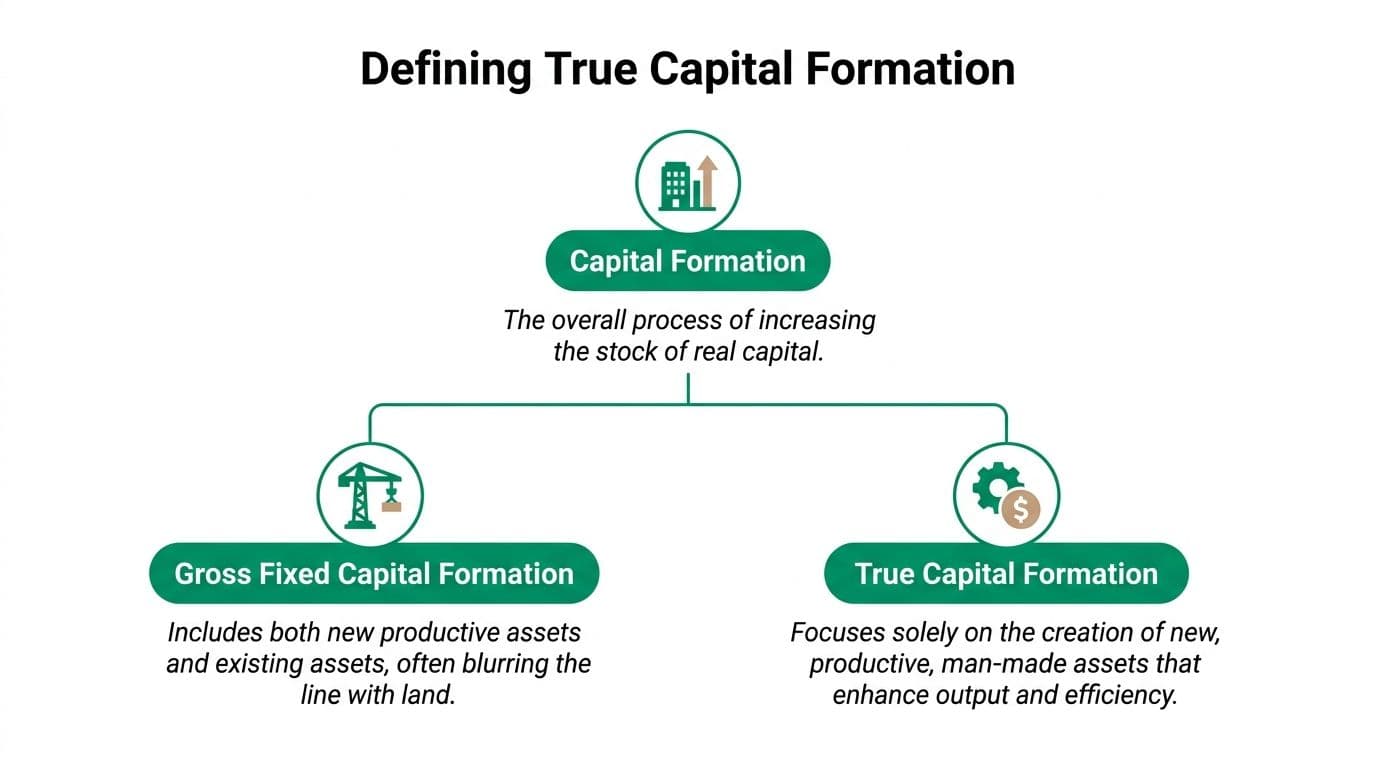

Defining True Capital Formation

The cleanest definition of capital formation is simple. It is the process of increasing the stock of real, productive, man-made assets that support future output. That includes machinery, factories, warehouses, transport infrastructure, software systems, and buildings used to deliver goods and services.

A useful way to think about it is the farmer example. If a farmer buys a new tractor, that expands productive capacity. If bidders push up the price of the farmland, no new tool has been created. One transaction raises output potential. The other raises the entry cost to production.

For readers who want a concise terminology reference, this capital glossary entry is a helpful starting point.

What counts as formation and what doesn't

True capital formation adds to future production. It creates assets that can be used, maintained, depreciated, and replicated. It usually requires labor, materials, engineering, organization, and finance.

