Explore fiscal sustainability with our guide for policymakers. Learn key metrics, risks, and how land-value capture can create stable, resilient public finance.

July 9, 2026

Fiscal Sustainability: A Policymaker's Guide for 2026

Explore fiscal sustainability with our guide for policymakers. Learn key metrics, risks, and how land-value capture can create stable, resilient public finance.

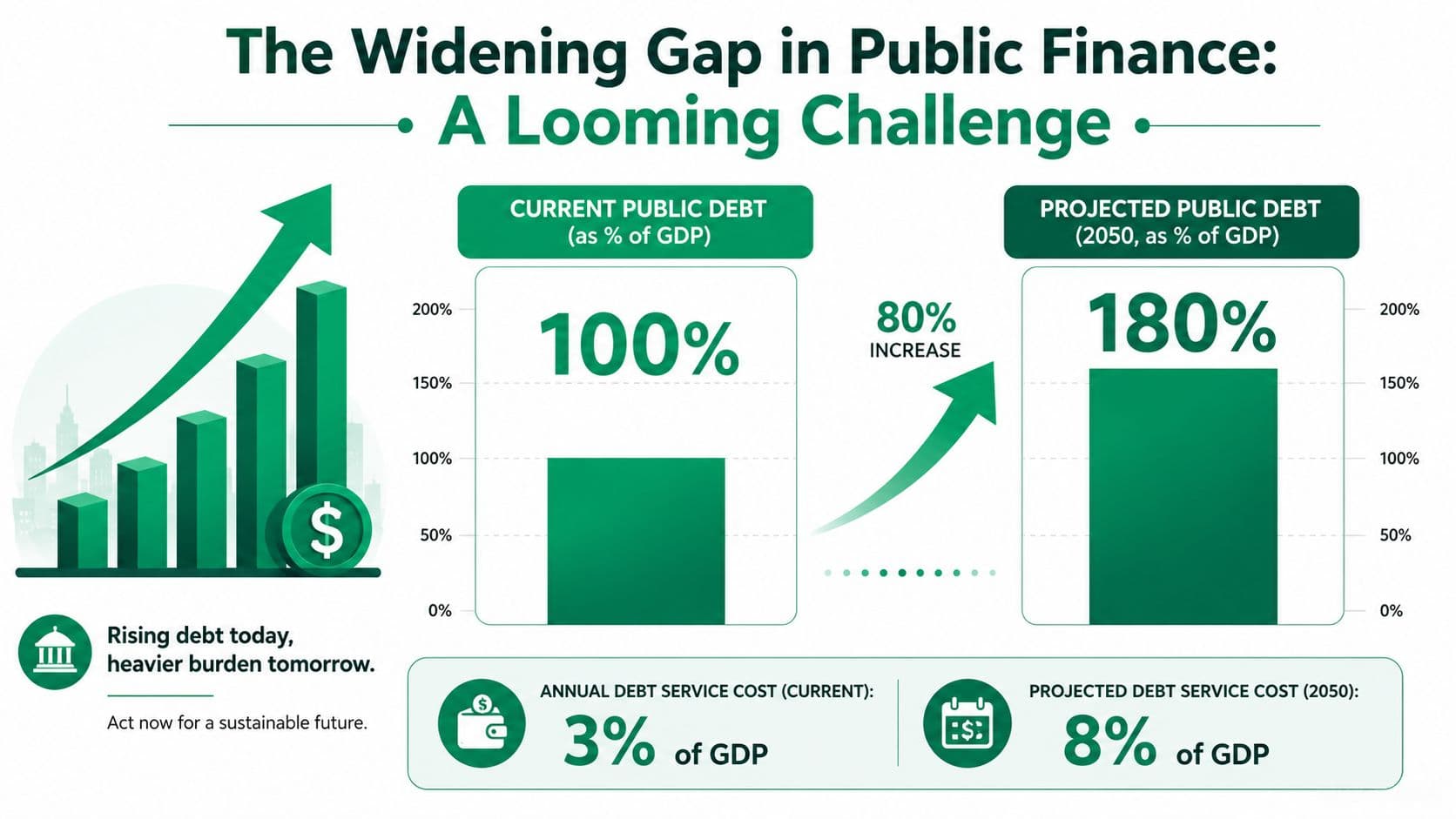

Fiscal sustainability stops sounding abstract when you look at the trajectory. Under unchanged U.S. fiscal policy, federal debt is projected to exceed 200 percent of GDP by 2046 and reach 566 percent by 2097, and closing that long-run gap would require spending reductions and revenue increases totaling about 4.9 percent of GDP over the period, according to the U.S. Bureau of the Fiscal Service's 2022 Financial Report.

Most fiscal debates still treat this as a narrow problem of deficits, entitlements, or tax rates. That framing is incomplete. From a land-economics perspective, the deeper question is whether a government relies on stable, productive tax bases or on revenue streams inflated by property cycles, speculative holding, and distorted land markets.

A government can balance a budget for a time and still be on an unstable path. If the tax base is fragile, if housing costs are being driven by land speculation, and if public revenue rises and falls with real estate cycles, fiscal sustainability becomes less about accounting technique and more about political economy. That's where conventional models often miss the core instability.

Table of Contents

- The Widening Gap in Public Finance

- Defining and Measuring Fiscal Sustainability

- The Hidden Drivers of Fiscal Instability

- Strategic Policy Levers for Long-Term Stability

- International Precedents and Distributional Impacts

- Modeling the Transition to a Land-Based Fiscal System

- Recommended Next Steps for Policymakers

The Widening Gap in Public Finance

A long-run fiscal correction equal to nearly 5 percent of GDP is not a marginal budget problem. It is evidence that the current revenue model and expenditure path are drifting apart in ways that standard debt debates often understate.

For finance ministries, the immediate concern is not only the stock of debt. The larger issue is declining fiscal room. As borrowing absorbs a greater share of future revenue, governments have less capacity to maintain infrastructure, respond to recessions, or protect household incomes during shocks. This reframing turns a political debate into a management problem. Which parts of the tax base remain dependable under stress, and which parts erode when asset markets reverse?

