5. Business Recessions

The largest asset in every economy is land, followed by buildings, followed by public infrastructure. So what people imagine are industrial economies have remained, basically, land economies.

— Michael Hudson

Professor of Economics, University of Missouri, Kansas City

Why is something as basic as land still important in our technologically-advanced world? After all, developed nations even have thriving internet economies, where wealth is created virtually yet leads to tangible benefits in the material world. Companies such as Google don’t even seem to use significant amounts of land in the vast majority of their business transactions. Or do they?

In order to understand why land is still essential in today’s economy, we need to remember that land is the access mechanism by which people and companies benefit from social wealth. Internet conglomerates, for example, benefit from a labor pool of highly skilled employees who live in the neighborhoods that surround their offices; they also benefit from vast technological infrastructures created by countless people and companies over decades, all of which add value to land. These benefits are accessible by location, which is in large part why Google was able to become one of the most successful companies in the world: Its success has to be placed in the context of the society in which it exists. Had Google been founded in a developing nation that lacked a highly trained workforce and sophisticated capital infrastructures, its success would have been less likely.

MEDIA 5-1: BILL MOYERS ESSAY:

THE UNITED STATES OF INEQUALITY

In California’s Silicon Valley Facebook, Google, and Apple are minting millionaires, while the area’s homeless are living in tent cities at their virtual doorsteps.

http://unitism.co/theusofinequality

Now let us look at what happens when a society experiences an economic recession or depression. In an economic recession or depression, there seems to be a lower demand for products that were formerly in greater demand, although this isn’t really the case: The same human desires that stimulated demand before continue unabated, but now can no longer be satisfied—so technically we still have the same demand as before. What we lack are the same means to fulfill that demand. This causes economic activity to constrict, and this constriction can lead to economic recessions and depressions.

In a recession or depression, unemployed workers remain willing to work so that they can afford to buy the things that they continue to desire. And herein lies the crux, the great enigma that economists have wrestled with for centuries: Since there is a continued demand for products and since people have a continued desire to work and produce, why is it that people can’t produce the goods and services that other people want to buy but can’t?

Many economists point to a constriction in the money supply as the root cause of a society’s inability to consume. But this conclusion is the economic equivalent of putting the cart before the horse because the creation of wealth must always precede the availability of money, since money only functions as a medium in the exchange of wealth. In other words, it isn’t a lack of money that fundamentally creates economic contraction, but rather a lack of wealth production. For example, when a lone factory in a small town shuts down, the town often experiences an economic depression because the community no longer has the same wealth-producing capacities as before; laid-off factory workers and their families therefore spend less. When demand for goods can’t be satisfied because of what seems to be a shortage of money, we’re in effect talking about a restriction of wealth production somewhere in the economic cycle, which in turn leads to an eventual reduction in the supply of money (unless it becomes otherwise inflated, such as by central bank decree).

Economists talk a lot about the need for a consumer economy (as if consumption alone were the purpose of life, the end-all to happiness and bliss). Yet few economists realize that we can’t have a consumer economy if people can’t afford to consume, and the only way they can afford to consume over the long run is if they create new wealth to either consume at that time or to defer as investments for later consumption. Simply put, the best way to have a functioning economy is to focus on having a wealth-producing economy. But when wealth can’t be created in spite of the need for such, the production of wealth has been artificially limited, and this artificial limitation is the root cause of business recessions.

As we recall, there are three factors involved in the production of wealth: nature, human labor, and capital goods. A society undergoing a recession has plenty of unemployed labor to spare, so lack of human labor isn’t the constricting factor. And although it’s often claimed that the root cause of diminished wealth production is a lack of money (leading to a lack of access to capital goods), lack of money is only the effect of a deeper, underlying dysfunction. For example, recent attempts at curing the economic depression in the United States through increases in the money supply have shown that such increases don’t necessarily resolve the issues at hand, except to divert more money into the hands of those who already seem to have plenty to spare.

Thus, could it be that the high cost of land restricts the optimal functioning of the economy? Because the cost of land—and therefore the cost of location—directly affects people’s abilities to interact and connect with one another in the context of society, the expensive price of land has consequences that reverberate through the entire economy and inevitably lead to restriction in the production of wealth throughout society.

