Explore the link between taxation and efficiency. Learn how to design tax systems that raise revenue without harming growth, with a focus on land value capture.

July 1, 2026

Taxation and Efficiency: A Guide for Policymakers

Explore the link between taxation and efficiency. Learn how to design tax systems that raise revenue without harming growth, with a focus on land value capture.

How do you raise enough revenue to fund a modern state without discouraging the work, investment, and development that generate that revenue in the first place?

That question exposes a gap in much of the taxation and efficiency debate. Policy discussions usually compare labor taxes with capital taxes, or income taxes with consumption taxes. They often skip a separate factor of production that behaves very differently from both labor and capital: land and nature. That omission matters. If policymakers treat land as just another form of capital, they miss one of the few tax bases that can finance public services with far less distortion.

For a finance ministry, tax efficiency shouldn't mean “lowest possible tax rates.” It should mean raising required revenue while minimizing changes in behavior that shrink welfare, reduce productive activity, or push costs into administration and compliance. A useful analogy is traffic management. The objective isn't to eliminate tolls or rules. It's to design them so that people still reach their destination with the fewest unnecessary detours, delays, and bottlenecks.

That is why deadweight loss matters. It captures the economic activity that disappears because taxation changes incentives. In practical fiscal terms, that means fewer projects that go ahead, fewer transactions that occur, or more resources spent avoiding tax rather than creating value. For ministries concerned with growth, housing, infrastructure, and revenue stability, this is not abstract theory. It is core budget design.

A narrower focus on capital formation often misses this third factor. The policy challenge is not solely how to encourage savings and investment, but how to do so while reducing the private capture of publicly created land rents. That distinction becomes clearer when capital and land are separated analytically, as in this discussion of capital formation.

Table of Contents

- Introduction

- Comparing Tax Bases Through an Efficiency Lens

- The Unique Efficiency of Land Value Taxation

- Addressing Distributional Impacts and Equity Concerns

- A Practical Framework for Implementing Land Value Capture

- Frequently Asked Questions on Taxation and Efficiency

Introduction

Tax systems fail when they chase revenue without asking what gets damaged along the way. A ministry can collect from wages, profits, sales, property transfers, and many other bases. But each base changes behavior differently. Some reduce work at the margin. Some deter investment. Some encourage avoidance. Some lock land into speculation rather than use.

That's why taxation and efficiency must be framed around distortion, not slogans. A tax can be politically popular and still economically wasteful. It can be administratively simple and still steer capital into low-productivity activity. It can even appear pro-growth while mostly shifting after-tax incomes rather than expanding output.

What efficiency actually measures

Economist Martin Feldstein argued that deadweight loss should sit at the center of tax policy analysis, alongside revenue estimates, because taxation can impose major efficiency costs through distortions in saving and investment behavior. His framework shifts the question from “How low is the rate?” to “How much distortion does the structure create?” as set out in his NBER working paper on the effect of taxes on efficiency and growth.

For a finance ministry, that leads to four practical tests:

- Deadweight loss: Does the tax reduce beneficial activity that would otherwise occur?

- Excess burden: Does the social cost exceed the revenue collected?

- Administrative cost: Can the state assess and collect it predictably?

- Compliance cost: How much time and effort do households and firms spend dealing with it?

Practical rule: A tax is efficient when it raises stable revenue with the least distortion to productive decisions.

The standard debate usually stops after labor, capital, and consumption. Tri-factor economics adds a more useful distinction: labor produces, capital produces, and land captures location-specific value that society largely creates. Once that distinction is clear, the policy ranking changes.

A ministry-level comparison framework

The ministry's task isn't to choose a single ideal tax. It's to build a portfolio of taxes where the most distortionary bases carry less weight and the least distortionary bases carry more. That means taxing mobile and behavior-sensitive bases more carefully, and taxing immobile rents more directly.

That distinction also matters for implementation. Data quality, parcel records, and valuation systems determine whether a theoretically efficient tax works in practice. Ministries building these capabilities often face the same integration problem seen in other fiscal systems. A useful operational reference is the benefits of integrating tax data APIs, especially where valuation, cadastre, and billing systems need to work together.

