Learn how does tax increment financing work in 2026. Explore TIF district creation, bond repayment, mechanics, risks, and land value capture for city planners.

July 16, 2026

How Does Tax Increment Financing Work

Learn how does tax increment financing work in 2026. Explore TIF district creation, bond repayment, mechanics, risks, and land value capture for city planners.

You're probably looking at a corridor that hasn't kept up. The sidewalks are broken, the utility capacity is weak, storefronts sit half-empty, and every redevelopment proposal dies when the infrastructure bill hits the spreadsheet. Across town, another district is thriving and generating the tax base that keeps schools, parks, and public safety running.

That contrast is where Tax Increment Financing usually enters the conversation. It offers a tempting promise: fix the lagging district without raising current tax rates, because the project will pay for itself through future growth in property value. For a city manager or planner under pressure to make stalled land productive, that sounds practical.

It can be practical. It can also become a long, opaque diversion of revenue tied to forecasts that may not materialize, especially in weak markets. If you're weighing how does Tax Increment Financing work, the core question isn't just mechanics. It's whether TIF is the right tool at all, or whether a city should move toward direct land value capture instead, especially approaches based on land-use rights rather than land-value taxes. That distinction matters if you're also wrestling with affordability pressures and land-driven cost escalation, which are closely tied to why housing is unaffordable.