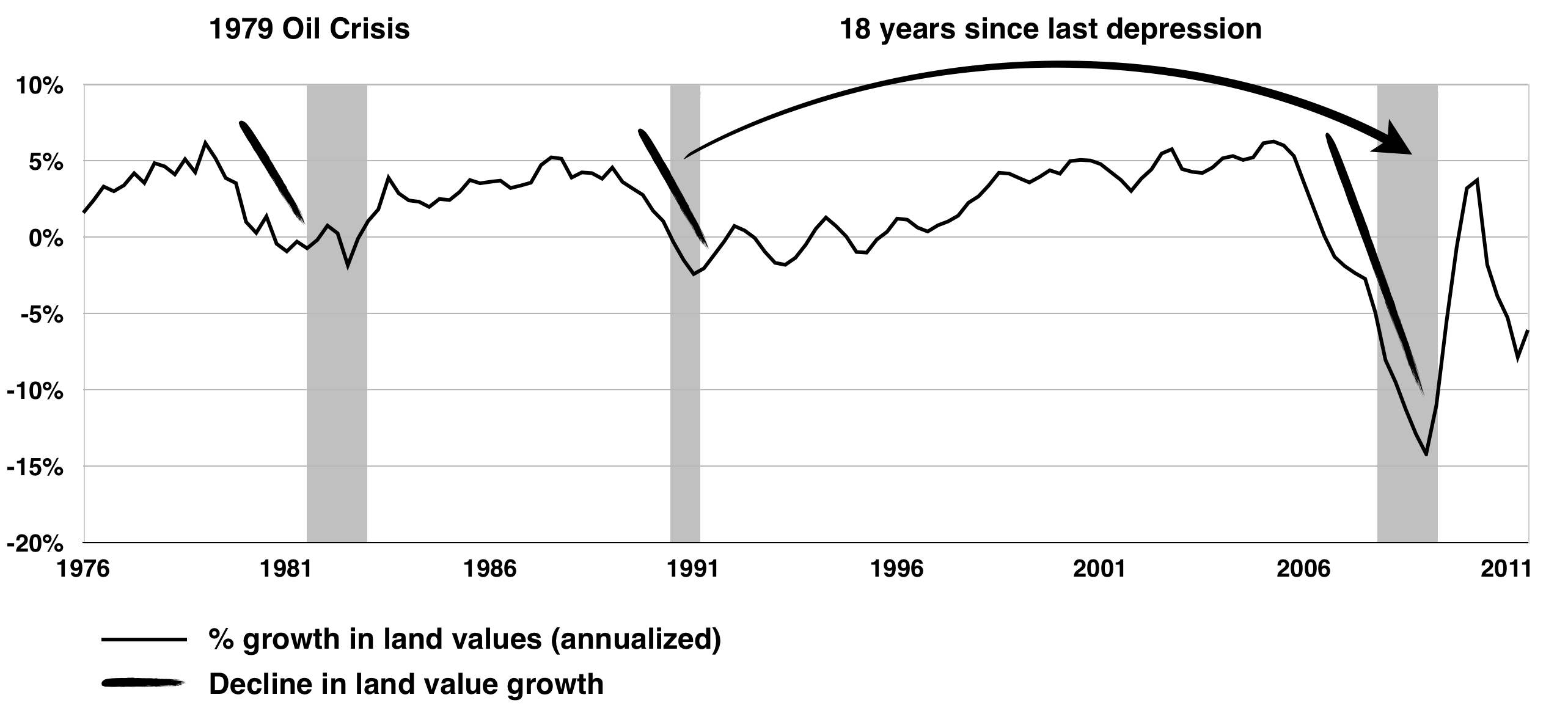

In 1983, British economist Fred Harrison published his seminal book The Power in the Land, in which he analyzed the economic history of Great Britain since 1701 and noted that property prices—driven by increases in underlying land values—tended to undergo boom-and-bust cycles about every eighteen years.20 He discovered that these cycles, in turn, affect the business cycle, and not the other way around. In a 2007 article in MoneyWeek, Harrison asked the rhetorical question of why many so-called experts haven’t been able to accurately predict the direction of the housing market: “Why do these ‘experts’ get it so wrong? It’s because they are working with defective models, which assume that the health of the property market depends upon the condition of the rest of the economy. In fact, my research suggests that property is the key factor that shapes the business cycle, not the other way around.”21

Harrison explains in The Power in the Land how land values over time become so expensive that too little wealth is left to pay for goods and services. The reason land becomes too expensive too quickly is because realestate speculation allows property owners to demand prices for land that are higher than the economy can realistically sustain. In a sense, property owners have the ability to demand tomorrow’s wealth output today, because they have the power to withhold land from use and public enjoyment in expectation of future gains. This process creates an artificial constriction in the supply of land, which makes the price of land increase at a rate the economy cannot sustain. But because people can’t compromise on basic subsistence, land eventually becomes unaffordable, and the price of land contracts simply because it has to. At the same time, businesses are no longer able to make a profit after paying for rent and mortgages: Production stalls while consumption drops; a depression ensues. In time, once wages have sufficiently recovered, a new cycle begins, and the whole process starts all over again: Land values eventually increase until they reach a point where they grow so much that they then forcibly contract once more, leading to another depression, and so forth.

