Explore modern infrastructure funding models. Learn how land-use rights and land-value capture offer a stable, equitable alternative to traditional financing.

July 10, 2026

Infrastructure Funding: A Guide to Land-Based Finance

Explore modern infrastructure funding models. Learn how land-use rights and land-value capture offer a stable, equitable alternative to traditional financing.

The global infrastructure funding gap is $1 trillion annually, and the most useful response isn't to ask only where more money will come from. It's to ask which revenue base can fund long-lived assets without punishing work, building, and enterprise. The usual debate stays trapped between taxes, debt, and private capital. That misses a more durable fiscal question: when public action raises land values, should governments keep taxing labor and investment, or should they recover more of the land-based value they help create?

That question matters because the capital is there, but the funding architecture is often weak. The combination of public-private coordination, better project delivery, and land-based revenue offers a more coherent route than endlessly layering grants, bonds, and distortionary taxes. For ministries assessing long-term infrastructure funding, a useful companion on federal program mechanics is WaterJobsIntel's guide to funding, especially when paired with a broader fiscal lens on long-term public finance resilience.

Table of Contents

- The Trillion-Dollar Question in Infrastructure Funding

- A Catalogue of Traditional Funding Instruments

- The Land Value Advantage for Public Revenue

- Why Land-Use Rights Outperform Land-Value Taxes

- Global Precedents and Implementation Pathways

- A Design Checklist for Future-Proof Funding

The Trillion-Dollar Question in Infrastructure Funding

The headline figure is large enough to distort policy judgment. The world faces a $1 trillion annual infrastructure funding gap, and the same analysis argues that integrating public and private capital is necessary while better project delivery could reduce infrastructure costs by 40%, yielding $1 trillion in average annual savings over the next 18 years according to the CIRSD analysis on infrastructure funding. That changes the frame. The issue isn't solely scarcity of capital. It's weak revenue design, fragmented procurement, and poor alignment between who creates value and who captures it.

For finance ministries, that distinction is decisive. If governments fund infrastructure mainly through taxes on wages, transactions, and buildings, they narrow the productive tax base they need for growth. If they rely too heavily on debt, they push today's revenue weakness into tomorrow's balance sheet. If they seek private capital without stable public revenue backing, they raise financing complexity without resolving fiscal fragility.

Practical rule: Treat infrastructure funding as a revenue-system problem first, a capital-raising problem second.

A stronger framework starts with tri-factor economics. Land, labor, and capital aren't the same thing. Labor produces. Capital improves productivity. Land is a natural and locational asset whose value often rises because of public investment, legal order, transport access, utilities, and surrounding economic activity. When governments build transit, water systems, ports, or energy links, nearby site values often increase even where the owner has done little.

That's why land-based revenue deserves a central place in infrastructure strategy. It can recycle publicly created value back into the public budget. It can also reduce dependence on taxes that deter hiring, construction, and formal investment. The key policy choice, however, isn't merely whether to capture land value. It's how. That is where land-use rights deserve more attention than conventional land-value taxes.

A Catalogue of Traditional Funding Instruments

Every ministry already has a toolbox for infrastructure funding. The problem is that each instrument solves one constraint while creating another. A durable strategy starts by being honest about those trade-offs.

In 2024, global Private Participation in Infrastructure investment reached $100.7 billion, a 16% increase from 2023, driven by energy and transport projects in emerging markets where land-value capture mechanisms are increasingly being piloted, according to the World Bank PPI database. That rise shows two things at once. Private capital remains interested in infrastructure. But investors still need projects with credible revenue structures.

Comparison of Infrastructure Funding Instruments

| Instrument | How It Works | Primary Advantage | Key Risks & Distortions |

|---|---|---|---|

| General taxes | Governments fund infrastructure from broad revenue such as income, payroll, sales, or property-related taxes | Large base and familiar administration | Taxes on labor, trade, and construction can suppress productive activity and weaken growth |

| Municipal bonds | Public entities borrow upfront and repay over time from budget revenue or dedicated streams | Matches long-lived assets with long-term finance | Debt depends on future repayment capacity and can crowd out other public spending |

| User charges | Tolls, fares, connection fees, and usage charges recover costs from beneficiaries | Creates a direct payment link and can improve demand management | Political resistance is common, and some essential services can't rely on fees alone |

| Public-private partnerships | Private firms finance, build, operate, or maintain assets under contract | Brings delivery capacity, discipline, and risk-sharing potential | Poor contracts can shift risk back to government and obscure long-term fiscal obligations |

| Land-based charges | Governments recover part of the site value or usage value created by public action | Aligns revenue with place-based value creation | Weak design can trigger valuation disputes or unstable expectations |

General taxation

General taxation is the default because it is administratively established, politically familiar, and broad enough to support national investment plans. It also lets governments fund infrastructure with strong public-good characteristics, including networks that can't recover costs fully from users.