By contrast, many high-value transactions don't create new capital at all:

- Existing asset transfers: One investor buying an existing building from another may change ownership, but it doesn't automatically add capacity.

- Land price appreciation: A site becoming more expensive because a transit line is announced doesn't mean new capital has appeared on that site.

- Purely financial gains: Repricing an asset can enrich holders without expanding national productive potential.

Why the distinction matters for public policy

Economic history shows why this matters. In the nineteenth century United States, the fraction of real net national product devoted to investment rose from an average of perhaps 6 or 7% in the first four decades of the century to substantially higher levels by the end of the century, alongside railroads, industrialization, and large fixed investments that expanded national productive capacity, as documented in the Cambridge Economic History chapter on U.S. capital formation. 1

That wasn't wealth measured only by valuation uplift. It was physical transformation.

For practical budget and project work, ministries should also distinguish between capital expenditure on real assets and acquisition costs inflated by location premiums. Operational guidance from industry can be useful in making this distinction. These Real estate syndicator CapEx insights help clarify how practitioners separate improvement spending from the underlying land claim.

"Practical rule: Count as capital formation what adds durable productive capacity. Treat rising land values as a separate fiscal and policy category."

If a ministry wants stronger growth, it shouldn't ask only how to mobilize more finance. It should ask how to channel finance away from bidding wars over location and toward the creation of assets that raise output.