One more conceptual correction is necessary. Economists often speak of “capital” when they mean both produced assets and location values. That conflation obscures a major source of inefficiency: private gains from passive landholding. The underlying dynamic is closer to rent-seeking in economics than to productive investment.

Comparing Tax Bases Through an Efficiency Lens

The usual ranking of taxes assumes one main trade-off: how much labor and capital respond to tax rates. That's important, but incomplete. The stronger question is which tax base remains available to the state without shrinking when taxed. Labor can adjust. Capital can relocate, defer, or reclassify. Consumption can be postponed or shifted. Land can't move and its supply can't be reduced.

That difference changes how a ministry should think about tax mix.

Why the traditional ranking is incomplete

Research from the Center for Equitable Growth finds that tax changes in recent decades have mainly affected inequality and government revenue, not overall economic growth, and that cutting taxes on business owners and capital has rarely produced perceptible effects on investment. That directly challenges the common assumption that lower taxes on capital automatically improve efficiency through higher growth, as discussed in the Center's analysis of taxation and U.S. economic growth.

For policymakers, the implication is sharp. If tax cuts on capital don't reliably produce visible investment gains, then efficiency cannot be inferred from “lighter capital taxation” alone. It has to be assessed by the distortions avoided and the rents captured.

A system can look pro-investment on paper while mostly redistributing gains upward and leaving productive behavior little changed.

Efficiency Comparison of Major Tax Bases

| Tax Base | Deadweight Loss | Distortion Effect | Administrative Cost |

|---|---|---|---|

| Labor income | Moderate to high | Can discourage work, hours, formality, and reported earnings | Moderate |

| Capital income | Often significant | Can alter saving, investment timing, location, and legal form | High |

| Consumption | Lower than many income taxes in broad form, but still distortionary | Can affect spending patterns and burden lower-income households more heavily | Moderate |

| Land rental value | Qualitatively lowest | Does not reduce the supply of land and can push underused sites into better use | Moderate once valuation systems are established |