Why the standard debate is too narrow

Conventional discussions usually frame fiscal repair as a choice between lower spending and higher taxes. That framing misses a more consequential distinction. Revenue can be large in aggregate and still be poorly designed if it suppresses work, investment, or building activity while allowing land rents and speculative gains to accumulate with limited public capture.

That design flaw becomes visible during property cycles. Governments often tax transactions, wages, and improvements more heavily than the underlying site value that rises because of public infrastructure, zoning decisions, and metropolitan growth. The result is a revenue system that penalizes production and leaves budgets exposed to real estate booms and corrections. That is the core instability conventional models often miss.

Local policy illustrates the point. Unitism's analysis of the District of Columbia homestead exemption shows how homeowner relief, assessment rules, and land incentives interact. These are not separate housing and budget questions. They are the same fiscal question viewed from different balance sheets.

Forecasting problems reinforce the gap. Budget offices routinely project revenue from income, sales, and transactions with more confidence than they can justify when land prices are driving household debt and local tax receipts. Better scenario design, including methods outlined in this forecasting accuracy guide, improves administrative performance, but forecasting alone cannot stabilize a tax base built on volatile asset conditions.

Fiscal sustainability depends on whether revenue holds up when credit tightens, land prices stall, and demand for public services rises.

The intergenerational issue

The costs are distributed unevenly over time. Older owners often benefit from capitalized land gains created by public investment and scarcity, while younger households face higher entry costs, higher rents, and later tax increases when governments backfill weak revenue systems with additional borrowing.

A land-economics lens changes the diagnosis. It directs attention away from debt as a stand-alone outcome and toward fiscal architecture. Governments that rely too heavily on taxing labor, enterprise, and property improvements narrow their own future tax base. Governments that recover a larger share of publicly created land value can reduce speculative pressure, broaden housing access, and build a more stable foundation for public finance.