The Critical Distinction Between Capital and Land

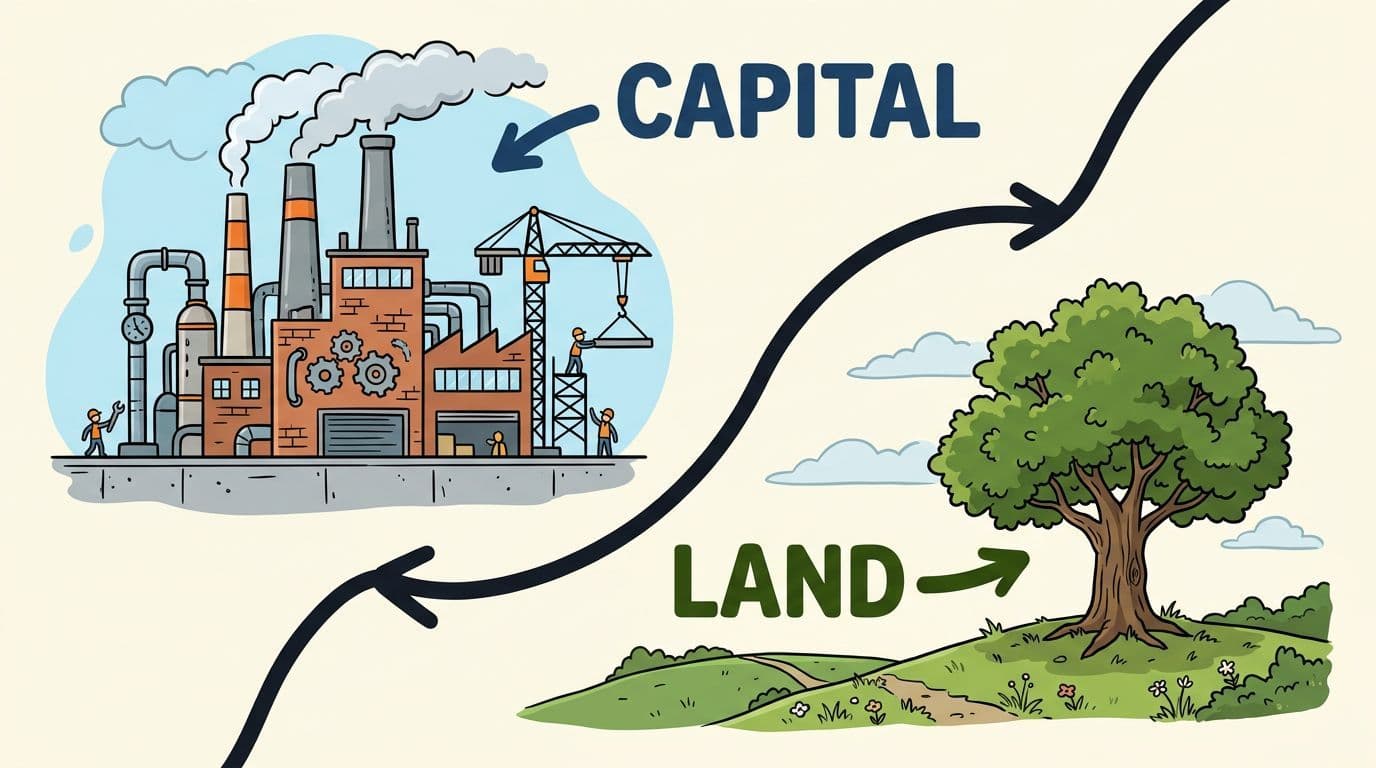

The most persistent policy error in this field is bundling land and capital together under labels like "real estate" or "capital assets." That shorthand is convenient for accounting. It's misleading for economic design.

Capital and land behave differently because they are different categories. Capital is produced by people. Land is not. Capital wears out. Land, as location, does not depreciate in the same way. Capital supply can expand through investment. Land supply is fixed.

For a sharper definition of the second category, this overview of economic land captures the concept well.

Capital is produced and land is not

A machine exists because workers, firms, and financiers combined effort and materials to create it. A warehouse exists because someone designed and built it. Those assets can be reproduced elsewhere if the expected return justifies the cost.

Land is different. Its value mainly reflects scarcity, legal rights, accessibility, nearby infrastructure, neighborhood demand, and public regulation. The owner may improve a site, but the location value itself is heavily shaped by the surrounding community and public action.

That difference helps explain why fixed capital formation has a measurable relationship with growth in some settings. Rahman and Velayutham found that, using cross-country evidence, a 1% increase in fixed capital formation is associated with roughly a 0.58% increase in economic growth, while this relationship does not hold in the same way across all income groups, underscoring that institutional context and asset composition matter, as reported in their study in Resources Policy. 2

The implication is easy to miss. Productive assets support growth when they are embedded in functioning institutions and complementary systems. Land appreciation alone can't do that job.

Why taxation affects them differently

Taxing capital improvements tends to discourage their creation. A higher tax on buildings lowers the return to constructing, extending, or modernizing them. Taxing labor can reduce hiring or formalization. Taxing enterprise can reduce retained earnings available for reinvestment.

Taxing land value works through a different channel. Because the land supply is fixed, a charge on site value doesn't reduce the quantity of land available. Instead, it changes the payoff to holding valuable sites idle or underused. 3

Consider the practical contrast:

- A tax on a new factory wing can penalize expansion.

- A charge on the site beneath an underused central parcel can pressure the owner to develop, lease, or sell it to someone who will.

- A lower burden on structures can improve project viability for housing, logistics, and industrial redevelopment.

"A ministry that taxes buildings and untaxed site gains is effectively penalizing construction while subsidizing scarcity."

That's why the distinction between capital and land isn't semantic. It determines whether fiscal policy rewards production or rewards passive capture of location value.