Table of Contents

- Introduction A Tale of Two Districts

- The Core Mechanics of Tax Increment Financing

- The Legal and Fiscal Setup of a TIF District

- Common TIF Use Cases and Critical Risks

- TIF Compared to True Land Value Capture Instruments

- Implementation Best Practices for Public Officials

- Conclusion A Policy Recommendation for Smarter Growth

Introduction A Tale of Two Districts

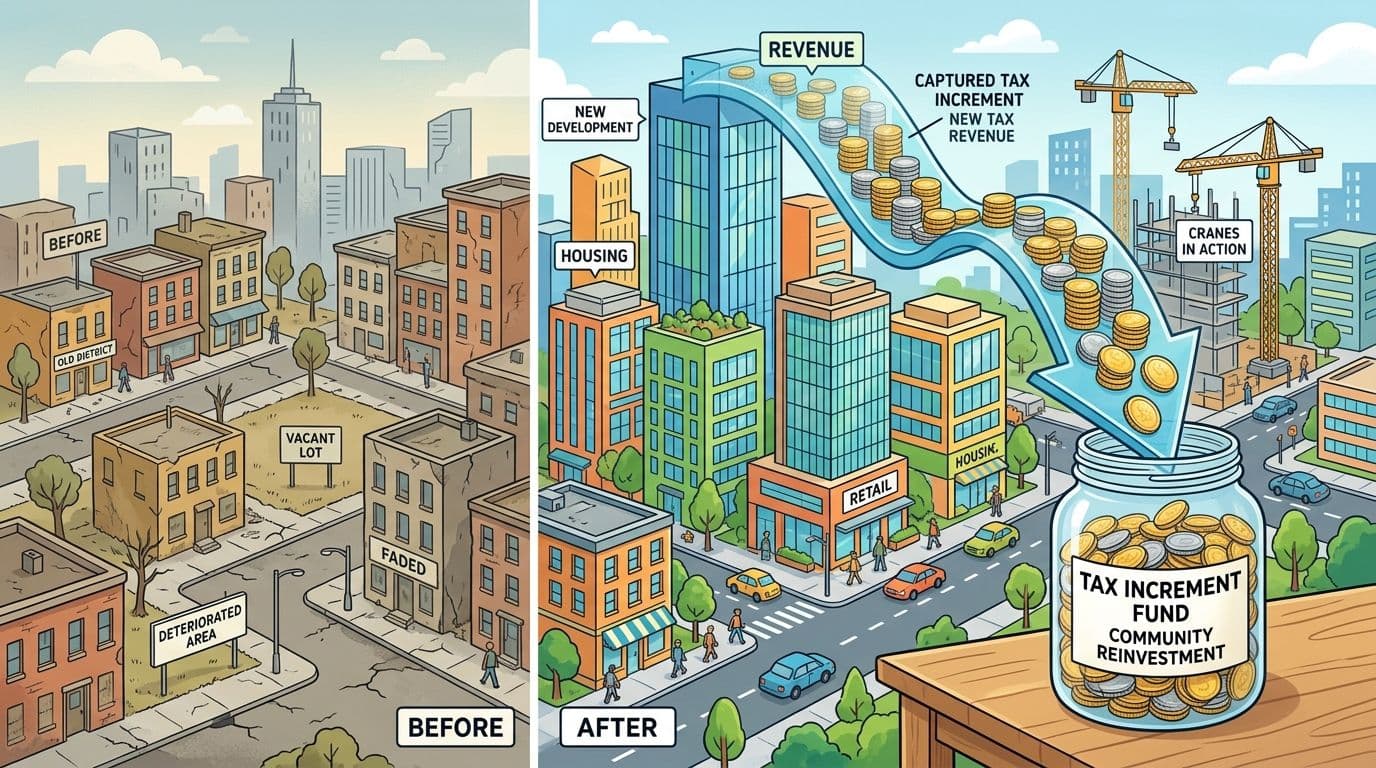

A planner stands between two districts. One has active storefronts, steady maintenance, and a tax base that supports routine city services. The other has vacant parcels, obsolete buildings, and infrastructure gaps that repel private capital. Local officials don't need an academic definition to recognize the problem. They live with it every budget season.

That's the setting where TIF gets pitched as a redevelopment tool. Draw a boundary. Freeze the current assessed value. Fund public improvements. Capture the future increase in tax revenue inside that boundary and use it to pay development costs. Done well, that can help make viable sites that the private market has ignored.

Done poorly, it becomes a subsidy wrapped in technical language. The city ties up future revenue for years, assumes property appreciation that might not happen, and shifts fiscal strain onto everyone outside the district. In practice, TIF isn't magic. It's a bet on land values, timing, and public administration.

Practical rule: If the district's market fundamentals are weak and the public case is vague, TIF won't fix a bad project. It will only finance the attempt.

For city managers and planners, the important distinction is this: TIF is not a general growth strategy. It's a narrow financing mechanism for specific places and specific costs. If your broader goal is equitable development, lower speculation, and more stable public revenue, stronger tools exist. The rest of the analysis starts with the mechanics, then moves to the harder question of whether cities should prefer direct value capture through land-use rights.