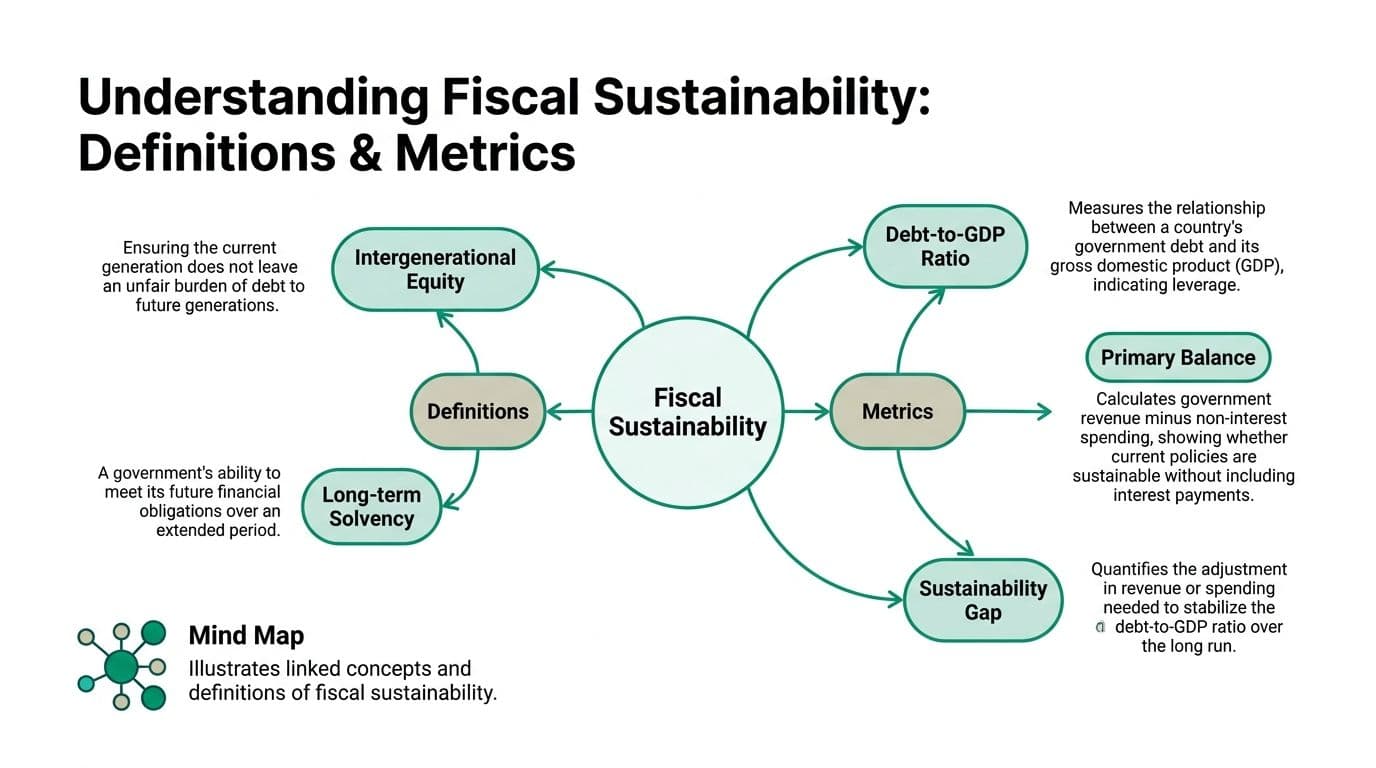

Defining and Measuring Fiscal Sustainability

Policymakers need a usable definition, not a slogan. In operational terms, fiscal sustainability asks whether a government can continue its current policy path without debt growing faster than its capacity to carry it. The concept becomes measurable when finance officials compare what the budget is doing now with what would be required to stabilize debt.