Its weakness is economic. When ministries fund roads, transit, water, and urban services through taxes on wages, business turnover, or improvements to property, they tax activities they want more of. A tax on labor reduces the return to employment. A tax on buildings can penalize maintenance, redevelopment, and infill. A tax on transactions can freeze mobility in land and housing markets.

Municipal bonds and public borrowing

Borrowing remains essential because infrastructure produces service flows over long periods. A bond can align payment with asset life better than annual taxation can. This is often good fiscal practice.

But debt isn't revenue. It is an advance against future revenue. If the underlying revenue base is narrow, cyclical, or politically fragile, borrowing only delays the adjustment. Ministries should ask a simple question before approving debt-financed projects: what recurring value stream will repay the liability without undermining growth?

Borrow for assets. Don't confuse borrowing with a substitute for revenue reform.

User charges and pricing

User fees are often underused in infrastructure debates. Reason Foundation notes that pricing and user fees for major transportation projects remain an overlooked lever, while the Bipartisan Infrastructure Law allocates $850 billion toward core priorities, with over $500 billion for transportation and water, as discussed in its commentary on economic factors in infrastructure debates. That matters because pricing can improve both fiscal discipline and asset utilization.

Still, ministries shouldn't force every asset into a narrow user-pay model. Many systems generate wide spillovers beyond direct users. Transit raises corridor land values. Water and sewer systems support public health and economic development beyond household bills. Ports and logistics assets affect regional productivity. User charges are strongest when paired with another value-recovery tool.

Public-private partnerships and private participation

PPPs can work well when the public side defines outputs clearly, allocates risk carefully, and protects the public balance sheet from hidden contingencies. They can fail badly when governments use them to bypass budget discipline.

A sensible ministry view is operational, not ideological:

- Use PPPs when contracts are measurable. Availability, maintenance, and service standards need enforceable metrics.

- Avoid revenue fantasy. If demand risk is speculative, government often ends up carrying it anyway.

- Link private participation to transparent public value capture. Private finance works better when the public sector has a stable land-based or user-based revenue stream behind the project.

For jurisdictions reviewing legacy tax structures, the debate shouldn't stop at PPP design. It should extend to the tax base itself, especially where property tax reform options can reduce bias against construction and productive land use.