The Core Mechanics of Tax Increment Financing

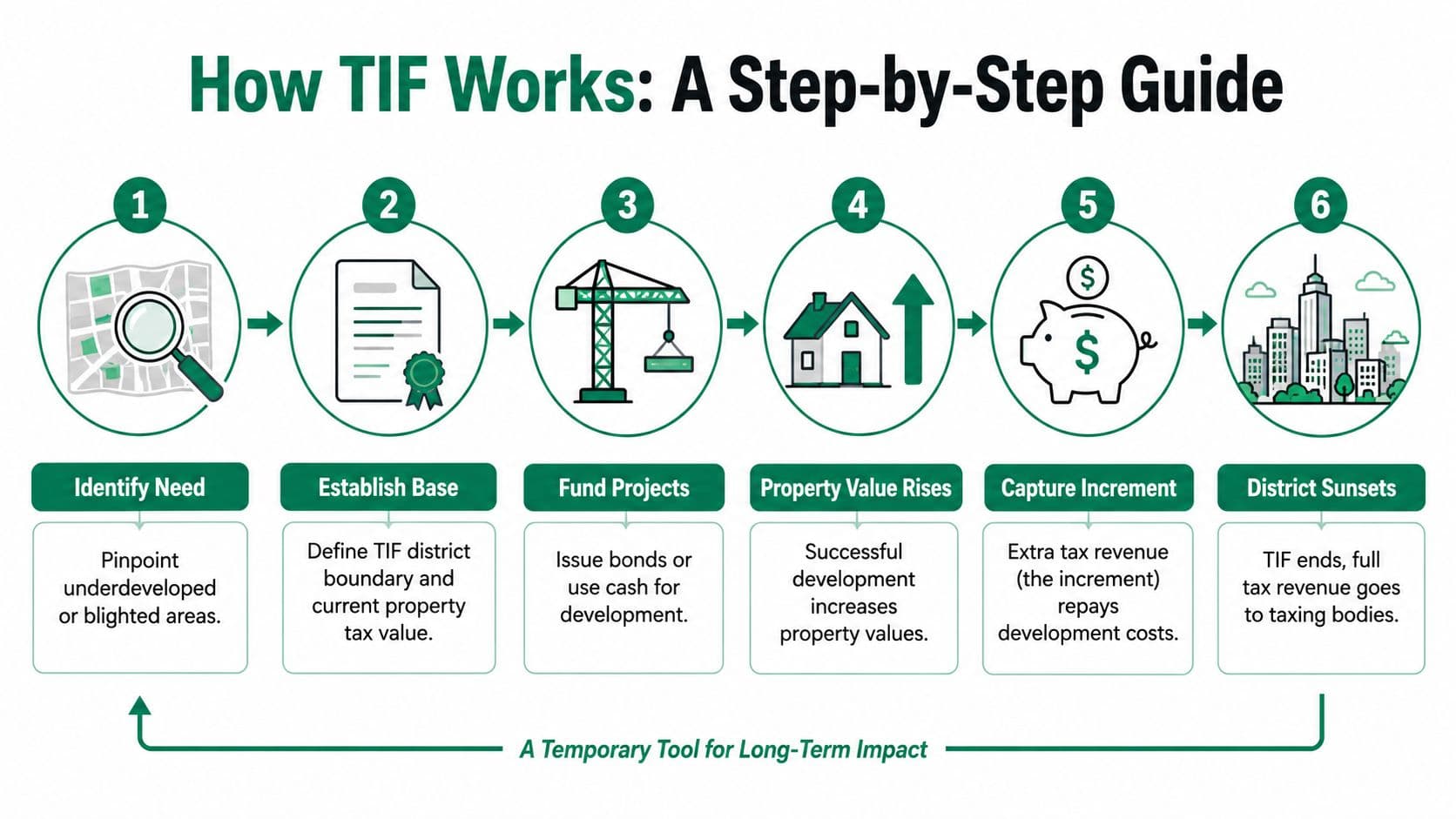

TIF pre-commits future property tax growth to pay current redevelopment costs. In practice, that means the city draws a district, fixes a base assessed value, and diverts taxes generated by later increases in value into a dedicated fund for eligible project costs, as described in this TIF overview.

Step one creates the district

The starting point is not the bond. It is the tax base.

A city designates a TIF area and records the taxable value inside that boundary on the date of creation. That amount becomes the base value. Taxes generated from that base continue to flow to the usual taxing jurisdictions under the rules set by state law and local agreements.

The policy question starts here. If officials draw the boundary too broadly, they may end up capturing growth that would have happened anyway. If they draw it too narrowly, the district may not produce enough increment to support the improvements it is supposed to finance.

Step two separates ordinary revenue from captured growth

Once the district is active, assessors continue valuing property as they normally would. If new construction occurs, obsolete buildings are replaced, or market conditions improve, the taxable value can rise above the base.

That increase produces the increment. The taxes tied to the increment are set aside for TIF purposes rather than treated as unrestricted revenue. For budgeting, this distinction matters more than the diagram suggests. A captured increment can support a project, but it also reduces what would otherwise be available for general services or overlapping jurisdictions after the base amount is accounted for.

Before approving a district, cities should run a fiscal impact analysis for redevelopment areas to test whether the projected increment justifies the revenue diversion.

Step three converts projected increment into cash

Redevelopment costs arrive early. Increment arrives later. TIF works by turning that expected future revenue stream into present financing.

Cities usually use one of three structures:

- Bond financing. The city issues debt and repays it from future increment.

- Pay-as-you-go reimbursement. The developer pays eligible costs upfront and is reimbursed only as increment is collected.

- Tax rebate structure. The developer pays the taxes, and the incremental portion is returned under the approved agreement.