The central benchmark is the debt-stabilizing primary balance. The IMF describes fiscal sustainability as commonly assessed by comparing the actual primary budget balance with the balance needed to keep public debt constant at its current level. If the actual balance is below that threshold, debt rises, which indicates unsustainability, as explained in this IMF discussion of debt-stabilizing primary balances.

The metric that matters most

A household analogy helps. If a family can pay daily expenses but must borrow more each year just to keep existing obligations in place, the budget isn't stable. The same logic applies to governments. The primary balance strips out interest costs and asks a cleaner question: before debt service, is fiscal policy strong enough to prevent debt from drifting upward?

A simple policy reading of that framework looks like this:

- Actual primary balance: What the government collects and spends before interest payments.

- Debt-stabilizing primary balance: The balance needed to stop debt from rising relative to the economy.

- Sustainability gap: The distance between those two positions.

That framework matters because it turns a political debate into a management problem. Officials can test whether a new spending commitment, tax cut, or downturn would push the jurisdiction further below the stabilizing threshold.

Why measurement quality changes policy choices

Not all fiscal projections are equally useful. If baseline assumptions are weak, governments can underestimate risk and delay course correction. Technical teams that want better scenario work can learn from forecasting disciplines outside public finance. A concise forecasting accuracy guide from PlotStudio AI is useful here because it focuses on model discipline, error checking, and the consequences of poor baseline design.

That matters for land economics as well. If property-related revenue is volatile or inflated by speculative prices, debt sustainability metrics can look healthier than they really are. Better forecasting must therefore separate recurring, durable revenue from revenue that only appears strong during a land-price upswing.

Practical rule: Don't treat cyclical property windfalls as structural fiscal capacity.

Officials running this kind of analysis often need parcel-level and budget-level integration, not just macro ratios. That's why tools such as fiscal impact analysis are important in practice. They help ministries and municipalities test whether new development, changing assessments, and different tax designs strengthen long-term fiscal sustainability or just shift burdens around the map.

The Hidden Drivers of Fiscal Instability

Conventional fiscal risk analysis usually starts with aging populations, healthcare costs, pension liabilities, and interest rates. Those pressures are real, but they don't explain why local and regional finances can look healthy during a boom and suddenly deteriorate when property markets reverse. Land speculation often sits underneath that pattern.

Why land speculation disrupts budgets

When governments lean on taxes or fees tied to inflated land markets, they can mistake cyclical gains for permanent fiscal capacity. In practical terms, that's like treating lottery winnings as salary. The budget expands, debt looks serviceable, and policymakers defer structural reform. Then land turnover slows, values reset, and the revenue that supported recurring commitments weakens.

This isn't just a theoretical concern. A major gap in existing fiscal sustainability models is their failure to account for land-value speculation as a primary driver of fiscal volatility. In major markets such as the U.S., Canada, and Australia, real-estate-driven fiscal shocks contributed to 30 to 40 percent of local budget stress test failures in recent data, yet only 12 percent of fiscal sustainability advisories referenced land economics as a core variable, according to this IMF-linked discussion of land and fiscal volatility.

What conventional models leave out

Traditional frameworks are strong on debt arithmetic and weaker on tax-base composition. They tell you whether debt is climbing, but often not whether the tax base itself has become more speculative, less productive, or more regressive.

Three blind spots matter most:

- Speculative appreciation: Rising land prices can create the appearance of broader prosperity even when the productive base hasn't improved.

- Revenue fragility: Budgets become exposed when transaction-driven or bubble-sensitive receipts finance ongoing services.

- Housing distortion: High land costs crowd households and productive firms while rewarding passive landholding.

A sharper approach treats land markets as a fiscal variable, not just a housing variable. That perspective aligns with the broader problem of rent seeking in economics, where private actors capture value created by community growth, public infrastructure, and legal privilege rather than by new production.

A city can post strong receipts during a property upswing and still be becoming less fiscally sustainable.

That's the hidden instability. When public finance depends too much on land-price inflation rather than land-value capture, officials end up governing the cycle instead of governing the system.