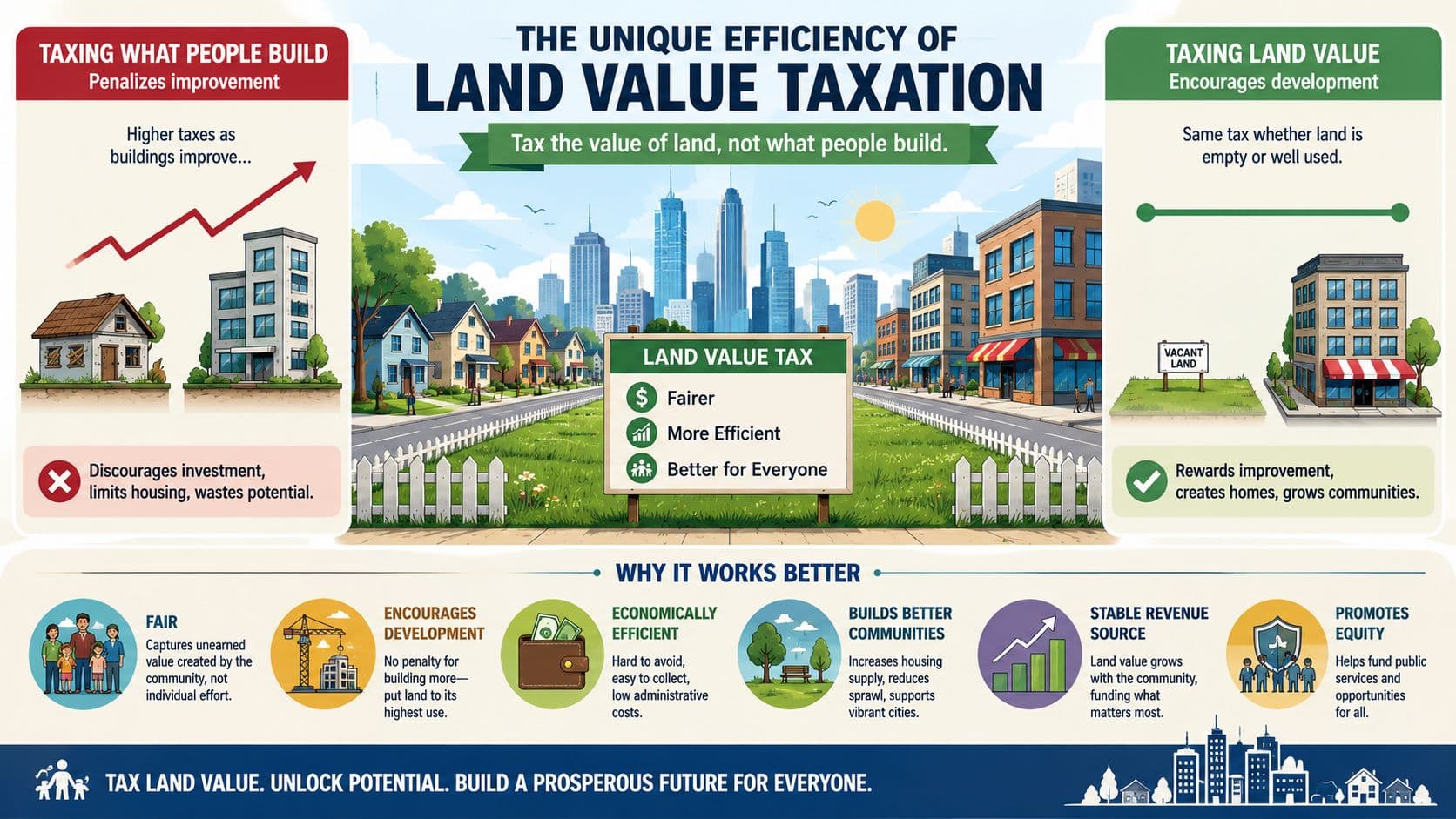

This table points to a conclusion that standard tax debates often miss. Land is not just another property tax base. Taxes on buildings can discourage construction and improvement. Taxes on transactions can suppress sales and mobility. Taxes on land value target the site itself, not the productive activity placed on it.

That distinction is central to current debates on property tax reform. A ministry that wants more housing, more infill, and fewer speculative vacancies shouldn't treat a tax on buildings as equivalent to a charge on land rents. The first can penalize development. The second can reward it by making idle holding more expensive.

A second implication follows. If a government reduces reliance on labor and productive capital while increasing reliance on immobile land value, it is not merely changing who pays. It is changing what the tax system rewards. Work and building become less penalized. Passive appreciation becomes less privileged.

That is the core efficiency advantage of treating land as a distinct factor of production.

The Unique Efficiency of Land Value Taxation

A tax on wages reduces the reward to work. A tax on buildings can reduce the reward to construction. A tax on capital returns can alter where and when firms invest. A tax on land value does something different. It claims part of the value of a fixed asset whose supply no one can increase or withdraw from the economy.

Why land behaves differently

Land value taxation (LVT) is economically efficient because the tax base is fixed in supply, which means it does not distort the quantity of land available. On that basis, LVT is widely described as generating zero deadweight loss, and in some cases it can create negative deadweight loss, meaning net social benefits, because it discourages speculative holding and pushes land toward use. The underlying rationale is summarized in this overview of land value taxation.

That phrase, negative deadweight loss, matters more than it first appears. It means the tax can improve allocation rather than merely fund the state. If owners hold vacant or underused urban land because expected appreciation exceeds carrying costs, the public absorbs the cost through sprawl, delayed housing supply, and infrastructure inefficiency. LVT changes that calculation. Owners either develop, sell, or use the site more intensively.

Tri-factor economics clarifies policy design. Labor should be rewarded for effort. Capital should be rewarded for production and risk-taking. Land rent, by contrast, often reflects location, public infrastructure, legal privilege, and community growth. Taxing that rent doesn't punish production. It recovers socially created value.

A ministry considering reform must therefore separate site value from improvement value. That requires rigorous assessment methods, not rough proxies. The practical starting point is understanding how to calculate land value independently from structures and business activity.