These major business cycles happen on average about every eighteen years, and are usually punctuated by a single, brief recession along the way. According to Harrison, the property cycle generally undergoes a fourteen-year upswing: The first seven years are a recovery phase from the previous bust, after which a seven-year boom phase ensues. This boom phase includes a two-year run-up in real-estate prices toward the end, and it’s inevitably followed by a severe price correction that lasts about three to five years.22 Harrison’s observations were so on point that he went on record to accurately predict not only the timing of the major depression of 1992, but also the global 2008–2010 depression in 1997—eleven years before the depression occurred:23

The property boom of 2000 will come as a shock to Gordon Brown [who was Britain’s Chancellor of the Exchequer at the time, and later, in 2007, became Britain’s Prime Minister], who, if he is still presiding in Britain’s Treasury in the first decade of the millennium, will . . . be politically traumatised by the astronomical unearned gains from land that will be pocketed by shrewd operators who know how to manipulate the tax system. . . . The consequence is predictable. By 2007 Britain and most of the other industrially advanced economies will be in the throes of frenzied activity in the land market equal to what happened in 1988/9. Land prices will be near their 18-year peak, driven by an exponential growth rate, on the verge of collapse that will presage the global depression of 2010. The two events will not be coincidental: the peak in land prices not merely signaling the looming recession but being the primary cause of it.

ILLUSTRATION 5-2: LAND VALUES AND ECONOMIC DEPRESSIONS

Fred E. Foldvary is another prominent economist who also published his timely predictions of the 2008–2010 depression in 1997: “The 18-year cycle in the U.S. and similar cycles in other countries gives [this] cycle theory predictive power: the next major bust, 18 years after the 1990 downturn, will be around 2008, if there is no major interruption such as a global war.”24 He goes on to explain in greater detail how land speculation causes economic depressions:

When a boom is underway, the anticipated increase in rent induces speculators to buy land for price appreciation rather than for present use, which causes the current site value to rise above that warranted by present use. Once widespread speculation sets in, land values are carried beyond the point at which enterprises can make a profit after paying for rent or mortgages. The rate of increase of investment slows down, eventually reducing aggregate demand as the slowdown ripples through the economy, increasing unemployment and bringing forth a depression. Thus a fall in demand follows the initial cause, the rising cost of land.

TABLE 5-3: PEAKS IN LAND VALUES, PEAKS IN CONSTRUCTION, AND ECONOMIC DEPRESSIONS

| Peaks in Land Values | Interval (years) | Peaks in Construction | Interval (years) | Economic Depressions | Interval (years) |

| 1818 | — | — | — | 1819 | — |

| 1836 | 18 | 1836 | — | 1837 | 18 |

| 1854 | 18 | 1856 | 20 | 1857 | 20 |

| 1872 | 18 | 1871 | 15 | 1873 | 16 |

| 1890 | 18 | 1892 | 21 | 1893 | 20 |

| 1907 | 17 | 1909 | 17 | 1918 | 25 |

| 1925 | 18 | 1925 | 16 | 1929 | 11 |

| World War II | |||||

| First Oil Crisis | |||||

| 1973 | — | 1972 | — | 1973 | — |

| Second Oil Crisis | |||||

| 1979 | 16 | 1978 | 14 | 1980 | 17 |

| 1989 | 1986 | 1990 | |||

| 2006 | 17 | 2006 | 20 | 2008 | 18 |

| Averages: | 17.50 | 15.38 | 18.13 | ||

One of the key characteristics of science is predictability: If we can’t make accurate predictions, the model we’re using is faulty. If, on the other hand, we can have a general idea of outcomes based on a predictable pattern, then our economic model warrants a closer look. Like a prophet drawing from both his scientific experience and his intuitive insight, Foldvary issued another warning in an article he published in March 2012 titled “The Depression of 2026”:

If shocks [from outside the U.S. economy] don’t interrupt the cycle, the deep fiscal and monetary structures of the U.S. economy, which have not changed in 200 years, will generate the next boom and bust just as they have done so in the past. But the Crash of 2026 will be much worse than that of 2008, because as the U.S. government continues its annual trillion-dollar deficits, by 2024 the U.S. debt will have grown so large that U.S. bonds will no longer be considered safe, and in the financial crisis the U.S. will no longer be able to borrow the funds needed to bail out the financial firms. Americans still have time to prevent the next great boom and bust, but they are culturally bound to the status quo, as are almost all economists, so the warnings will go unheeded as they did during the 1990s and 2000s. We are now far upstream, but heading down into the river of no return to the real estate and financial waterfall of 2024–2026.

Will it happen? Strong tendencies seem to move us in this direction. Unfortunately, many politicians today— and homeowners bound to expensive mortgages—want properties to become more expensive in order to help the economy out of its recession. What most people don’t yet realize is that the value of land is best shared, and that whenever we profit from land, we profit from society. Indigenous peoples have long known this ancient and timeless wisdom, of course, yet we’ve forgotten it. Chief Crowfoot of the Siksika First Nation in southern Alberta, Canada, for example, reminds us, “As long as the sun shines and the waters flow, this land will be here to give life to men and animals. We cannot sell the lives of men and animals. The land was put here by the Great Spirit and we cannot sell it because it does not belong to us.” We in the modern age have forgotten this simple truth; our entire economy is built upon this one presumption that nature is property. The next business cycle will unravel before we know it, and it won’t be too long before we’ll have to deal with the next major depression and the immense personal impact that our ongoing profiting from land will have upon our lives.