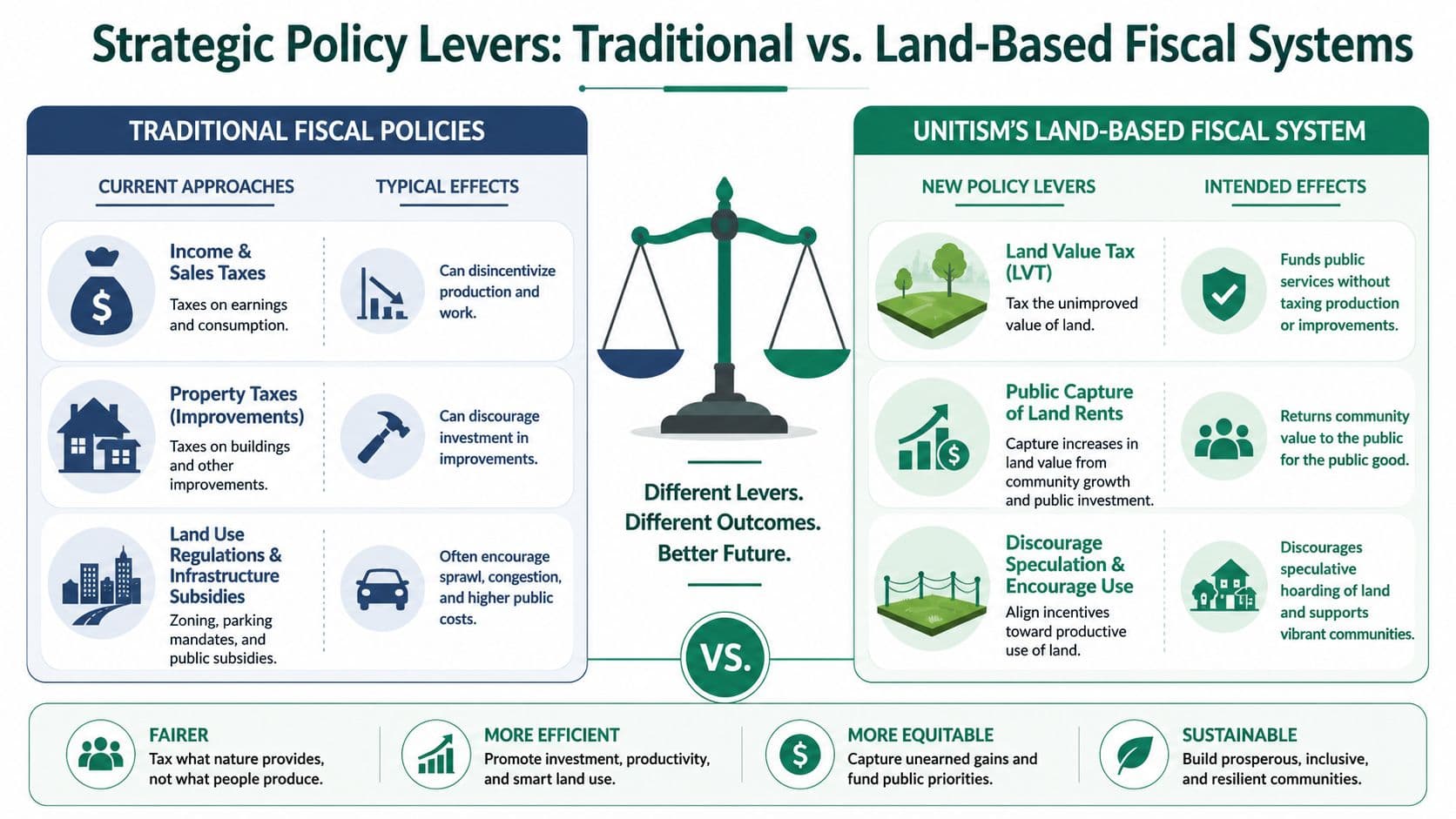

Strategic Policy Levers for Long-Term Stability

If speculation in land is part of the instability, the revenue system has to change at the base. The most effective levers are the ones that shift taxation away from productive activity and toward location value, monopoly rents, and other forms of unearned gain that the public sector helps create.