The real objection and the policy answer

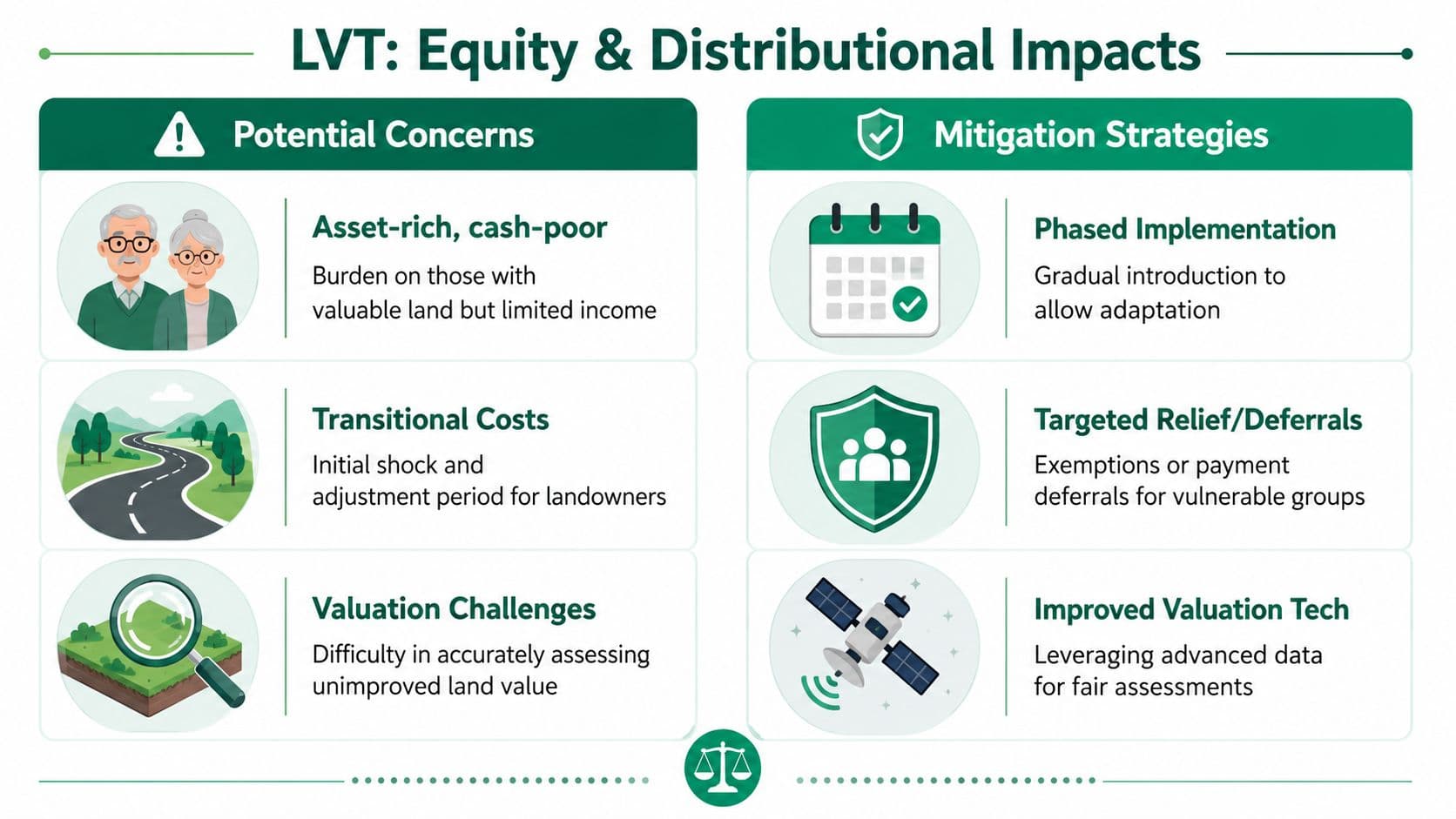

The strongest objection to LVT is not economic theory. It is distributional politics. Some households may hold valuable land but have limited current income. That concern is valid. It doesn't refute the efficiency case, but it does shape the design.