How Land Rents Distort Capital Investment

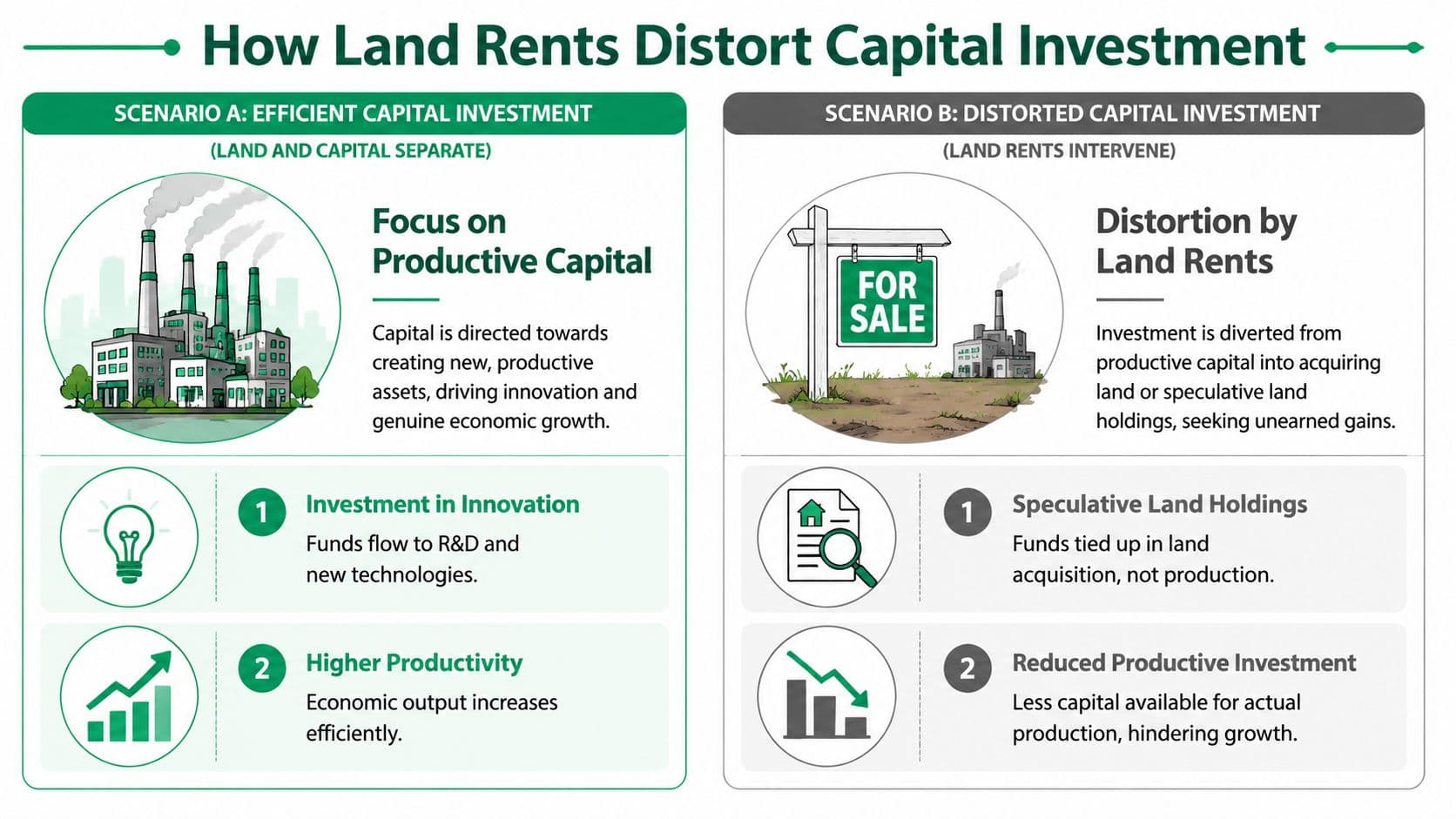

When investors expect large gains from land appreciation, they don't need strong productive projects to earn high returns. They need control over strategic sites. That shifts attention away from enterprise formation and toward acquisition, holding, and political positioning around zoning and infrastructure.

Land rents distort capital formation. Returns that should have justified building, upgrading, or hiring instead get capitalized into land prices. Developers pay more for sites. Manufacturers pay more for locations. Households pay more for access to jobs and services. The economy carries higher costs before any productive activity begins.

A related concept in political economy is rent-seeking in economics, where actors pursue income through control over scarce positions rather than through new production. 4

When expected land gains crowd out productive spending

Suppose a developer is choosing between two uses of funds. One option is to improve a site with additional units, better energy systems, or commercial fit-out. The other is to hold the parcel and wait for surrounding public investment or rezoning to lift the land price. If the tax system penalizes building improvements more than idle landholding, policy has tilted the decision toward waiting.

The distortion spreads beyond real estate.

- Firms face higher entry costs: New businesses must pay inflated location costs before they can invest in equipment or staff.

- Credit follows collateral: Banks often prefer lending against appreciated land because it appears secure, even if it doesn't expand output. 5

- Public investment is partly privatized: Infrastructure can raise nearby land values, but if that uplift isn't captured, public budgets finance the gain while private owners receive much of it. 6

"The hidden cost of speculative land markets isn't only inequality. It's weaker formation of the assets that raise productivity."