Why land-based revenue is structurally different

A land value tax has an unusual fiscal property. It doesn't shrink its own base through reduced supply because land is fixed in quantity. The IMF has confirmed this efficiency logic, and modeling for Richmond, Virginia, showed that a shift to land value taxation could maintain revenue while allowing residents to save up to $19 million annually, as discussed in this IMF working paper on land value taxation and property reform.

That's important for ministers deciding where to raise marginal revenue. Taxes on labor can reduce work incentives. Taxes on business investment can deter upgrades and expansion. Taxes on buildings can penalize construction and maintenance. A tax on the unimproved value of land works differently because it targets value that owners didn't produce alone.

A better fiscal mix

For long-term fiscal sustainability, the policy goal isn't only to add an LVT to an already overloaded tax code. It's to build a better mix. In practice, that means pairing land-based revenue with reductions in taxes that suppress productive activity.

A workable reform package often includes:

- Site-value taxation: Shift the burden from structures to land so governments stop penalizing development and reuse.

- Land value capture around public investment: Recover part of the uplift generated by transit, rezoning, and infrastructure.

- Resource and location rents: Where applicable, collect public value from natural advantages rather than taxing earned income more heavily.

The political advantage is often underestimated. A land-based system can be framed not as austerity, but as fiscal repair through better incentives. Officials can preserve revenue, reduce distortions, and discourage speculative vacancy at the same time.

One practical route is to redesign the local property tax base rather than inventing an entirely new instrument. That's why property tax reform often becomes the administrative bridge. Assessment systems, cadastres, appeals processes, and billing mechanisms already exist. What changes is what government chooses to tax most heavily.

There's also an institutional point. Public budgets rise and fall with location value because public action helps create location value. Transit, schools, safety, planning decisions, and business clustering all feed into land rents. Capturing more of that value for public use is not a novel burden on production. It is a correction to an existing leakage.

Where governments want technical support for distributional analysis, valuation, and phased implementation, Unitism® is one option among several advisory providers. Its work focuses on land-value capture, site-value taxation, and fiscal modeling grounded in land economics.

International Precedents and Distributional Impacts

Skeptical officials usually ask two questions. Has this worked anywhere, and who ends up paying? Those are the right questions because a fiscally sound reform still fails if administrators can't implement it or if the burden falls in a politically untenable way.

What real-world reform looks like

The practical lesson from international precedent is not that every country uses the same instrument. It's that jurisdictions repeatedly return to land-based revenue when they need a tax base that is harder to hide, harder to offshore, and more aligned with efficient land use.

Denmark is often discussed because land taxation there has remained part of the live policy toolkit rather than a historical footnote. Estonia has also maintained a clear separation between land and improvements in ways that keep the tax conversation focused on underlying site value. Singapore, though institutionally distinct, demonstrates a broader principle: governments that actively shape and recapture land-related value gain far more fiscal control over infrastructure, housing, and long-term development.

In the United States, Allentown, Pennsylvania, is frequently cited in debates over split-rate taxation because it illustrates a politically accessible path. Instead of presenting reform as a wholesale replacement of the revenue system, officials can shift relative tax burdens within the property tax itself. That makes the reform legible to assessors, councils, and taxpayers.

The most durable reforms usually begin where administration is already strongest, not where theory is purest.

Who benefits and who resists

The distributional effects are usually more favorable than critics assume, but only if the reform is designed carefully. A tax system that falls more heavily on land value tends to benefit households and firms that are using land productively while placing more pressure on owners who hold valuable sites idle or underused.