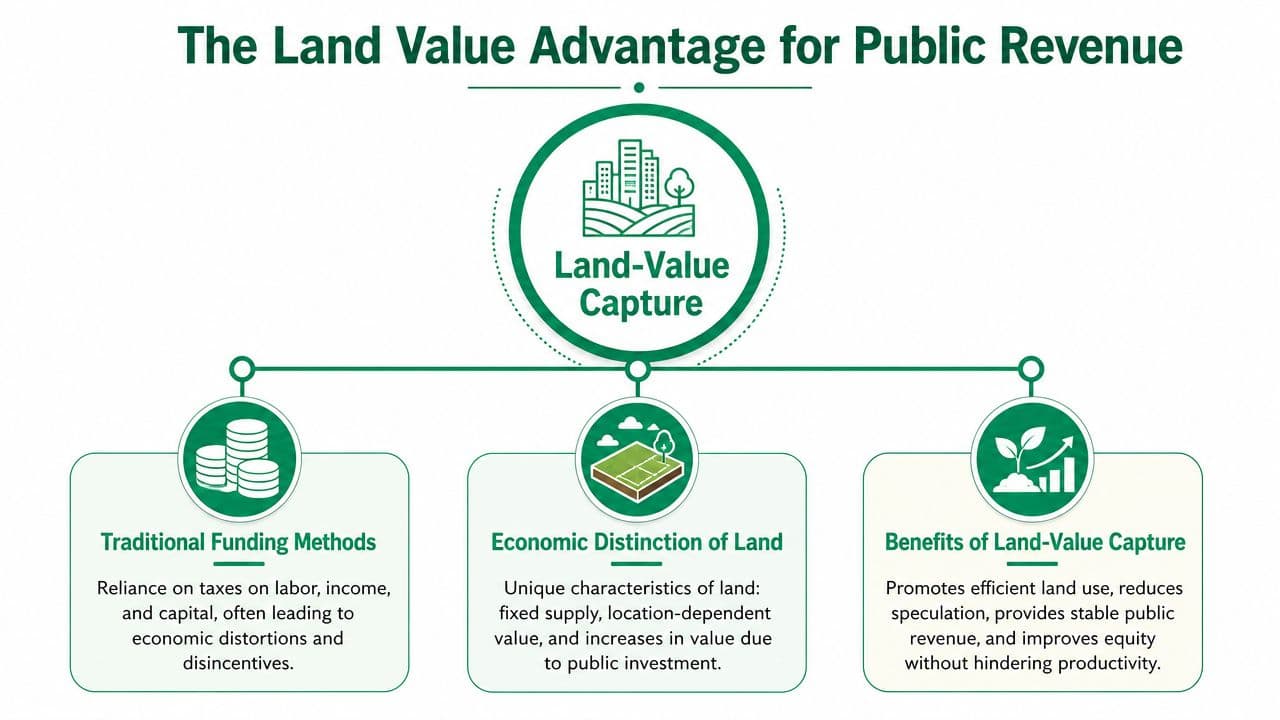

The Land Value Advantage for Public Revenue

The strongest argument for land-based revenue is not moral. It is fiscal.

Why land is fiscally different

Land has a distinct economic character. Governments don't create labor. Firms create capital by saving and investing. But location value often arises from public decisions and community growth. Zoning, roads, transit stations, schools, flood control, utilities, and basic public order all shape what a site is worth.

That makes land-based revenue unusually efficient. A ministry can recover value from a tax base that doesn't relocate, doesn't disappear when taxed, and doesn't depend on reducing employment or discouraging construction. By contrast, taxes on earnings, sales, and improvements can drive avoidance, delay investment, or push development outward.

The standard infrastructure funding debate often stalls because many policymakers accept the broad case for land-value capture, but they still assume the only practical route is an annual land-value tax. That assumption is too narrow.

Why public investment should recycle into public revenue

Public works often increase nearby land values before they increase fiscal capacity. If government leaves that uplift largely private while financing the project from labor and capital taxes, it creates a structural mismatch. The public creates place value, private owners receive much of the gain, and workers and firms fund the bill.

A better principle is straightforward:

- Fund location-enhancing infrastructure from location-based value

- Reduce taxes on productive effort

- Create a revenue stream that grows with actual land use and public service demand

This approach also improves economic behavior. Owners have stronger incentives to bring well-located sites into use when passive gains are no longer fully privatized. Builders face fewer penalties if governments reduce taxes on structures and transactions. Ministries gain a base that is tied to urban success rather than detached from it.

A tax system works better when it charges for exclusive access to valuable locations instead of charging for adding homes, jobs, and productive capital.

That logic aligns closely with a broader program of productivity-focused tax design. But once a government accepts the land-based premise, it still has a design choice. It can tax assessed land values each year, or it can grant and price rights to use land on defined terms. The second route is often more stable.