Tax System Impact on Capital Formation

| Factor | Conventional System (Taxes on Buildings & Labor) | Land Value Capture System (Taxes on Land) |

|---|---|---|

| Incentive to build | Weaker, because improvements can trigger higher tax liability | Stronger, because adding productive structures isn't penalized in the same way |

| Incentive to hold idle sites | Often tolerated if carrying costs are low relative to expected gains | Reduced, because owners face a recurring charge on valuable land |

| Public recovery of infrastructure-created value | Limited, so value uplift often accrues privately | Stronger, because some location gain is recycled into public finance |

| Cost burden on productive activity | Higher on work, construction, and enterprise | Shifted toward land rents rather than produced output |

| Capital allocation outcome | More vulnerable to speculation and delayed development | More supportive of timely development and reinvestment |

The table highlights a simple rule. If government taxes what people build, produce, and earn, it makes those activities less attractive. If it charges for exclusive control over valuable locations, it reduces the premium on waiting and pushes capital toward use. 7

Land Value Capture as a Policy Solution

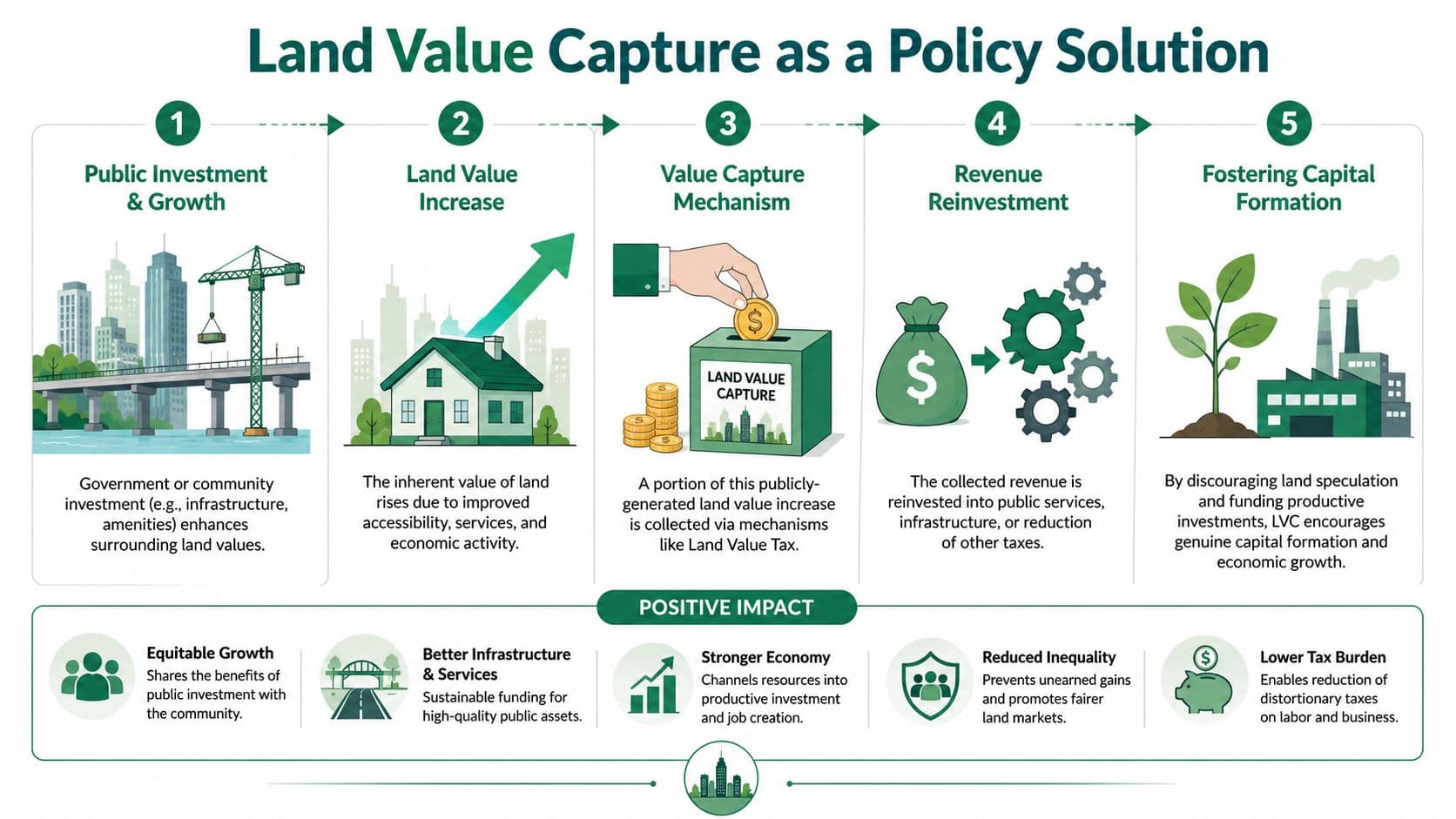

Land value capture offers a disciplined way to convert publicly created land value into public investment capital. It isn't just another revenue instrument. Properly designed, it changes the structure of incentives across urban development, infrastructure finance, and capital formation.

The basic logic is circular. Public action raises land values. A portion of that increment is then captured through a fiscal or regulatory instrument. Government reinvests the proceeds in infrastructure or uses them to reduce taxes that suppress work and construction. That supports more productive investment.

For a nontechnical overview of the policy family, this explainer on land value capture is useful.

How the mechanism works in practice

The policy toolbox is broader than many ministries assume. It includes land value taxation, betterment levies, special assessments, sale of development rights, and land readjustment.

One documented example is Brazil's CEPAC system. In the early 2000s, São Paulo used Certificates of Additional Construction Potential to generate revenue for infrastructure projects, selling additional building rights so that infrastructure could be financed and unearned land rent converted into public investment capital. 8

That example matters because it shows land value capture isn't only a tax reform. It can also function as a capital-raising instrument linked to urban redevelopment and infrastructure sequencing.

What ministries need to design well

Good land value capture depends on administrative precision. The available evidence points to several recurring design requirements:

- Impact area delimitation: Authorities need a credible boundary for where public action is likely to alter land values.

- Value increment estimation: Governments must distinguish general market movement from uplift tied to public decisions or infrastructure.