These structures are not interchangeable. Bond financing delivers immediate capital but creates the greatest exposure if assessed values stall, appeals reduce valuations, or construction slips. Pay-as-you-go is slower, but from a municipal risk standpoint it is often the cleaner option because reimbursement depends on real collections, not optimistic underwriting.

A working example

Suppose property inside the district has a base assessed value that generates annual taxes of $2,000. After infrastructure work and private investment, the same property generates $10,000 in annual taxes. The original $2,000 remains tied to the base. The additional $8,000 is the increment available for TIF purposes.

That arithmetic is simple. Administration is not.

Officials still have to ask whether the increase came from the public improvement, from a hot market, or from a project that would have proceeded without subsidy. That is the central weakness in many TIF programs. They measure captured growth well enough, but they often prove causation poorly.

If you need a quick refresher on how tax rates are assembled before projecting district revenue, Texas property tax rate explained is a useful primer.

TIF performs best when a public investment clearly raises nearby land values and the city can document that the project would not proceed in the same form without assistance.

That is also why many cities should treat TIF as a limited tool, not a default development strategy. It captures value only after assessments rise, inside a narrow geography, and usually for a single project or corridor. Stronger land value capture systems, especially those tied to land-use rights and entitlement decisions, can recover public value more directly, with less fiscal ambiguity and better citywide equity.