That changes the political map:

| Group | Likely effect under well-designed land-based reform |

|---|---|

| Productive homeowners | Often protected or improved through rebalancing and targeted relief |

| Builders and renovators | Face less penalty for adding or improving structures |

| Small businesses on modest sites | Often benefit when taxes shift away from improvements and transactions |

| Speculative landholders | Face stronger carrying costs on idle or underused locations |

The usual opposition comes from actors who benefit from scarcity, appreciation, or strategic underdevelopment. That doesn't make reform anti-investment. It makes reform anti-rent extraction.

A second concern is fairness for cash-constrained owners. That issue is manageable through deferrals, circuit breakers, phased transitions, and homestead protections. The principle matters. Fiscal sustainability should not be purchased by forcing hardship on asset-rich but income-constrained residents. Good design distinguishes between discouraging speculation and destabilizing occupancy.

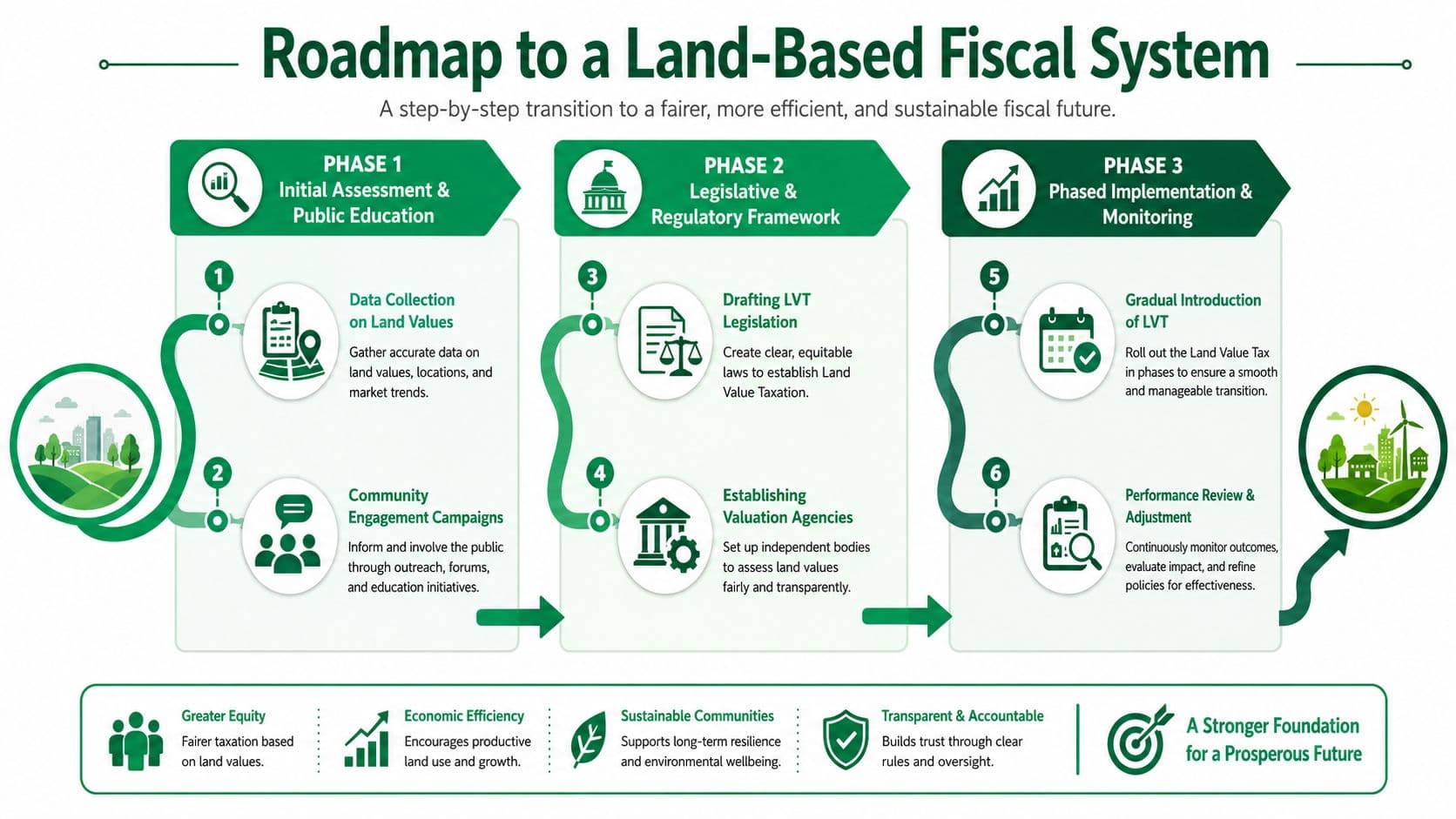

Modeling the Transition to a Land-Based Fiscal System

The biggest implementation mistake is trying to treat reform as a one-step tax swap. Land-based fiscal reform works best when governments build valuation capacity, model effects in detail, and phase changes against administrative readiness.

A practical transition sequence

A serious transition usually follows three tracks at once.

-

Valuation first. Governments need parcel-level estimates that isolate land value from improvement value. Without that distinction, the reform remains rhetorical. Methods discussed in technical resources such as how to calculate land value are useful because they focus on the mechanics officials need for implementation.

-

Fiscal and distributional modeling. Before legislation moves, teams should test revenue neutrality, sectoral impacts, neighborhood effects, and appeals exposure. Scenario design is most critical during this phase.

-

Phased rate adjustments. Governments can increase land-based charges gradually while reducing taxes on buildings, capital, or labor in tandem.

The macro case for this transition is stronger than many officials assume. Empirical modeling cited by the Lincoln Institute indicates that increasing the land tax rate from 0.55% to 5.55% while reducing taxes on capital and labor by 28% and 10% respectively could raise national output by 15% relative to trend, according to this SUERF brief discussing green land value taxation and Lincoln Institute modeling.

Why phased reform outperforms sudden reform