The correct response is not to abandon the tax base. It is to distinguish between the base and the payment schedule. A government can preserve the efficiency of land taxation while offering deferrals, roll-ups to the point of sale, or targeted relief for vulnerable owners. In other words, the ministry should protect cash flow without exempting land rent from the fiscal system altogether.

The policy mistake is to treat every hardship case as evidence against the tax base itself. Often it is evidence for better transition design.

That distinction matters because many current taxes are inefficient precisely where LVT is not. Transaction taxes deter movement. Building taxes deter improvement. Payroll taxes burden employment. If reform is blocked because vulnerable landholders need protection, the result is often a tax mix that harms the broader economy more while solving less.

Addressing Distributional Impacts and Equity Concerns

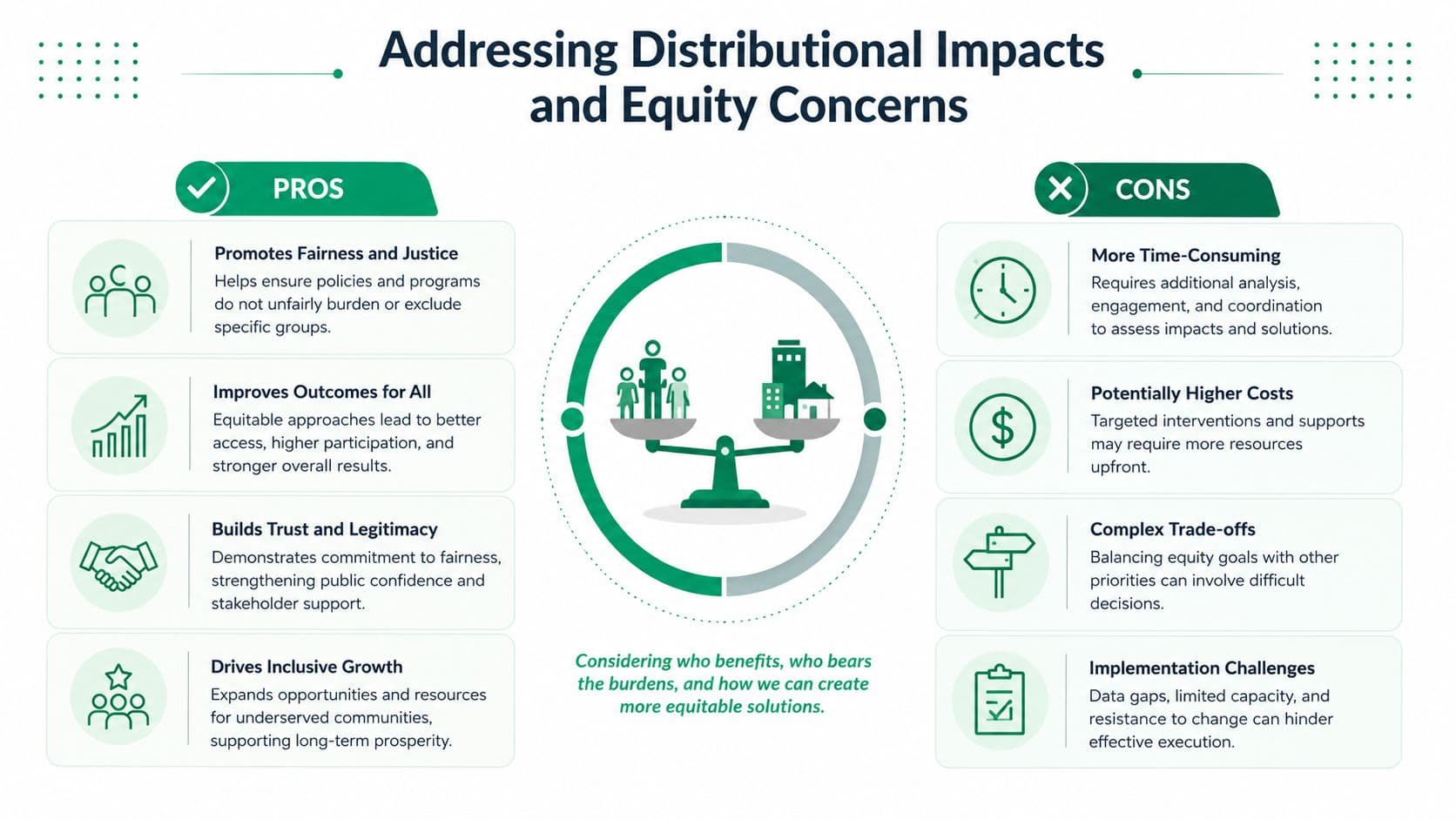

Efficiency arguments rarely survive contact with politics unless they also answer the household question: who faces the bill, when, and with what capacity to pay?

That is where many land-tax proposals fail. They win the economic argument but lose the implementation argument. Ministries speak about neutrality, fixed supply, and deadweight loss. Households ask whether a retired owner on a fixed income will be forced to sell. If policy teams can't answer that clearly, the reform won't hold.

Efficiency without equity won't hold

Recent work highlighted through the IMF's efficiency-oriented treatment of land taxation points to a neglected risk: without refund or deferral mechanisms, land value capture can raise effective burdens for asset-rich, cash-poor seniors. That gap between macro efficiency and micro fiscal stress is discussed in the IMF-linked material on land-area taxes and implementation concerns.