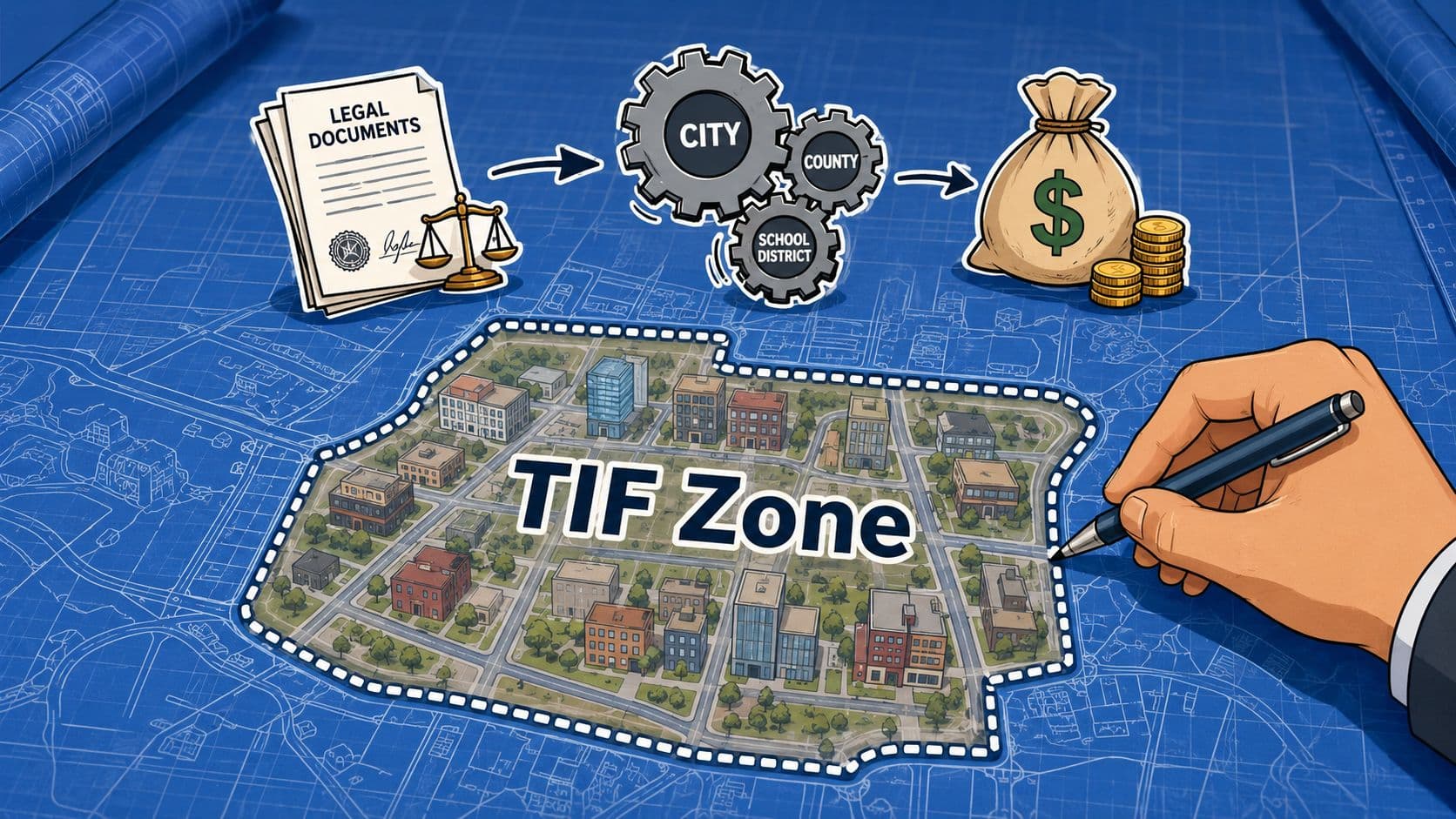

The Legal and Fiscal Setup of a TIF District

TIF districts are creatures of state law. Local governments don't invent them from scratch. They operate within enabling statutes that define eligible costs, approval steps, district duration, reporting requirements, and the rules for ending the district.

The legal frame matters more than most sponsors admit

One of the most misunderstood points is that the increment usually isn't treated as a tax cut. Legally, the captured increment is a reallocation of revenue via Payments-In-Lieu-Of-Taxes, or PILOTs, where developers pay the full assessed tax rate and the incremental portion is diverted to the TIF fund. In California, mandates have required 20% of that diversion to be allocated to affordable housing, as described in Minnesota's TIF guidance on PILOT treatment.

PILOT structures matter because they determine cash flow and accountability. On paper, everyone is paying the full rate. In practice, the city is rerouting part of that payment to a restricted financing purpose.

Cities also need to think carefully about duration. State statutes commonly allow TIF capture for a long period, and that long tail changes the fiscal posture of the jurisdiction. A district that lasts decades can outlive the administration that created it, which is why a rigorous fiscal impact analysis should be standard before approval.

Base value discipline determines who bears the cost

The baseline assessment is one of the most consequential choices in the entire structure. If the base is set too low, the district captures more future growth than necessary and general services lose access to revenue they otherwise would have seen. If the base is set too high, the project may never generate enough increment to cover the intended costs.

That's not a technical footnote. It's the fulcrum of the deal.

Consider how many judgments sit inside the initial designation:

- Boundary choice determines which parcels contribute future increment.

- Blight findings shape the legal justification for capture.

- Eligible cost definitions determine whether spending stays focused on public improvements or drifts into broader subsidy.

- Decertification terms determine how quickly the district ends once obligations are met.

A TIF district is only as honest as its baseline assumptions.

Good administration means forcing those assumptions into the open. Weak administration hides them behind consultant models and optimistic redevelopment narratives.

Common TIF Use Cases and Critical Risks

TIF has a legitimate place in the public finance toolbox. It was designed for places where normal market activity isn't enough to carry the cost of redevelopment, especially where site conditions or infrastructure deficits suppress investment.

Where TIF can make sense

The standard uses are familiar to most planners:

- Infrastructure gaps such as sewer extensions, streets, utilities, or structured parking that private developers won't finance alone.

- Environmental remediation on contaminated or obsolete industrial sites where cleanup costs block reuse.

- Public realm improvements including streetscapes, sidewalks, and park improvements meant to trigger broader private investment.

- Land assembly and demolition where fragmented ownership or derelict structures prevent redevelopment.

In those settings, TIF can help align timing. The city funds enabling improvements first. If those improvements support productive land use, the increment then repays the cost.

A well-targeted district can also keep attention on a defined geography instead of scattering subsidies across disconnected projects. That focus is one reason TIF remains politically attractive.