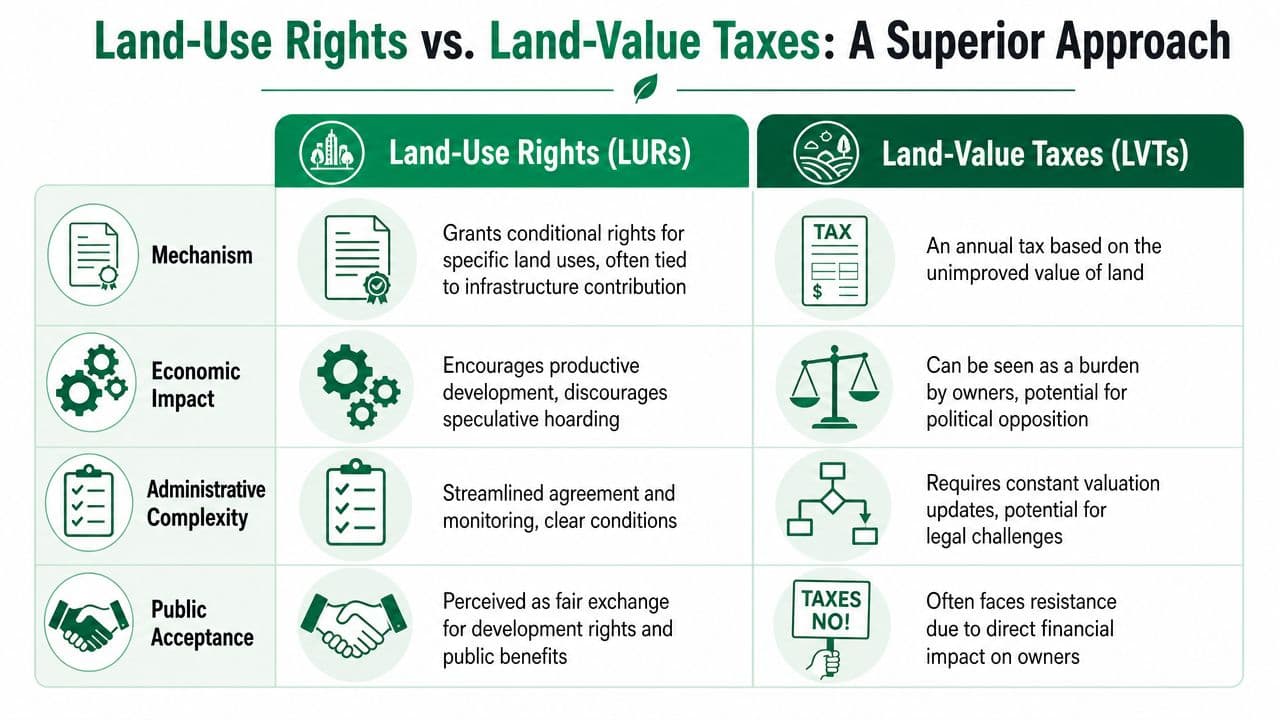

Why Land-Use Rights Outperform Land-Value Taxes

The most important choice in land-based infrastructure funding is often framed too crudely. Land-value taxes and land-use rights both seek to recover land value for public purposes. They are not the same instrument, and they don't produce the same fiscal behavior.

What land-use rights are

Land-use rights are a legal arrangement in which the state retains underlying ownership of land but grants an individual or firm the exclusive right to use that land for a specified purpose and term. Payment takes the form of a lease premium, annual rent, development charge, or another use-linked obligation. The core principle is simple: the public grants a valuable right, and the user pays for that right.

That differs from a land-value tax, which typically charges an annual levy on the assessed market value of unimproved land. The tax is linked to valuation, not necessarily to active use, development milestones, or a specific grant of public permission.

For infrastructure funding, this distinction matters because ministries need revenue systems that are predictable, administrable, and politically durable. Land-use rights can deliver all three when drafted well.

Why annual land-value taxes create avoidable friction

Annual land-value taxation has attractive features in theory. It targets a relatively inelastic base and can discourage idle holding. But in practice, it can create recurring conflict over valuation, annual reassessment, and payment burdens tied to market swings rather than use conditions.

That introduces several problems:

- Valuation volatility: owners focus on disputed appraisals rather than development performance.

- Political resistance: annual tax bills are highly visible, even when the underlying public logic is sound.

- Administrative load: governments need repeated reassessment systems and appeals capacity.

- Weak linkage to public bargains: the charge may feel disconnected from a clear grant of development rights or infrastructure access.

Land-use rights can avoid much of this friction because they price a legal permission, not an endlessly contested estimate of current market value. They also let governments attach explicit obligations on timing, permitted uses, infrastructure contribution, and renewal terms.

What Singapore and Allentown reveal

A useful comparison comes from two very different models. In Singapore, the state owns approximately 90% of land and allocates use via 99-year leases, with rent set at the time of lease grant. In Allentown, Pennsylvania, a split-rate land-value tax applies a 4.7% rate on current land value, which taxes fluctuating market value even if a site remains unused, according to the cited comparison in this discussion of land-value tax practice.

The policy lesson isn't that every country can or should replicate Singapore's land ownership structure. It's that pricing access to land through a long-term right can be more stable than taxing assessed value every year.