That finding should change how ministries frame reform. The question is not whether distribution matters after efficiency has been secured. Distribution is part of administrative feasibility, legal durability, and public legitimacy.

Three design responses are especially practical:

- Deferral for low-income owner-occupiers: Allow eligible households to postpone payment until sale or transfer. The tax base remains intact, while liquidity pressure falls.

- Circuit breakers tied to income: Cap current-year liability relative to household income. This addresses cash-flow strain directly.

- Phased implementation: Introduce reforms gradually where valuation changes are large or where previous systems undertaxed high-value sites.

These mechanisms don't weaken the logic of taxation and efficiency. They refine it. A tax is not efficient in any policy-relevant sense if social resistance makes it unstable, arbitrary, or politically reversible.

From equity concern to fiscal design

The deeper insight is that equity concerns can improve the design of land-based reform rather than derail it. Once a ministry identifies vulnerable owners, it can target relief far more precisely than under broad exemptions that also shield high-value land from public recovery.

That leads naturally to land value capture rather than a stand-alone debate about annual taxation. When public investment raises nearby land values, governments can recover part of that uplift to fund the infrastructure that created it. The burden falls less on households detached from the gain and more on beneficiaries of the publicly created increment.

Policy insight: Equity improves when governments stop asking general taxpayers to fund land value gains that accrue privately to specific sites.

This shifts the political narrative. Instead of “a new tax on owners,” the reform becomes “a rule that returns part of publicly created land value to the public budget.” For ministries managing infrastructure backlogs, that framing is not cosmetic. It links payment to benefit and turns a contentious reform into a fiscal reciprocity principle.