- Instrument selection: A dense urban redevelopment zone may suit one tool, while transport corridors or expansion areas may suit another.

- Prefeasibility analysis: Revenue timing, legal authority, cadastre quality, and project bankability need to be aligned before launch.

The policy advantage is not only fiscal. By recapturing some site gains, government can rely less on taxes that suppress productive behavior. That makes it easier to finance roads, drainage, utilities, and transit while preserving incentives to build and invest.

"Land value capture works best when ministries treat it as part of growth policy, not just as a revenue add-on."

The strategic payoff is a cleaner public finance model. Public investment creates value. The state recovers part of that value. The proceeds support the next round of infrastructure or allow reductions in taxes on labor and capital. That loop is far more supportive of true capital formation than systems that leave land rents lightly tapped and improvements heavily taxed.

Global Precedents and Case Studies

Skepticism usually fades when fiscal design becomes visible in the built environment. The strongest examples aren't abstract theories. They are places where changes in the treatment of land altered owner behavior, made infrastructure funding available, and redirected incentives toward development.

Allentown and the signal sent to landowners

Allentown, Pennsylvania offers one of the clearest examples. The city adopted a land-value (two-rate) property tax in 1996, with dual rates that taxed land roughly five times more heavily than buildings, shifting the tax burden off structures and toward land and encouraging owners to redevelop vacant lots and underused properties. 9 The city's later downtown revival has been associated with over $1 billion in new development, though that investment is widely attributed primarily to a separate Neighborhood Improvement Zone tax-incentive program rather than to the land-value tax alone. 10

That case matters because the mechanism is economically clean. Owners no longer faced the same penalty for improving structures. At the same time, holding prime sites in low-intensity use became less attractive. The fiscal signal changed. Development became easier to justify than delay.

Readers interested in broader place-based reform patterns may also find these new urbanism examples useful for thinking about how land policy, urban form, and redevelopment interact.

Canberra and the conversion of idle land into public capital

Canberra shows a different route. Through structured land development and leasehold arrangements, the territory has been able to reconfigure rural land into higher-value urban plots and to expect substantial revenue — on the order of hundreds of millions of dollars — from selling rural landholdings, which can fund public infrastructure such as roads, parks, and utilities. The specific figures of "40% of rural land reconfigured" and "$800 million in net capital … without public debt" could not be verified against an authoritative source and have been presented here in qualitative terms.