Under a land-use-rights model, the ministry can define:

-

Term

How long the right lasts, and what happens at renewal. -

Use conditions

Whether the site is for residential, industrial, logistics, energy, or mixed use. -

Payment structure

Whether the charge is upfront, annual, or staged alongside development. -

Performance obligations

Whether failure to build, maintain, or activate the site triggers penalties or reversion.

That structure creates a clearer exchange. The public grants a scarce and valuable right. The user receives security for productive activity. The state secures revenue without relying on annual valuation contests.

Policy test: If a land-based instrument can be written as a clear development contract rather than an annually disputed tax bill, ministries should prefer the contractual version.

Land-use rights also fit infrastructure sequencing better. Governments can tie rights to serviced land, transit-oriented development, port logistics zones, energy corridors, or urban regeneration sites. Revenue can be linked to the moment public investment makes use rights more valuable. That is a closer fiscal match than waiting for annual assessments to capture rising site values imperfectly.

For ministries looking at long-duration public land and infrastructure strategy, the practical implications of 99-year land leases are more relevant than most annual tax debates admit. The objective isn't to maximize tax cleverness. It's to create a stable public claim on location value while encouraging timely, productive use.

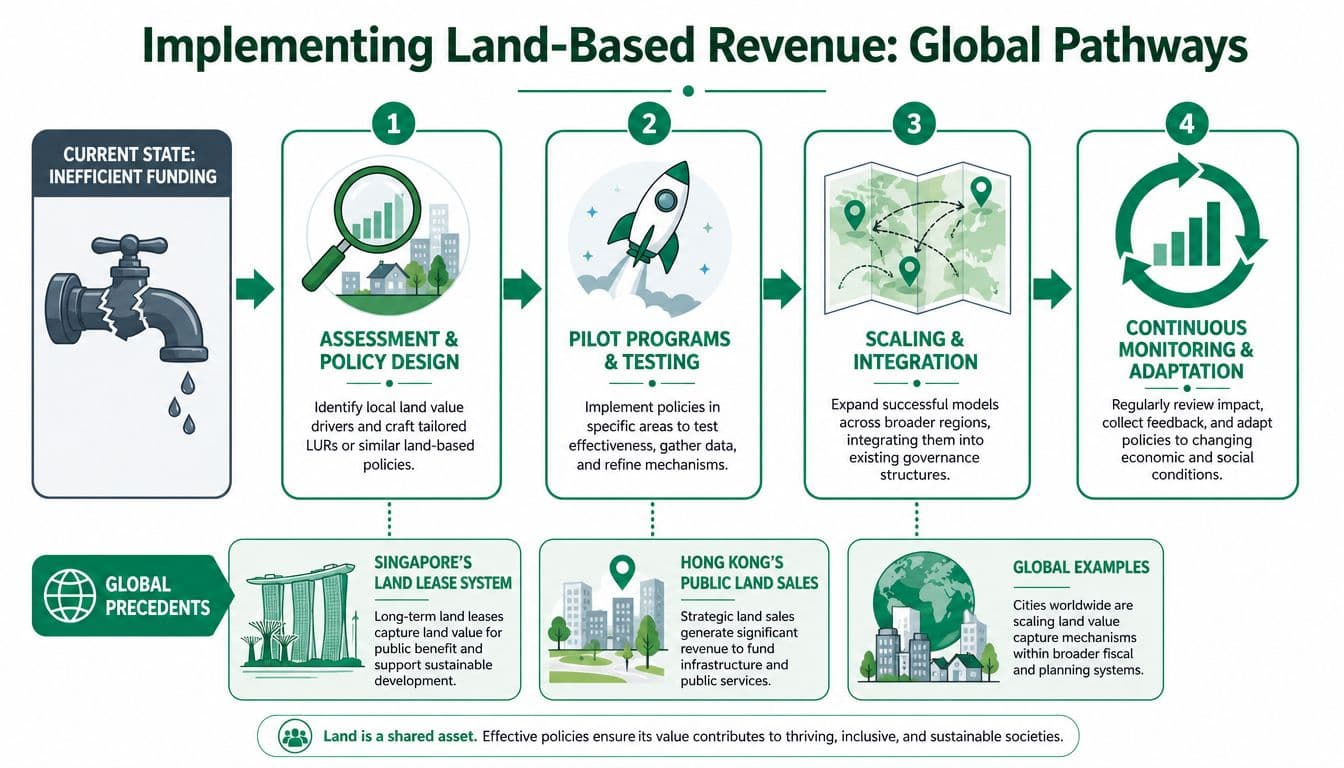

Global Precedents and Implementation Pathways

Land-use-rights logic is not confined to one city-state or one legal tradition. Different jurisdictions have used leasehold, development charges, and use-linked obligations to secure public value from land while avoiding some of the instability built into annual market-based taxation.