Where cities get into trouble

The central risk is the but-for test. If the project would have happened anyway, then TIF doesn't catalyze development. It only diverts revenue that could have supported schools, police, fire, or general operations.

The second problem is underperformance. A 2023 study noted that TIF districts often rely on optimistic projections, with 30-40% of districts in some midwestern U.S. cities failing to generate sufficient increments to cover debt within the original timeline, according to Good Jobs First's discussion of TIF risk. That's the number public officials should keep in mind when a revenue forecast arrives with too much confidence.

Here are the risks that matter most in practice:

- Forecast risk. Assessed values don't always rise on schedule. Recession, weak absorption, or poor project execution can delay increment.

- Budget displacement. Even if the base remains untouched, future tax growth that might have supported general services stays locked inside the district.

- Equity concerns. TIF can improve one area while leaving lower-income neighborhoods outside the district with fewer public resources.

- Complexity and opacity. Multiple reimbursement agreements, overlapping public purposes, and long district lives can make oversight difficult.

- Political drift. A blight tool can become a routine incentive for projects in already-improving areas.

A city should also distinguish between public improvements that create broad value and private gap-filling requests that mainly protect a developer's pro forma. Those are not the same thing.

For officials trying to connect redevelopment finance to long-term capital planning, this broader discussion of infrastructure funding is useful because it highlights options that don't depend so heavily on speculative future appreciation.

TIF Compared to True Land Value Capture Instruments

If you work in public finance long enough, you start seeing TIF for what it is. It's a workaround. It captures land value indirectly, after development, over time, through a ring-fenced stream of property tax growth. That's better than giving subsidies away with no recapture at all, but it's still a second-best instrument.

Why TIF is only an indirect form of land value capture

TIF captures value only if assessed values rise enough, soon enough, and in the right parcels. The city fronts risk first and collects later. It also relies on district boundaries, reassessments, bond structures, and long compliance periods.

Its intended payoff is delayed. Once TIF obligations are completed over a defined period, often 20 to 30 years, the full increased property value returns to the general tax rolls, permanently expanding the tax base, as explained by Roselle's TIF overview. That's the classic defense of TIF. Temporary diversion now, broader tax base later.

That logic can hold. But cities still absorb years of uncertainty before they reach that outcome.

Why land-use rights are better than land-value taxes

A city that wants cleaner, more efficient value capture should prefer land-use rights over both TIF and annual land-value taxes.

Land-use rights are the public authority to permit a more valuable use of land. That might mean added density, a change in permitted use, additional floor area, or development capacity that wasn't previously available. Instead of waiting for future assessments and then siphoning off increment over many years, the city can auction, lease, or charge transparently for those rights upfront.

That approach has several advantages:

- Revenue arrives earlier. The city captures part of the expected land uplift when the right is granted, not after years of uncertain appreciation.

- The transaction is transparent. Officials can tie the granted right directly to a payment, lease, or public obligation.

- Speculation is reduced. Owners can't sit on entitlement gains without paying for them.

- Administrative burden is lower than maintaining a complex TIF district with annual monitoring and restricted revenue accounting.

- The public bargain is clearer. The city grants a valuable permission. The public receives compensation.

Site-value taxation is still stronger than TIF because it focuses on land rather than improvements and discourages idle holding. But land-use rights go one step further for many growth decisions. They let the city capture expected future value at the moment public permission creates it.

If you want a broader grounding in the policy family behind these tools, this guide on land value capture explained is a helpful reference.

Comparison of Land Value Capture Mechanisms

| Mechanism | Value Capture Method | Fiscal Risk to City | Administrative Complexity | Impact on Speculation |

|---|---|---|---|---|

| TIF | Captures future property tax growth within a district after value rises | Higher, because revenue depends on projected increment materializing | High, due to district setup, compliance, accounting, and financing structures | Limited, because owners may still hold land while expecting subsidized uplift |

| Site-value taxation | Charges recurring tax based on land value rather than buildings | Lower than TIF, because revenue doesn't depend on a single project succeeding | Moderate, because it requires regular land valuation and tax administration | Stronger, because holding underused land becomes more costly |

| Land-use rights | Captures value upfront through auction, lease, or charge for added development rights | Lower, because payment is secured when rights are granted | Moderate to lower, depending on the permitting and disposition system | Strong, because entitlement gains are priced directly and transparently |

Cities shouldn't have to gamble on future increments when they can charge for publicly granted land advantages at the moment those advantages are created.