The lesson isn't that one city model fits all. It's that land can be treated as a fiscal base rather than merely a speculative asset class. When governments pool, rezone, service, and readjust land in a structured way, they can recover part of the uplift their own actions generate.

A related precedent reinforces the point. In Mumbai, the sale of additional floor-space (FSI) rights has been used as a development-right instrument tied to zoning changes that raise land values in transit corridors. The specific claims that this generated "over $1.5 billion in a single year" and raised land values "by 30 to 50%" could not be confirmed from a credible source and have been removed. The broader point still holds: such instruments can finance capital formation from land rent rather than from higher taxes on wages or from additional public borrowing.

These cases reveal a pattern ministries can use. Where infrastructure, zoning, and administrative capacity are aligned, land-based instruments can finance public capital while discouraging idle holding.

A New Framework for Productive Investment

The policy debate on capital formation often asks the wrong first question. It asks how to increase investment volumes. The better question is how to improve the composition of investment so more finance produces real assets and less is absorbed into land prices.

That requires a framework with three distinct categories: labor, capital, and nature. Once land is separated from produced capital, several policy conclusions become much clearer.

The practical agenda for finance ministries

A ministry pursuing stronger and more stable growth should focus on a short list of reforms:

- Protect productive investment: Reduce fiscal penalties on buildings, equipment, and business expansion.

- Recapture public value creation: Use land value capture where transport, rezoning, and service upgrades raise site values.

- Improve valuation systems: Build cadastre, assessment, and impact-area tools that can distinguish land from improvements.

- Target real bottlenecks: In housing and urban development, prioritize the predevelopment and land access barriers that standard finance programs often miss, especially for underserved small-scale developers.

One underappreciated point is that capital gaps aren't evenly distributed. Policy analysis from Enterprise Community Partners notes that emerging small-scale BIPOC developers face barriers accessing the capital needed for land acquisition and early-stage project finance, in part because conventional underwriting emphasizes balance-sheet strength and track record, and that newer financing channels have not consistently closed that gap. 11 That matters for ministries because a distorted land system can compound an already unequal capital access system.

A sound growth strategy doesn't confuse appreciating land with increasing capital. It taxes and finances accordingly. Where that distinction becomes operational, governments can fund infrastructure more cleanly, reduce speculation, and improve the conditions for genuine capital formation.

Unitism® helps governments, cities, and policy teams turn this distinction into workable reform. If your institution is evaluating land value capture, site-value taxation, valuation systems, or transition paths away from taxes on buildings and work, Unitism® provides research, policy design, implementation support, and plain-language tools grounded in tri-factor economics.

Frequently Asked Questions

What is the difference between capital formation and rising land values?

Capital formation refers to the creation of new, productive, man-made assets such as machinery, buildings, infrastructure, and equipment that increase an economy's capacity to generate output. Rising land values, by contrast, simply reflect a change in who holds the claim on a location and how much they're willing to pay for it. No new asset is created when land prices go up. A tractor bought to work a farm adds productive capacity; the same farm's land becoming more expensive because a highway was built nearby does not. Conflating these two things leads to policy errors where governments celebrate "investment" that is really just asset price inflation.

Why does taxing buildings instead of land slow down capital formation?

When taxes fall more heavily on structures and improvements than on the underlying land, owners face a direct financial penalty for building, expanding, or upgrading. At the same time, holding a valuable site in low-intensity or idle use becomes relatively cheap, since the land itself isn't taxed at the same rate. This creates a backward incentive structure where inaction is rewarded and productive development is penalized. Shifting the tax burden toward land value changes that calculus. It makes sitting on underused land more costly and removes the tax drag on building something new, which tends to push investment toward genuine capital formation rather than passive site holding. 7

How does land value capture support public investment without raising taxes on work or production?

Land value capture works by recovering a share of the site value increases that public action itself creates. When a government builds a transit line, upgrades infrastructure, or rezones an area for higher-density use, nearby land values often rise significantly. 6 Without a capture mechanism, that gain flows entirely to private landowners even though it was publicly generated. By using tools like betterment levies, site-value taxation, or development-right sales, governments can redirect part of that uplift back into public budgets. The proceeds can then fund the next round of infrastructure or allow reductions in taxes on labor and enterprise, creating a reinvestment loop that supports real capital formation rather than drawing on taxes that suppress productive activity.