Canberra and South Korea as policy templates

Canberra offers a particularly relevant precedent for finance ministries considering predictable lease-based systems. In Canberra, land is leased for 99 years with an annual land rent fixed at the time of lease grant and adjusted only upon transfer or renewal. This avoids the disincentive for long-term holding that can arise under an annual land-value tax based on fluctuating market value, as described by the Federal Highway Administration fact sheet on land value capture tools.

That matters for infrastructure finance because stable lease conditions support long-range planning. Governments can forecast payments more clearly. Users can invest with greater certainty. The public side doesn't need to turn every budget cycle into a valuation dispute.

South Korea provides a different model. Its reform used a development surcharge tied to active development and a penalty structure for failure to develop within a defined period, as described in the verified data. The design principle is notable: public charges were linked to actual development behavior, not merely passive ownership.

These precedents suggest that the core policy variable is not whether government captures land value. It is whether the capture method rewards use and enforces timely development.

A practical pathway for finance ministries

Most governments won't begin with wholesale tenure reform. They should begin where land value is already being reshaped by public investment.

A practical pathway looks like this:

-

Start with infrastructure-defined zones

Focus on transit corridors, logistics hubs, industrial parks, port land, urban extensions, or regeneration districts where public works clearly increase location value. -

Convert vague uplift into formal rights

Instead of relying only on general taxation, create explicit use rights, lease conditions, or development agreements tied to those sites. -

Match payment timing to project economics

Some projects suit upfront premiums. Others need annual ground rent, staged obligations, or development-triggered charges. -

Write enforceable use conditions

Include build-out timelines, service obligations, reversion clauses, and penalties for land banking. -

Integrate with fiscal analysis early

Ministries should model baseline revenue, transition effects, and distributional outcomes before launching pilots. That's where fiscal impact analysis for land-based reform becomes essential.

Governments should pilot land-based revenue where public investment already creates visible site value. That is where political explanation is easiest and fiscal logic is strongest.

The implementation challenge is less technical than institutional. Finance ministries need treasury officials, land agencies, planners, transport authorities, and legal drafters working from the same revenue logic. If they don't, infrastructure funding remains fragmented. Capital projects proceed, land values rise, and the fiscal benefit leaks away.

A Design Checklist for Future-Proof Funding

The next generation of infrastructure funding won't be defined by one instrument. It will be defined by whether ministries can combine efficient delivery, private participation, and a stronger claim on land-based value without deterring productive investment.

In 2025, the five dominant trends reshaping infrastructure finance are blended finance, sustainable instruments, digitalization, evolving PPPs, and local currency deepening, and over 50% of 2024 private investment was classified as green, according to this overview of infrastructure finance trends in emerging markets. Those trends are important, but they don't answer the fiscal base question on their own. A ministry still needs recurring revenue that is stable, visible, and aligned with public value creation.

Six tests for policy design

-

Choose the right base

Prioritize revenue tied to land use, location value, and public permissions before increasing taxes on labor, buildings, or transactions. -

Prefer rights over recurring valuation disputes

If a land-use-rights model can achieve the same objective as an annual land-value tax, it will often be simpler to administer and easier to defend politically. -

Link charges to actual public investment

The clearest cases are sites whose value rises because of transport, utilities, flood protection, or other public works. -

Write obligations, not just fees

Strong systems specify use, duration, development timing, renewal, and penalties for non-performance. -

Protect transparency

Ministries should publish the logic of the charge, the permitted use, and the infrastructure purpose it supports. -

Plan the transition

Reform works best when governments phase down taxes that penalize work and construction as land-based revenue comes onstream.

The central lesson is simple. Governments don't need to choose between growth and infrastructure. They need a funding model that stops taxing the very activity they want to expand and starts recovering more of the value that public action creates in land.

Unitism® helps governments and public institutions design that transition. Its work focuses on land-based public revenue, tax reform, valuation frameworks, fiscal modeling, and implementation support grounded in tri-factor economics. For ministries looking to replace distortionary taxes with more stable land-based funding, explore Unitism®.