That's why my policy preference is clear. If a city has the institutional capacity to shift toward direct value capture, it should build around land-use rights first, use site-based charges where appropriate, and reserve TIF for rare cases where neither option can handle a genuine redevelopment barrier.

Implementation Best Practices for Public Officials

Sometimes TIF is the only politically available tool on the table. When that happens, the job isn't to celebrate it. The job is to constrain it.

Five rules that improve bad TIF practice

A disciplined TIF program starts with a short list of hard rules:

- Use an independent but-for analysis. If the project is viable without subsidy, reject the district or reduce the subsidy scope.

- Model conservatively. Underwrite slower value growth and delayed absorption, not best-case redevelopment narratives.

- Limit eligible costs. Prioritize durable public improvements such as utilities, streets, remediation, and land assembly over soft or loosely defined expenditures.

- Write clawbacks and performance triggers. Reimbursement should depend on actual delivery, not promised outcomes.

- Create a visible public dashboard. Show district revenues, expenditures, obligations, and sunset conditions in plain language.

Those aren't cosmetic reforms. They separate a narrowly justified TIF from a standing invitation for negotiated subsidy.

A city should also use shorter decision loops. Don't approve a district and then disappear into annual reports nobody reads. Assign ownership to finance staff, planning staff, and legal staff jointly, and require periodic review of whether the district still serves a public purpose.

When to walk away

Officials should decline TIF when the case depends on one or more of the following:

- The market is already moving and the district mainly captures growth that private demand would have produced anyway.

- The public improvements are vague and mostly exist to support a single developer's financing gap.

- The debt coverage story is fragile even under ordinary downside scenarios.

- The city has better options, especially direct land value capture or reform of the local property tax structure.

For jurisdictions considering broader reform, this discussion of property tax reform helps frame TIF as one small piece of a larger fiscal design problem rather than a standalone answer.

The practical test is simple. If you wouldn't be comfortable explaining the district's assumptions, risks, and trade-offs in a public meeting without slides from a consultant, don't approve it.

Conclusion A Policy Recommendation for Smarter Growth

A city manager under pressure to revive a corridor can make TIF sound like the responsible middle path. Approve the district, finance the improvements, and let future growth cover the cost. In a narrow set of cases, that can work.

The policy problem is that TIF asks a city to bet on value growth that may or may not arrive, while committing future revenue that could have supported general services or broader infrastructure priorities. It also captures value late, after the project structure, subsidy terms, and political commitments are already in place. For many cities, that is an expensive way to do public finance.

My recommendation is straightforward. Use TIF sparingly, with tight eligibility rules and a clear public purpose. Do not treat it as the standard redevelopment tool.

Cities that want a stronger long-term model should shift toward land value capture methods that collect public value more directly. Site-value taxation is often cleaner because it taxes land rather than improvements and reduces the incentive to hold well-located parcels in low-value use. In many growth areas, land-use rights are better still. If public action grants additional height, density, floor area, or a more profitable use, the city should charge for that benefit through a transparent fee, negotiated contribution, lease, or auction.

That captures value earlier. It is easier to explain in public. It avoids tying repayment to optimistic appreciation forecasts over long periods.

The broader point is fiscal design, not just project finance. Cities get better results when they claim a fair share of publicly created land value at the moment it is created and allocate that revenue openly to infrastructure, housing, and services. That approach is usually more equitable, more efficient, and easier to govern than project-by-project reliance on TIF.

If your team is rethinking TIF, land-value capture, or the fiscal rules behind urban growth, Unitism® offers research, policy design, valuation methods, and implementation support for governments that want to fund public services by sharing the rental value of land and nature while reducing taxes on work and productive investment.