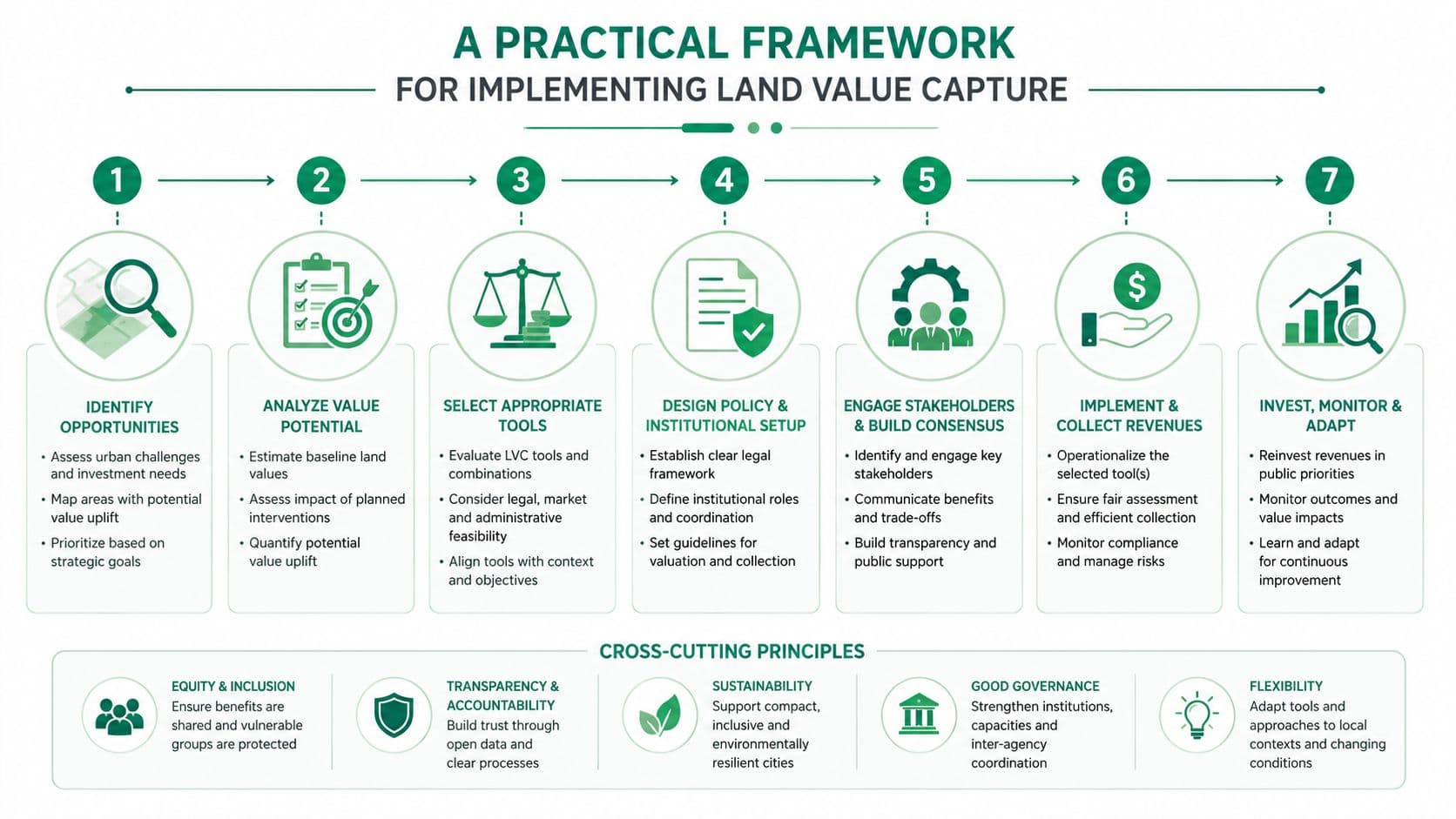

A Practical Framework for Implementing Land Value Capture

Land value capture works when governments treat it as a finance system, not a slogan. Public investments in transit, streets, utilities, and place-making often raise nearby land values. If the state doesn't recover part of that uplift, it finances the investment broadly while allowing a concentrated windfall to remain private.

Evidence summarized by the Inter-American Development Bank shows that Tax Increment Financing and betterment levies are among the most effective land value capture instruments for urban infrastructure, and case material from Denmark, Singapore, and Estonia shows these tools can stabilize municipal revenue, reduce real-estate-driven volatility, and promote infill development, as outlined in the IDB report on land value capture for financing urban projects.

What land value capture should fund

A ministry should prioritize land value capture where the public action and private uplift are closely linked. That usually includes:

- Transit corridors: New accessibility often capitalizes into nearby land prices.

- Urban realm upgrades: Street redesigns, flood protection, parks, and public services can alter location value materially.

- Rezoning and entitlement changes: Where planning decisions expand development rights, public policy itself creates a portion of the gain.

The principle is straightforward. Those who receive the clearest land-value windfall from public action should contribute to the cost of that action. That closes the fiscal loop and reduces pressure to rely on more distortionary taxes.