Phasing isn't political caution alone. It's better policy. Gradual implementation allows assessors to improve land-value maps, lets finance teams monitor incidence, and gives taxpayers time to adjust asset and development decisions.

For policymakers tracking international implementation detail, especially in European contexts, this essential guide for UK property investors is a helpful practical reference because it shows how land-tax rules are interpreted by market participants, not just by theorists.

A well-run transition should include:

- Public education: Explain that the reform shifts the base, not just the bill.

- Administrative rehearsal: Test appeals, billing systems, and assessment updates before full rollout.

- Policy offsets: Pair new land charges with visible reductions elsewhere so households and firms can see the tradeoff.

Reform succeeds when officials can show, parcel by parcel and district by district, how the burden changes and why.

Recommended Next Steps for Policymakers

Governments don't need to solve the entire fiscal problem in one budget cycle. They do need to stop relying on frameworks that ignore how land speculation distorts both housing markets and revenue systems. Fiscal sustainability becomes more credible when tax design, valuation practice, and land policy are treated as one strategic field.

A practical agenda starts with diagnosis, not ideology.

Immediate actions that move the issue forward

- Commission a land-value baseline: Establish whether the jurisdiction can separate site value from improvement value with current data systems.

- Run a revenue-neutral reform model: Test how much of the existing burden on buildings, transactions, labor, or business activity could be shifted toward land value.

- Stress test fiscal exposure to real estate cycles: Identify where current revenue depends too heavily on speculative appreciation or land turnover.

- Design protections early: Build homestead relief, deferral options, and transitional rules before opponents define the reform as indiscriminate.

- Align finance and planning teams: Tax policy, assessment, zoning, and infrastructure finance should work from the same land-value map.

The deeper conclusion is straightforward. Durable fiscal sustainability won't come from accounting fixes alone. It requires a revenue system that captures socially created value without suppressing work, construction, and productive investment. Once policymakers recognize land speculation as a fiscal variable, not just a housing issue, a wider set of stable and fair policy options becomes available.

If your government is assessing land-value taxation, property tax redesign, or the fiscal effects of speculative land markets, Unitism® provides research, valuation frameworks, policy design, education, and implementation support for land-based public finance reform.