Seven implementation priorities

-

Map the legal base first. Identify whether current law permits site-value taxation, betterment charges, special assessments, or increment financing. Ministries often discover that legal fragmentation, not economic logic, is the first barrier.

-

Build a valuation system that isolates land from improvements. Administrative credibility depends on this. Parcel-level assessment, transparent appeals, and regular updates matter more than rhetorical support.

-

Model distribution before drafting rates. The ministry should test how burdens fall across owner-occupiers, landlords, developers, and institutional holders. In this context, fiscal impact analysis becomes indispensable.

-

Match the instrument to the project. A corridor-wide increment tool may suit transit. A one-time betterment levy may suit rezoning. A general annual site-value tax may suit national reform.

-

Protect vulnerable owners without exempting windfalls wholesale. Deferrals and targeted relief preserve legitimacy better than broad carve-outs.

-

Use revenue visibly. If proceeds fund transport, housing infrastructure, or local service upgrades, public acceptance strengthens because the benefit is observable.

-

Sequence reform with tax substitution where possible. Political support improves when land-based charges help reduce taxes on buildings, transactions, labor, or productive investment.

A practical question often follows: if land value capture works well, what happens to property prices? The likely effect is not mysterious. If government taxes away a larger share of future land rent, some of that rent is no longer capitalized into sale prices. That can bring land prices closer to underlying construction economics and weaken the speculative premium that distorts housing markets.

Frequently Asked Questions on Taxation and Efficiency

Policymakers usually agree on the principle of reducing distortion. The harder part is handling the edge cases. The following questions tend to determine whether reform moves from briefing papers into cabinet decisions.

Does progressive taxation always reduce efficiency

Not always in the same way, and not always in the same magnitude. Theory commonly holds that more progressive taxes create larger efficiency costs because deadweight loss rises with the tax rate squared. At the same time, recent discussion has pointed to an underexplored tension: targeted progressive taxes on high-income capital may offset some efficiency losses when they reduce speculative bubbles and stabilize revenue, as raised in this MIT lecture discussion of progressivity and the tau squared rule.

The ministry lesson is practical. Don't ask whether “progressivity” is efficient in the abstract. Ask which base is taxed, how responsive it is, and whether the tax reduces harmful speculation or productive activity.

Would land-based taxation raise or lower property prices

It depends on what part of property value you mean. Land-based taxation is designed to recover land rent. Where buyers expect future land rent to be taxed more heavily, that expectation can reduce the amount they are willing to pay upfront for the site. That tends to bear more directly on land prices than on the value of buildings or improvements.

For housing policy, that matters. If less speculative land rent is capitalized into price, governments can reduce one of the drivers of unaffordability without penalizing construction itself.

Can land revenue replace other taxes

In many systems, it should at least replace part of the most distortionary tax mix. The strongest case is not absolute replacement. It is marginal substitution. If each additional unit of land-based revenue allows a reduction in taxes on labor, transactions, or buildings, the overall system becomes more efficient and often more coherent.

That's the right way to frame reform publicly. The question is not whether land taxes can do everything alone. It's whether they can do more of the revenue work that current taxes do badly.

Why not rely only on broad consumption taxes

Because efficiency is not the only criterion. Broad consumption taxes can be relatively efficient in narrow public-finance terms, but they still change household behavior and often raise sharper distributional concerns. They also don't address land speculation, urban vacancy, or the private capture of publicly created site values.

A ministry that relies only on consumption taxation leaves a major rent base untouched and asks households to fund public services while landholders retain gains tied to public investment and urban growth.

The most durable system usually combines broad, administratively workable taxes with stronger recovery of immobile rents.

Taxation and efficiency become clearer when labor, capital, and land are analyzed separately. Once that distinction is made, the policy hierarchy shifts. Taxes on productive effort and mobile investment need careful restraint. Taxes on fixed land value deserve a larger role. And land value capture offers a practical route for doing that while funding infrastructure more effectively.

If your ministry or city is evaluating land-value reform, Unitism® can help with valuation frameworks, fiscal and distributional modeling, policy design, legislative implementation, and plain-language stakeholder education grounded in tri-factor economics.